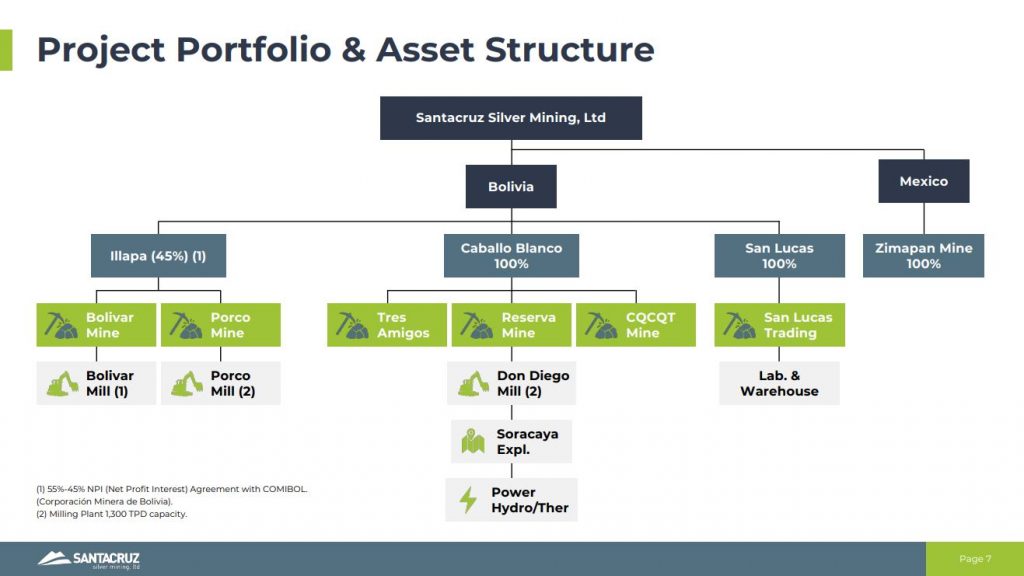

Arturo Préstamo Elizondo, Executive Chairman and CEO of Santacruz Silver Mining Ltd. (TSXV: SCZ) (OTCQB: SCZMF), joins me to recap the key record Q2 2025 financial results along with a comprehensive review of all operations. Santacruz Silver operates 1 mine in Mexico, and 5 mines, 3 mills, and an ore feed-sourcing and metals trading business in Bolivia, as an emerging mid-tier silver and base metals producer.

Q2 2025 Highlights

- Revenues of $73.3 million, a 4% increase year-over-year.

- Gross Profit of $25.3 million, a 59% increase year-over-year.

- Net Income of $21.0 million, a 1,348% increase year-over-year.

- Adjusted EBITDA of $26.8 million, a 68% increase year-over-year.

- Cash and short- and long-term investments of $57.8 million, a 691% increase year-over-year.

- Working Capital of $60.3 million, a 303% increase year-over-year.

- Cash cost per silver equivalent ounce sold ($/oz) of $19.48, a 10% decrease year-over-year.

- AISC per silver equivalent ounce sold of $22.95, a 8% decrease year-over-year.

Q2 2025 Production Highlights:

- Silver Equivalent Production: 3,547,054 silver equivalent ounces

- Silver Production: 1,423,081 ounces

- Zinc Production: 21,148 tonnes

- Lead Production: 2,773 tonnes

- Copper Production: 229 tonnes

Arturo discussed the very strong revenues, gross profit, net income, adjusted EBITDA, cash and cash equivalents, and working capital all up substantially in year-over-year metrics. In addition their cash costs and All-In Sustaining Costs (AISC) numbers came down in a meaningful way due to a combination of factors from mine optimization work paying off, to favorable currency exchange rates, and the positive impact of paying down the Glencore loan early, which will save the Company US$40 million. The Company plans to successfully complete the final 2 payments to Glencore by October 31, 2025, and will likely pay off both installments in the month of September. The company also announced a sale of 70 million Bolivian Bolivianos Promissory Note at 7.00% interest rate, a maturity date of June 15, 2026, just to give them treasury efficiencies for working capital in country.

Switching over to the operations for the quarter, there was better revenues from their San Lucas ore-feeding business, which is now absorbing the Reserva Mine ore to then blend it with ore from the small-scale miners. This leaves the ore from both the Tres Amigos and Colquechaquita mines to report to Caballo Blanco, making all operations much more efficient with better metals recoveries. The San Lucas production and revenues largely offset the lagging effects in the quarter from the water issues at Bolivar, which have now been mostly resolved, and those high-grade veins will be a bigger contributor to production again for H2 of 2025.

Transitioning over to Mexico, we discussed the higher-grade 960 Level at the Zimapan Mine starting to contribute, and how this will continue growing in the Q3 and Q4 production profile from Zimapan for the balance of this year and for many years into the future.

Arturo also highlighted that with the strength of the balance sheet, the coming elimination of the Glencore debt, and robust incoming revenues, that the Company is now currently ramping up more exploration and development work at their Soracaya Project, to put it on the pathway to primary silver production about a year and a half out. An internal study was completed by Glencore with an estimated capex of ~US$40MM for construction of a processing plant and tailings facility. Mine plan envisions a 7 year mine life with average annual payable production of ~4.5MM oz AgEq (based on consensus prices). Development is subject to permitting.

If you have any follow up questions for Arturo regarding Santacruz Silver, then please email them to me Shad@kereport.com.

- In full disclosure, Shad is a shareholder of Santacruz Silver at the time of this recording, and may choose to buy or sell shares at any time.

Click here to follow the latest news from Santacruz Silver

.

.