Black Knight Mortgage Monitor: “Purchase Lending Hits Highest Level Since 2007”

Some interesting stats from this posting below. We all know the many warning signs in the current economy but mortgages are another debt instrument that I like to keep an eye on. I don’t think that this data is a definitive sign of anything to come but it is interesting to see the similarities between the hurricane in 2007 and the ones this year.

This posting is from a great site Calculated Risk. Click here to visit the original posting.

…

Black Knight Financial Services (BKFS) released their Mortgage Monitor report for July today. According to BKFS, 3.90% of mortgages were delinquent in July, down from 4.51% in July 2016. BKFS also reported that 0.78% of mortgages were in the foreclosure process, down from 1.09% a year ago.

This gives a total of 4.68% delinquent or in foreclosure.

Today, the Data & Analytics division of Black Knight Financial Services, Inc. released its latest Mortgage Monitor Report, based on data as of the end of July 2017. Reviewing second quarter mortgage origination volumes, Black Knight finds that while overall mortgage lending saw a 20 percent increase over Q1 2017, total volumes were down 16 percent from Q2 2016. Additionally, although purchase lending hit its highest level in 10 years, the total number of purchase mortgages being originated still falls far below pre-crisis (2000-2003) averages. As Black Knight Data & Analytics Executive Vice President Ben Graboske explained, more stringent credit requirements enacted in the wake of the Great Recession may be hampering purchase lending volumes.

“We saw positive growth in lending in the second quarter, with $467 billion in first lien mortgages originated,” said Graboske. “While down 16 percent from a year ago, that marks a 20 percent increase in mortgage lending over Q1. Drilling down into the make-up of those originations, we see that refinance lending made up just 31 percent of all Q2 originations – the lowest such share in over 16 years. Refinance volumes were down as well, falling 20 percent from Q1, but that drop was more than offset by a 57 percent seasonal rise in purchase lending. Purchase originations totaled $321 billion in Q2 2017; up six percent from last year, and the highest quarterly volume since 2007. As a result of growing average loan amounts for purchase originations, the total dollar amount of purchase originations is higher than averages seen from 2000-2003, prior to both the peak in home prices and the Great Recession that followed. This is partly due to rising home prices, but also comes as a result of an all-but-total absence of second lien usage for purchases, a shift toward high-dollar/low-risk loans among non-agency lenders and a higher share of cash purchases at the lower end of the market.“However, the number of purchase loans being originated still lags the pre-crisis average by almost 30 percent; while overall purchase origination volumes are strong from a total dollar amount perspective, the market still does not appear to be performing at peak capacity. One key cause is the more stringent purchase lending credit requirements enacted in response to the financial crisis. Consider that borrowers with credit scores of 720 or higher accounted for 74 percent of all Q2 2017 purchase loans as compared to a pre-crisis average of 47 percent. Today, there are 65 percent fewer purchase loans being originated to borrowers with credit scores below 720 than in those years. The lack of credit availability for those borrowers is causing a strong headwind for the purchase market. Using 2000-2003 averages as a measure, as many as 645,000 purchase loans were not originated in Q2 due to tighter lending standards. To put it another way, the purchase market is operating at less than two-thirds of peak capacity because of these factors.”

emphasis added

image: https://3.bp.blogspot.com/-vuO-f0Tk_dM/WbYgi0lFeYI/AAAAAAAAsOA/CJEGRXa9quMiYplolFzEqn7KC-x1SDgjACLcBGAs/s320/BKFSJuly2017.PNG

Click on graph for larger image.

Click on graph for larger image.

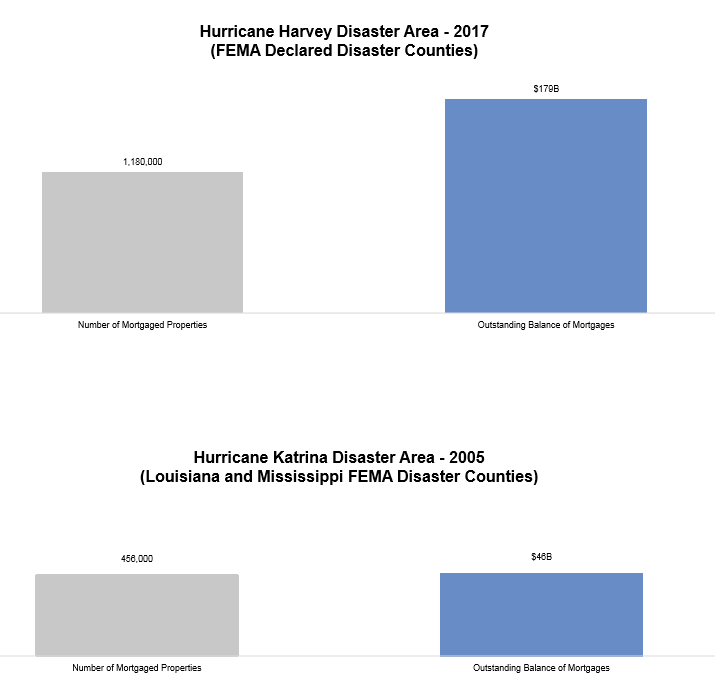

This graphic from Black Knight compares the number, and balance, of mortgages impacted by hurricane Katrina in 2005, and hurricane Harvey in 2017.

From Black Knight:

• Though the situation around Hurricane Harvey continues to evolve, millions of Americans’ lives have been impacted by the storm and immense flooding

• The effects on mortgage performance may actually exceed those of Hurricane Katrina in 2005, both due to the magnitude of the rainfall as well as the population of the impacted area

• FEMA-designated disaster areas in southeast Texas associated with Hurricane Harvey have over twice as many mortgaged properties as Katrina’s FEMA-designated disaster areas, carrying nearly 4x the unpaid principal balance.

There is much more in the mortgage monitor.

CHINESE agree with me…… 🙂

http://www.zerohedge.com/news/2017-09-11/1000-iphone-too-expensive-middle-class-chinese-buyers

Electric will become more expensive….

http://www.zerohedge.com/news/2017-09-11/half-floridians-without-power-state-braces-lengthiest-restoration-us-history

zero hedge ……article

Rational people recognize this $20 trillion for the supernatural scale of obligation it represents, and understand that it will never be paid back, so, what the hell? Why not just drop the pretense, but keep on working this racket of the government borrowing as much money was it wants, and the Federal Reserve creating that money (or “money”) on its computers to infinity. Seems to work so far.

I used to own 100 trillion dollars (Zimbabwe). I offered to pay off America’s entire debt but nobody took me seriously. So, I gave it to my father. I think he still has it. Paying off that $20 trillion is a piece of cake when no lawful standard of value exists. There is no fundamental difference between a dollar American and a dollar Zimbabwean. Both are made of paper and ink. Even my 6 year old daughter can make money.

Interestingly there was a time when 100 trillion dollar Zimbabwe notes sold for about US$1.

Strangely they now often sell for about US$20.

I wonder was that says!

When I bought it it was 100,000,000,000,000 to 5.

A real good reason to own …..hard assets……….. , but, we have been saying that for a long time……..

Because if there was an announcement of printing to infinty people would leave dollar investments even faster.

JUST HIGH LIGHTs…………before lights out

from zerohedge

Remember, Robert Rubin, deciding not to finish out his term as Secretary of the Treasury and left the Clinton administration just a few months before the dot.com bubble popped?

Maybe Fisher will get a job in Zimbabwe

http://www.zerohedge.com/news/2017-09-11/remember-houston-repairingrebuilding-100000-damaged-houses