Has the Chinese Equity Market Bottomed? A Technicians Look

For those who like to read charts here is a great breakdown of some technical factors that show the Chinese equity market has bottomed. The author Martin Pring shows us 11 charts that support the argument that the worst is over. This would be huge for the global investment world as the approximately 50% fall in the Shanghai Index from last June impacted markets around the world.

Obviously there are a number of fundamental factors that would say the worst is not over but that is why I think a recovery, if we see one, will be slow.

Click here to visit the original posting page over at StockCharts. I highly recomend signing up for StockCharts if you have not already. There is a wealth of knowledge as well as some great charting options.

…

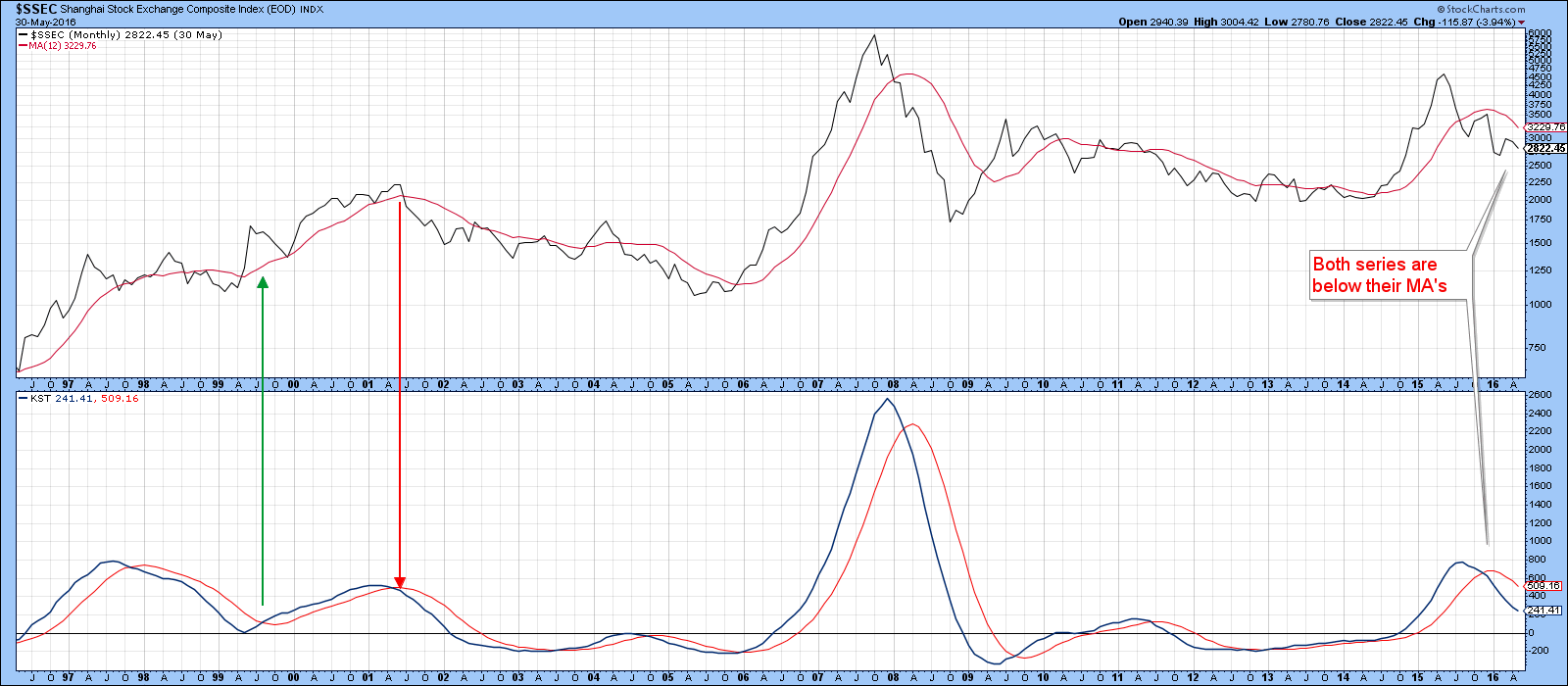

The Chinese equity market as reflected in the Shanghai Composite $SSEC has fallen by close to 50 % from the 5166 level on the June 2015 high to its late January 2016 closing low of 2655. The late, great, Edson Gould observed in the early 1970’s that bear markets often cut 50% off their value. For that reason alone there are grounds for exploring the possibility that the Chinese bear market may be getting long in the tooth.

Chart 1 compares the Shanghai Composite ($SSEC) to a long-term KST. My objective way of filtering out bull markets is to wait for the Index and the KST to move above their 12-month and 9-month MA’s respectively. It’s not a perfect approach by any means, but then that’s true for all technical analysis. Right now the model is bearish because both series are below their averages. However, we must also be mindful that these are long-term indicators, which assume a bear market of at least 18 months duration. In that respect, the current bear market has only been in force for about 12 months. That means that if we have seen the bottom, this approach is guaranteed to be unduly late this time around. That means that if we are to make a bullish case for Chinese equities it will have to rest on shorter-term indicators turning first, thereby resulting in a kind of reverse domino effect.

Chart 1

The bullish-reverse-dominos

In this respect, Chart 2 compares the Shanghai Composite ($SSEC) to my Chinese Diffusion indicator. The green highlights tell us when a basket of stocks in the Shanghai 50 are above their 50-week MA’s and when that number is also above its (red dashed) 15-week MA. An example of a buy and sell signal is displayed for the 2014-15 period. That indicator recently went bullish. The chart shows that most of the time, bullish signals have a tendency to remain positive for many months, sometimes longer. We never know for sure, but the fact that there are very few instances of signals lasting less than 10 months, gives me confidence that we could be at the beginning of something big here.

Chart 2

Chart 2

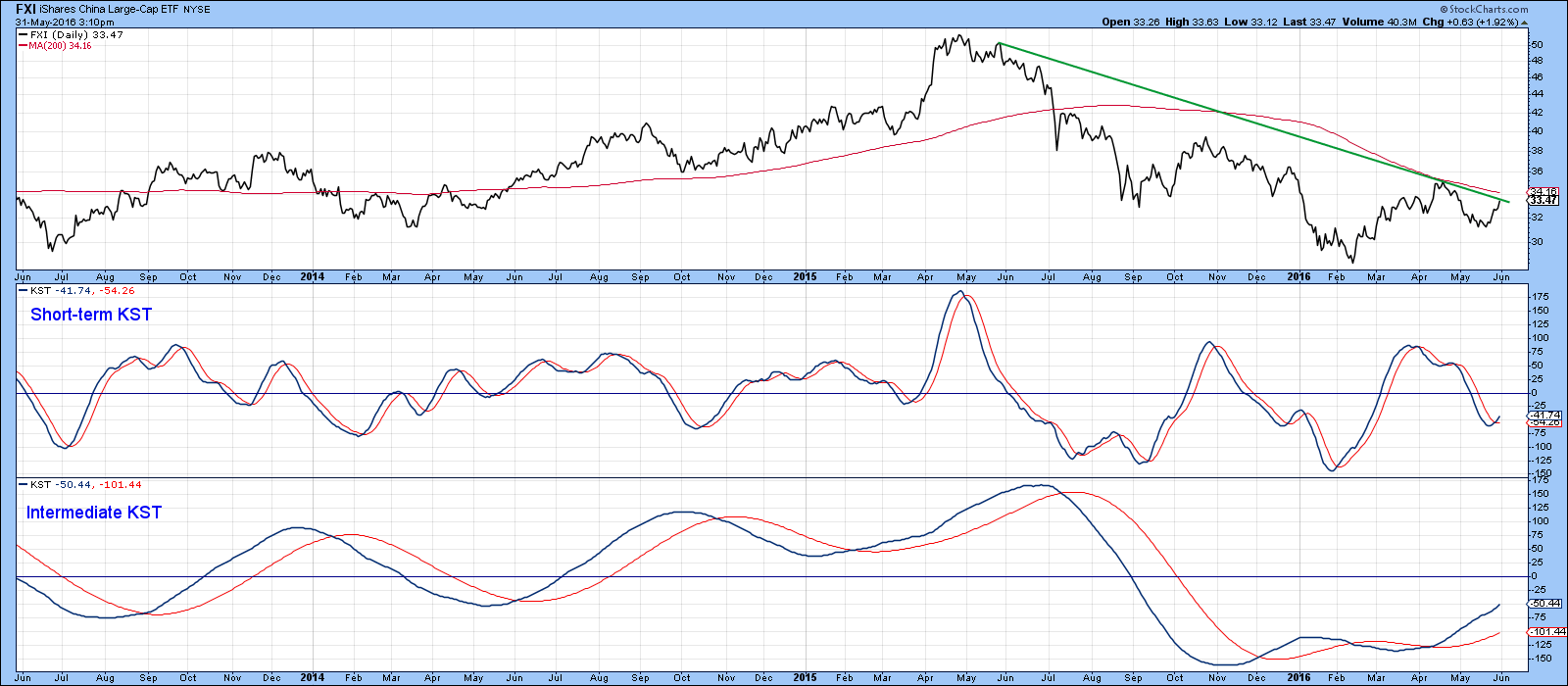

That feeling is also reinforced by the fact that the Shanghai Composite also violated a major bear trendline on Tuesday. This is shown in Chart 3, along with the fact that the short-term KST has begun to turn. Finally, the more dominant intermediate series went bullish a couple of weeks ago. Now if this is still a bear market, meaning that last January 28 was not the final low, I would not place that much emphasis on this positive oscillator action. However, if Tuesday’s tipping of the very fine technical balance turns into something stronger, we could be in for a very large intermediate or primary trend advance.

Chart 3

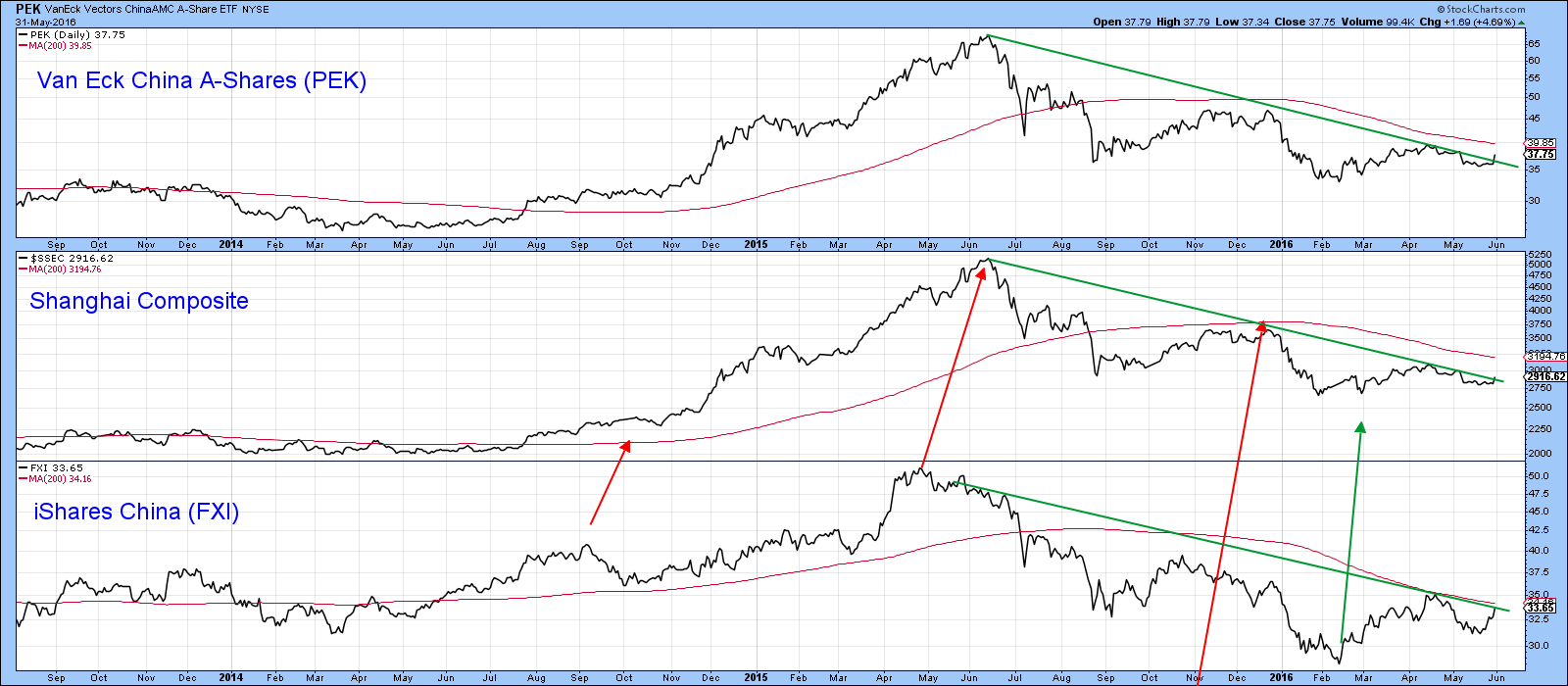

Chinese ETF’s

There are several ETF’s that specialize in China, but the two most popular seem to be the iShares China (FXI) and the Van Eck China A-Shares (PEK). They are both featured in Chart 4 along with the Shanghai Composite itself. The PEK seems to reflect the price movements in the Shanghai better than the FXI, though in several instances the red arrows show that the FXI often leads the Chinese Index. Right now only one ETF, the PEK, has rallied through the bear trendline, though the FXI looks set to follow.

Chart 4

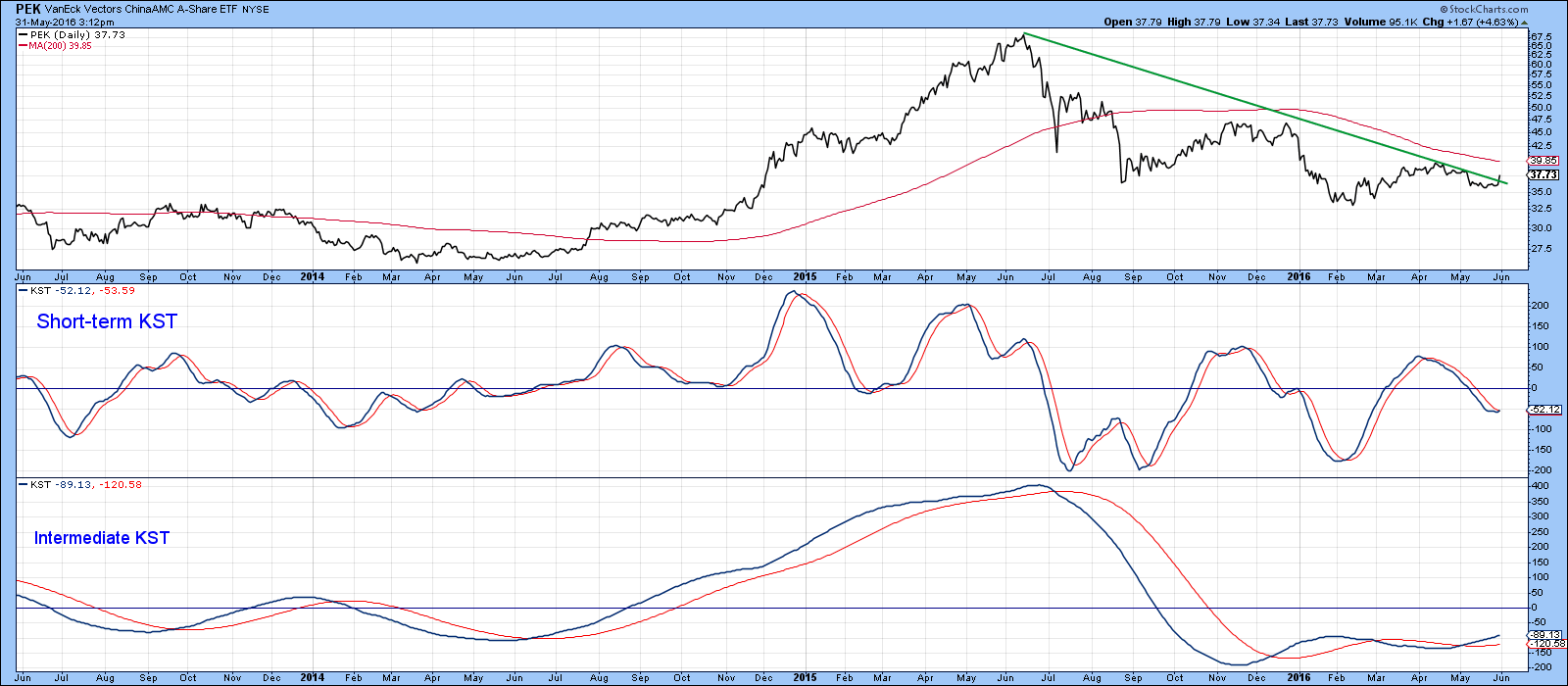

Charts 5 and 6 show that both the PEK and FXI have experienced short-term and intermediate KST buy signals.

Chart 5

Chart 6

Volume, relative to the recent past, was very heavy on Tuesday but is not included in the stats published by StockCharts. However, we can get a feel for volume trends in the PEK by applying a 14-day Money Flow Indicator (MFI) to the data. This is featured in Chart 7, where you can see that it has just violated a small down trendline in a similar fashion to violations that preceded the two previous intermediate rallies.

Chart 7

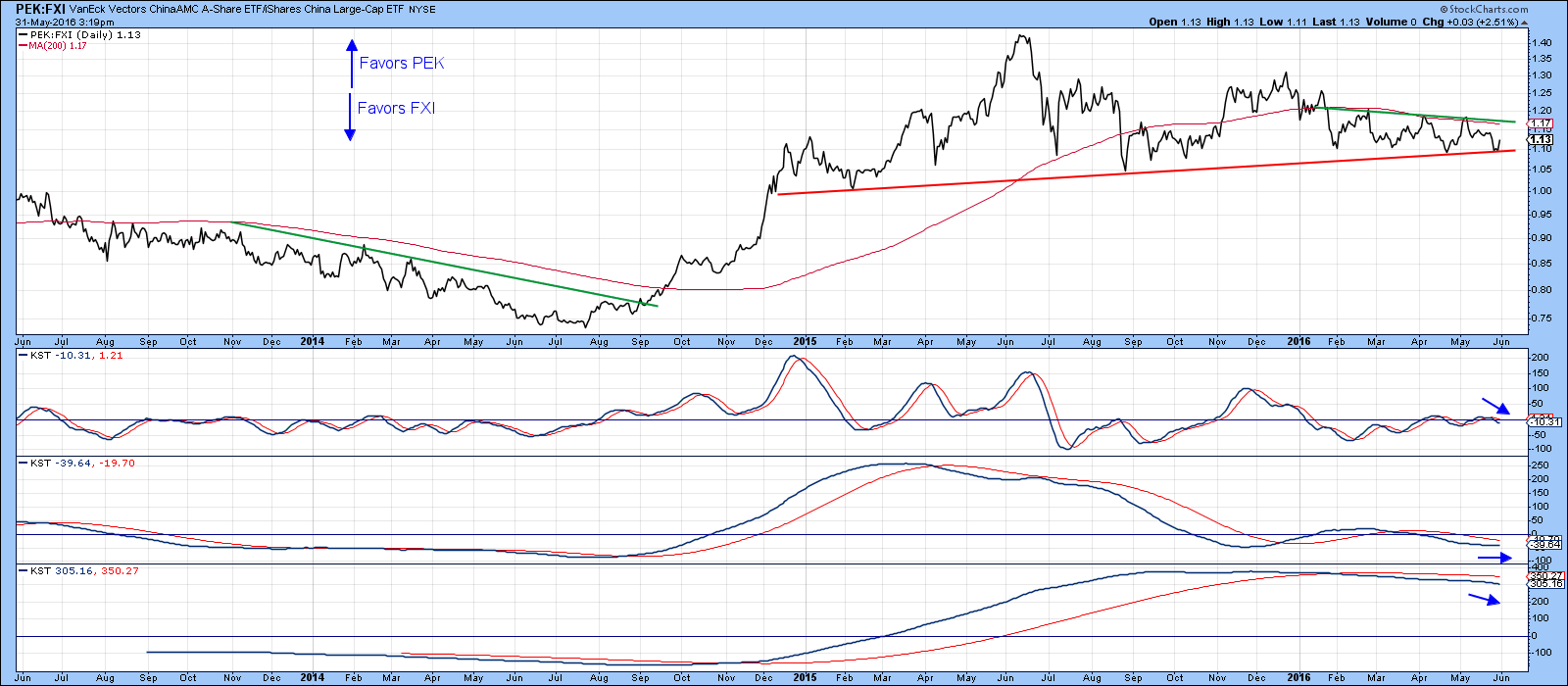

PEK or FXI

Chart 8 compares the performance between the two ETF’s. Sometimes there is a clear-cut choice between the two, such as the 2014 down trendline break. However, in the last few months, the ratio has been in a trading range bounded by the green line on the upside and the much more significant red line on the downside. Momentum is universally bearish i.e. favoring the FXI, but until that red line is penetrated we do not have an open and shut case.

Chart 8

Chart 8

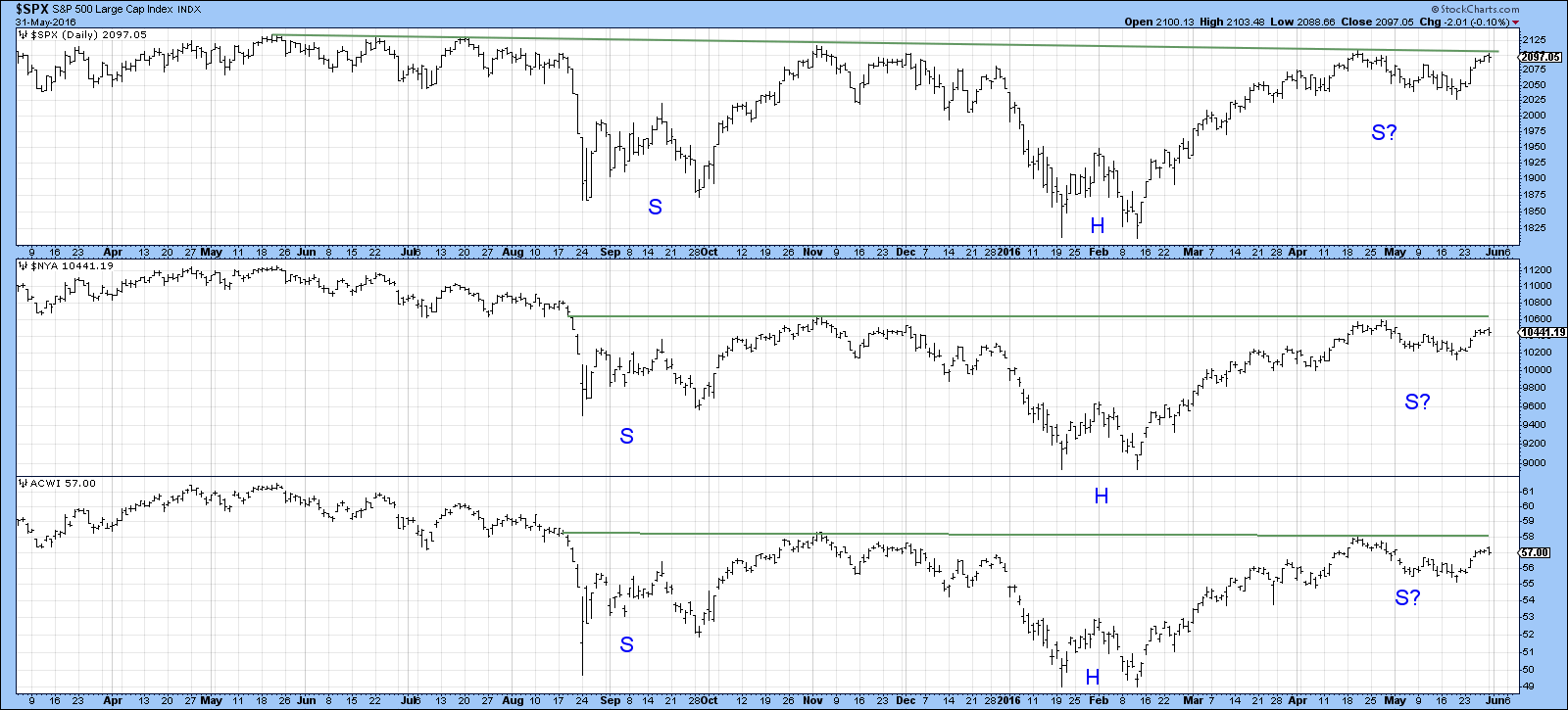

What would a Chinese rally mean for US equities

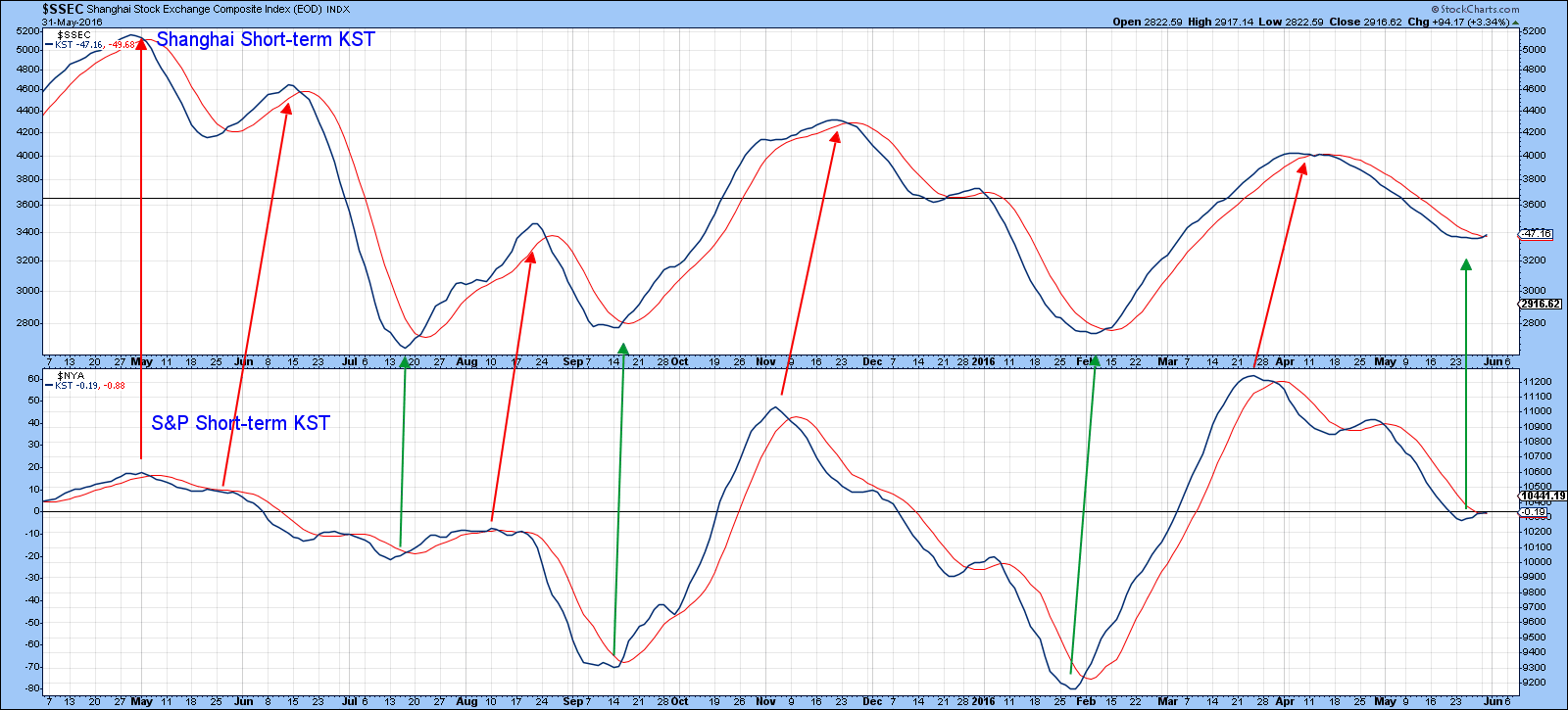

There are times when the Shanghai Composite ($SSEC) leads the S&P 500 ($SPX) as it did at the 2009 low and times when the US market leads its Chinese counterpart. Chart 9 shows that recently the US has been the leader on both the upside and downside when measured in terms of KST turning points. Both series have very marginally moved above their respective 10-day MA’s. However, if our reading of the Chinese markets is correct that should mean that the Shanghai KST will drag up the KST for the S&P 500, thereby resulting in a breakout from Chart 10.

Chart 9

Chart 10

Chinese Short Interest

Finally, just one more chart, as published by Bloomberg over the weekend. It shows that the short interest ratio for the largest Hong Kong ETF trading in mainland securities has recently rallied to a level slightly in excess of 6%. The green and red arrows are purely my own interpretation and show how the trend of the short interest has recently been moving inversely with the price. We do not know the ultimate duration and magnitude of this rally in short interest and the data points are very limited, but given the recent relationship and the ratio’s heady level, it sure looks bullish to me.

Chart 11

Good luck and good charting,

Martin J. Pring

The views expressed in this article are those of the author and do not necessarily reflect the position or opinion of Pring Turner Capital Group or its affiliates.

Looks like those charts are sniffing a massive few rounds of QE.