Hour 1 – US Markets Disconnected from Economies and Precious Metals Stocks Continuing the Breakout

i hope eveyrone enjoys this weekend’s show. I spend a lot of time on the precious metals sector. It’s an outperforming sector so there can be a lot of money to be made in the right companies.

Please keep in touch by emailing me with any questions for guests or companies – Fleck@kereport.com

- Segment 1 & 2 – Jesse Felder joins me to kick off the show with his thoughts on the disconnect between markets and the underlying economy. In the second segment we look to the metals sector. As Jesse says BANG has preformed better than FAANG.

- Segment 3 – Dave Erfle joins me to discuss his trading strategy now that junior gold stocks have moved higher. We also touch on a change to the rules for TSX listed companies for raising money.

- Segment 4 – Dave Erfle is back with me for a round table discussion with Philippe Cloutier, President and CEO of Cartier Resources. This week Cartier Resources released a new resource estimate that brings the total resource to almost 1.2million ounces. Dave wants you all to know that he holds shares and covers Cartier in his newsletter.

Exclusive Company Interviews This Week

- Novo Resources – Questions on ore sorting, exploration work on deck, and possible project economics

- Aztec Minerals – A New Focus on the Tombstone Property in Arizona

- KORE Mining – A Complete overview of this advanced exploration company with assets in California and BC

Thanks Cory for another great week of interviews and daily editorials and another weekend show on the books. Ever Upward!

Junior Gold Miners Ready To Run

by @TheTechnicalTraders on 8 May 2020

“Gold, the bell-weather safe-haven asset, initially collapsed when the US stock market started the massive selloff in late February 2020, then recovered to higher price levels near $1785 recently. Since reaching these levels, Gold has stalled into a sideways price flag near major resistance.”

“Silver, on the other hand, is trading near $15.60 and has yet to really recover to anywhere near the levels it had achieved in early January 2020 (near $18.60).”

“Well, GDXJ, the Junior Gold Miners ETF, is suggesting a very strong price rally is taking place that may push both Gold and Silver substantially higher. Key resistance exists near $46.50. Once broken we believe a very strong price rally will take place pushing GDXJ price levels to $51 or $52. After that, a brief downside rotation will potentially retest the $47 to $48 levels before an even bigger upside rally takes place. What is even more important is that we believe this big breakout move could start as early as next week, May 12th or after.”

https://ceo.ca/@thetechnicaltraders/junior-gold-miners-ready-to-run

TMAC to be Acquired by SD GOLD

8 May 2020

“TMAC Resources Inc. (TSX: TMR) is pleased to announce that it has entered into a definitive agreement with Shandong Gold Mining Co. Ltd. (SH:600547; SEHK:1787) , through its wholly-owned, overseas subsidiary Shandong Gold Mining Co., Limited, pursuant to which SD GOLD has agreed to acquire all of the outstanding shares of TMAC at a price of C$1.75 per share in cash.”

Gold Telegraph ✪ @GoldTelegraph · 1h on Twitter:

“One of China’s biggest gold producers, Shandong Gold, has entered into an agreement to acquire Toronto-listed TMAC Resources for US$149 million”

“It is worth noting China’s Zijin Mining also purchased Continental Gold in March.”

“China rushing to buy gold deposits?”

https://twitter.com/GoldTelegraph_/status/1258766695566581761

SD Gold will be the real winner here, similar to how (SVM) Silvercorp just scooped up Guyana Goldfields on the cheap after the (GUY) management team had repeated performance issues at their mine and this decimated their share price over the last 2 years.

>> It is interesting that in both cases it is the Chinese companies taking over the distressed Mid-Tier Gold producers. As the piece above mentions, Shandong Gold also nabbed Continental Gold’s large development project.

Last year it was the Australian companies that were on the hunt, but the Chinese companies are on the prowl as well.

We’ll continue to see more consolidation of the wounded and distressed producers while they are still on sale relative to where they should be with the high gold prices in the $1700s. There are also a number of single-mine producers that look prospective to be taken over as “bolt-on” operations for the big boys that I believe we’ll see get acquired in the next 12-18 months.

__________________________________________________________________

(SVM) Silvercorp Metals to Acquire (GUY) Guyana Goldfields Creating a Diversified Precious Metals Producer

April 27, 2020

Speaking of Mergers…. Wallbridge and Balmoral have officially tied the knot.

(WM) Wallbridge Announces (BAR) Balmoral Securityholder Approval of Arrangement

8 May 2020

https://ceo.ca/@newswire/wallbridge-announces-balmoral-securityholder-approval

It should also be noted that just a few weeks back Excellon Resources finished gobbling up Otis Gold, making it the next in a long string of Silver producers to diversify into Gold.

(EXN) Excellon Completes Acquisition of (OOO) Otis Gold

April 23, 2020

http://www.excellonresources.com/news/details/index.php?content_id=240

There was a PR that came out yesterday that Sprott bought more Balmoral.

Yeah saw that David. Eric Sprott also mentioned the Wallbridge & Balmoral business combo on his interview 2 days back:

“Be Careful What You Buy.” Why Gold and Silver Are Good Bets Right Now – Weekly Wrap Up (May 8, 2020)

By Craig Hemke & Eric Sprott #AudioInterview

As coronavirus and containment measures continue to wreak havoc on the world economies, host Craig Hemke and Eric Sprott sit down to discuss all the gold and silver news you need to weather the storm. In this edition of the Weekly Wrap-Up, you’ll hear:

> Why silver is about to pop

> What’s behind the terrific week for the mining shares

> Are negative interest rates coming?

The bit on Wallbridge & Balmoral comes in around the 24 minute mark.

The bit on Freegold comes in at the 26 minute mark, Sprott thinks they may have hit the main feeder vein.

Silvercorp is my largest junior miner holding. It is the only precious metal stock I did not sell In 2011. Then I added 10 fold till it reached 65 cents Canadian in 2015. Even I sold nearly half, I am still holding 6000 shares. Every time I read its financials I am more convinced that it will take off. I am gong to keep holding it till silver is red hot.

Dragonite – I got positioned in Silvercorp in late 2015 during tax loss season, and you were the one that advised I go back and take a closer look at the valuation mismatch at the time. SVM is still my largest Silver position as well, with IPT Impact Silver now in a close 2nd position. I actually trade in and out of Silvercorp all the time and have for years (over 20 SVM trades this year).

Dragonite – I’ve told you before, but just wanted to thank you again for your contributions over the years. Cheers!

Execlsior, I am glad that you are willing to check out my information and buying into SVM. I also want to thank you for your tremendously information and ideas you shared on this board.

Thanks

I am glad that you checked out my information and acted on it. I am also grateful with the tremendous information and ideas you have shared on this board.

Thanks Dragonite.

The Chinese own the rare earth and critical metal markets, they have been moving very aggressively into all sectors of the commodity markets. Canada is very vulnerable, our wealth is tied to mining and we are asleep. America is seeing it’s farmland being bought up by foreigners. We in The Western World have become complacent, fat, lazy, and broke, the Asians see this and are exploiting our weaknesses. DT

Money is now pouring into the gold market, almost overnight the situation for gold equities has changed from one of wait and see to one of maybe I should have gotten in last month. For me, now is the time to strike. DT

Agreed DT. I can’t blame them for wanting to seize on good deals in the marketplace and maybe this will be a wake-up call to US and Canadian businesses get in gear with their own domestic acquisitions before the East buys up most of the West.

I lived in Calgary for 33 years. I am sad to see it slides in to a state of depression. Based on our rich natural resources and large per capita land size plus very intelligent population, Canada could become the richest country in the world. Unfortunately, the socialist attitude of the general public and conflicts between central government and province has brought the country to a halt. When I moved from China to Canada in the 80s, the wealth gap between China and Canada is huge. Even as a student , I could live many times better than my old job in China. Unfortunately, after 30 some years, this is no more. China has had a modern and vibrant economy, and Canada has moved backward. To be honest, this country needs to change. We need to have an economy where everyone do their best, instead of wanting government hands out. The whole country should treat every region the same and with respect. I am really sad seeing the decay of my region and other regions I have been. Except trying my best to make money I really don’t know what to do. I used to be very active in elections and volunteered in every election including door knocking for Jim prentice. The situation does not seems improve much. Not sure what to do any more.

I feel that we should work together with any other country including China to improve our wellbeing instead having a confrontation mentality. We are not US and we don’t need hegemony. We just need a rich and prosperous country

Vale Sees A ‘Very Vigorous’ Economic Recovery In China

Reuters | May 8, 2020

“Vale is seeing a “very vigorous” economic rebound in China, the iron ore miner’s principal export market, Chief Financial Officer Luciano Siani said during an online event hosted by Brazil newspaper Valor Economico on Friday.”

“Industrial activities (in China) are practically at their normal levels…Civil construction is also rising daily and steel and iron ore stocks are falling,” he said.

https://www.mining.com/web/vale-sees-a-very-vigorous-economic-recovery-in-china/

it is true. China has a very prosperous economy because the economy relies on numerous small private companies for the wealth creation and at same time its public sector is managed by a group of technocrats whose incentives are not quarterly profit but the long term growth, and its profit to supply government spending. Government needs the private sector to be creative and needs public sector to be profitable. It is quite effective at this stage. I am not sure how long this can last, but hope it won’t change. COVIT 19 caused short term halt but all the basic supply is very abundant. Government correctly made the decision to isolate cities and people obeyed the rules to wear PPE. Virus faded away rather fast and situation started to return to normal after economy restarted in March, except education sector which is still not normal yet.

DT – Speaking of Rare Earths….

New Technology Promises To Be Game-Changer In The Extraction Of Rare Earths

Valentina Ruiz Leotaud | May 10, 2020

“In a paper published in the journal Green Chemistry, the scientists explain that the patented extraction and purifying processes use ligand-assisted chromatography and are shown to remove and purify rare earth metals from coal ash, recycled magnets and raw ore safely, efficiently and with virtually no detrimental environmental impact.”

“About 60% of rare earth metals are used in magnets that are needed in almost everyone’s daily lives. These metals are used in electronics, aeroplanes, hybrid cars and even windmills,” Nien-Hwa Linda Wang, whose lab developed the technology, said in a media statement. “We currently have one dominant foreign source for these metals and if the supply were to be limited for any reason, it would be devastating to people’s lives. It’s not that the resource isn’t available in the US, but that we need a better, cleaner way to process these rare earth metals.”

(UUUU) (EFR) Energy Fuels to Enter Rare Earth Elements Sector

April 13, 2020

“Energy Fuels believes its fully licensed and constructed White Mesa Mill, which is the only uranium and vanadium mill in operation in the U.S. today, can play a key role in bringing the REE supply chain back to the U.S. from China. The Company’s primary business is – and will remain – uranium mining and production. However, Energy Fuels believes it can leverage its existing licenses, infrastructure and capabilities at the WMM to also produce REEs.”

Hi Ex, A breakthrough in the processing of rare earths would truly be a marvel of super scientific technology. Things to come, let’s hope it doesn’t happen at the expense of human values. DT

Agreed. The extraction method for Rare Earth Elements seems interesting, but if what the REEs are used for is the technology to control or limit humans then it may all be for not. However, just like REEs can be used in weapons, defense, lasers, and AI, they can also be used for more efficient and cleaner energy sources, advanced in medicine, and the side of computers and AI that is helpful and benefits the human family. It comes down to the intent behind of the use of the tool, like all human invention and creation.

(SOLG) (SLGGF) SolGold PLC Announces Royalty Funding Package for Alpala Project

by @accesswire on 11 May 2020

“The Board of Directors of SolGold (LSE & TSX: SOLG) is pleased to announce that SolGold has entered into a US$100 million Net Smelter Returns Financing Agreement with (FNV) Franco-Nevada Corporation , with an option to upsize the financing to US$150 million at the Company’s election, with reference to the Company’s flagship Alpala copper-gold project and the remainder of the Cascabel license in northern Ecuador.”

https://ceo.ca/@accesswire/solgold-plc-announces-royalty-funding-package-for-alpala

(SOLG) (SLGGF) SolGold PLC Announces Royalty Funding Package for Alpala Project

11 May 2020

“The Board of Directors of SolGold (LSE & TSX: SOLG) is pleased to announce that SolGold has entered into a US$100 million Net Smelter Returns Financing Agreement with Franco-Nevada Corporation, with an option to upsize the financing to US$150 million at the Company’s election, with reference to the Company’s flagship Alpala copper-gold project and the remainder of the Cascabel license in northern Ecuador.”

https://ceo.ca/@accesswire/solgold-plc-announces-royalty-funding-package-for-alpala

China is gold poor and silver rich, at least it is like that before. Since China does not have big gold deposits and the mining industry is made up with many small mines and small fields. So China has no choice but to expand. Since China is an old civilization so her gold and silver and other minerals have been exhausted. Even a couple of thousand years ago, the history books say that iron, lead, copper, silver mines were controlled by the emperor and his ministries. Now there is really not left under her territory, maybe with exception of aluminum. It is only natural for china to purchase mining resource worldwide, especially the China friendly areas like Africa and south america.

Yeah, that makes sense Dragonite, although I have to believe that with modern geology and mining methods many older sites could be reworked looking for missed ore still in the ground.

Regardless, yes, it makes sense for China to reach out and acquire the mineral wealth it needs to grow its infrastructure further, and again, I believe these are wise acquisitions. Silvercorp nabbing Guyana Goldfields, and SD Gold grabbing TMAC are really great deals for the acquiring companies longer term.

The Australian producers were grabbing the good assets in 2019 since they were cashed up from the currency exchange rate in their favor on costs, and a really high Aussie gold price to sell into.

My question is what are the Canadian and US Mid-tier producers doing sitting on their hands as the all the good looking girls are going to get invited to the dance before they have a chance to ask them on the date. 🙂

I believe China has a pocket full of american dollars, I would think they would want to trade alot of those dollars for mines/resources.

Yeah, makes sense for them to convert their US fiat dollars into tangible assets of true value.

Canada stands a good chance to be a vendor to China, supplying them with oil, gas, mineral , foods, and other industrial materials we can do better. We could be a very rich country if we try. But governments and general public seem not interested. Why?

Excelsior, sorry to start another topic. Recently uranium has surpassed 30,best in 7 years. The mine shutdown may contribute to it. The uranium stocks have not reacted much. Do you think uranium rally has legs?

Do you think we should take some profit on U stocks or keep holding?

Hi Dragonite – As far as the Uranium miners, I’ve been pretty much just holding my core positions and adding on weakness, and trimming a bit back into strength since Uranium bottomed at $17-$18 back in late 2016 and then again in late 2017.

I trimmed my positions and reduced my positions in 2018 and most of 2019, but started adding more back in tax loss 2019. I also added to a few positions in March when most assets sold down to take advantage of the weakness. I have nice profitable positions in my primary Uranium stocks (UUUU, URG, UEC, NXE) at this point, now that Nexgen finally got on the ball. My AEC position is still slightly underwater but has been pretty active again lately. I’m considering adding back my DNN and LEU positions again soon, and adding AZZ to the mix, possibly PEN.AX.

___________________________

From a macro picture the Uranium supply has nearly been destroyed at this point:

1) Cameco has now shut down both it’s primary mines: with Cigar Lake and McArthur River both shuddered for an indeterminate amount of time.

2) Rossing mine has pulled back production.

3) Palladin’s mines were put on care and maintenance years ago

4) Kazakhstan (the OPEC of Uranium) has cut production back

5) The US production from Energy Fuels, Ur-Energy, and Peninsula Energy is on care and maintenance.

6) The US Dept of Energy finally quit dumping onto the spot markets as a secondary supply the last few years, which helped.

7) Russian underfeeding has been greatly reduced as secondary supply where it has been adding substantially for the last decade.

8) Cameco, Ur-Energy, and Peninsula are buying in the spot to fulfill any remaining longer term off-take contracts.

9) The US Nuclear working group has just announced that as a matter of national security they are going to build up a stockpile of Uranium again

10) Most of the excess inventory from Japan has been mopped up at this point, so it is not being bought by utilities any longer.

11) the new reactor builds are continuing in China, other parts of Asia,

The Utility companies are going to get a rude awakening if they don’t start a new longer-term off-take contract cycle soon. Uranium finally broke out of the $24-$26 range it was stuck in and got up to $33 recently and is hovering in the low $30s. I see the low to mid $40s as a congestion zone as that is when some supply will come back on line from Kazakhstan and some of the lower cost ISR producers.

Really the Uranium mining sector needs the $50s or $60s for all in costs including more exploration to replace reserves and for back in mine reclamation costs. Something is going to have to give soon where Contracts in the $50s or $60s get established, and when that happens these U miners are going to move much quicker than most asset classes because the choices available are so concentrated. At this point I’m just gradually building up my Uranium positions over the next year, with profits from the PMs.

While on the Uranium topic, I posted this long U rant to David later on Sunday on last weekend’s show, so will just repost it here as a thought starter on some ideas and companies in the Uranium sector from my perspective.

> On May 3, 2020 at 5:52 pm,

Excelsior says:

It depends on what you are looking for as far as exposure to the Uranium sector, and the risks you are willing to accept with a position on any of the earlier-stage companies.

For those investors with little Uranium exposure at present, none of those 3 would be my preference coming out of the gate in this sector, but everyone needs to make their own choices and I don’t like to tell others what to buy. I just discuss companies that I own and why I like them, and other companies I find interesting, noteworthy, or newsworthy.

Personally, my preference with resource stocks is to first be positioned in the medium to small producers of the given commodity, or to have a position in the advanced developers, where they’ve found a known deposit that will be economical and get re-rated higher.

> So whether it is Gold, Silver, Base Metals, Uranium, Lithium, Oil, etc…. I start with getting a good position in the producers & key developers first.

I dabble in the exploration plays as well, but not with the same kind of weighting or conviction, because by definition the “discovery” plays are still waiting to prove up that their exploration can be tied together into a resource that makes sense to pursue. Only 1 in 3000 targets ever becomes a legitimate mine, so that means Las Vegas has better odds than an explorer finding an economic mine.

_________________________________________________________________________

For Uranium stocks, I’ve never been a fan of Cameco as the big boy producer, and as bloated Sr with deep mines and water mitigation to contend with, it has been swirling the drain for some time with longer term structural and growth issues. (I don’t hate Cameco or anything, and they’ll do fine in an uptrend, but I’d rather have a smaller market cap Uranium miner with more torque, and less major issues to contend with).

There aren’t many publicly traded U producers, and Paladin shuddered it’s mines, and I never liked Energy Resources of Australia, so I opted for the 2 main US producers (UUUU) (EFR) Energy Fuels & (URG) (URE) Ur-Energy because they’d be the first to get a bid when things started to recover (like they have on each of the small rallies that commenced since late 2016). In addition they are front and center with the Nuclear Working Group, and will benefit directly from whatever actions the US government does decide to take. Both Energy Fuels & Ur-Energy are also dual-listed, like Cameco, UEC, Dension, and Nexgen, which I prefer to find when possible for a more liquid and widely followed company in this niche’ market.

(PEN.AX) Penninsula Energy is Aussie company and relatively new producer operating in the US using the ISR extraction method for a small time, but last I heard they had put their producing wells on care & maintenance waiting for a better pricing environment, and just bought in the spot market to fulfill their current contracts like Ur-Energy and Cameco have also been doing.

For the developers there aren’t a lot to choose from, so (NXE) Nexgen is my favorite as it is the highest grade/largest undeveloped Uranium development project available, and won’t have the water issues of most companies in the Athabasca, like Fission, Cameco, Purepoint, UEX Corp, ALX Uranium, etc…

> I’m not sure if Nexgen will take it into production on their own, or if Cameco or Rio Tinto or BHP or some other larger producer will take them over, but the Arrow deposit will eventually be a mine. They are like the Mag Silver or Seabridge of the Uranium space.

Denison (DNN) (DML) will actually be the first developer to make it into production in the Athabasca basin, also using the ISR mining method, and they also have a few key hardrock deposits with known resources. I don’t currently have a position in Denison, but have owned them off and on for years. They also have a reclamation business, they consult and manage the Uranium Participation fund, they have a 20% interest in the mill that processed Cigar Lake’s feed and could process other mining deposits, and they have a large stake in GoviEx since Denison spun out their African assets to GXU. I’ll likely be buying back my DNN position fairly soon.

In the US the developer closest to production, [besides Peninsula that is temporarily on care & maintenance], is Uranium Energy Corp (UEC). UEC had done some trial mining a few years back, but mostly have just worked on permitting their ISR deposits around their processing center in a hub and spoke pattern in TX, and have a few projects in WY, NM, CO, etc… They also bought 2 big ISR projects in Paraguay, but I’m not sure what the timeline on bringing those into production is. Many knock UEC because the ceo Amir Adnani is seen as a blowhard, hanging with Katusa & Rule & Casey, but at least he gets out there and promotes, and since they are dual-listed, they have far more liquidity for trading in and out of their stock, so I like trading around my UEC position.

(AZZ) (AZZUF) Azarga Uranium Corp will be up to bat next for ISR production in the US after UEC, and is well along the way in development and is a solid pick for future production. I’ll likely add some Azarga to the mix soon as well.

The next closest US developer to go into ISR production (after UEC and AZZ), is the often overlooked (AEC) (ANLDF) Anfield Energy Inc. AEC bought up most of the US-based U assets from Uranium One, that everyone was so stirred up about in the Clinton scandal. What is funny is if people were so worried about these assets leaving, then why didn’t they give a care when the assets came back and are now, once again, controlled by a Canadian entity. Uranium One has already got agreements in place to process Anfield Energy’s ISR projects once it makes economic sense to do so at their mill that is on care & maintenance. In addition, AEC also has one of the few permitted hard rock mills in the entire US, with the only active one being with Energy Fuels. That is why I selected a position in them, because of the major partner with Uranium One and pathway to production, and their mill, which would need to be refurbished, but they are nearly impossible to permit these days so that gives AEC a huge advantage strategically.

(LAM) (LMRXF) Laramide Resources has a few nice development/exploration projects that they picked up from Uranium Resources (before URRE went into Lithium, shelved their Uranium projects and became Westwater Resources WWR). I sold URRE back in the early 2017 surge in Uranium miners because I was pissed they sold their assets to Laramide, and jumped ship to get into Lithium as the bubble was bursting and with no history of Li mining but decades of experience with Uranium production in previous cycles. Now I’d rather own (LAM) Laramide since they have the goods.

(WUC) (WSTRF) Western Uranium& Vanadium has some of the properties spun out from Energy Fuels, since CEO George Glassier helped build (UUUU) back in the last cycle, and had some interesting ablation techniques to upgrade their ore, but the process got blocked by local opposition, and they ran into permitting issues on their mill, and I’m not sure where things stand now, but they may still surface as a developer.

There really aren’t any other good developers in the US besides UEC, PEN.AX, AZZ, AEC, LAM, and WUC.

As for Canada, the main developers with a chance to get into production are DNN, NXE, and FCU.

There are the Aussie developers Bannerman, Boss, the Spanish developer/producer Berkeley, the Peruvian developer Plateau Uranium, and the African developers GXU and DYL.AX, but I’m not the biggest fan of those.

The rest of the Athabasca U stocks like Canalaska, Purepoint, UEX, ALX Uranium, Isoenergy, Fission 3.0 corp, Skyharbor, etc… are really still exploration companies trying to prove they’ll have an economic deposit for a major to develop, but really the world is awash in Uranium discoveries, so the explorers are much further down the food chain for me personally. That doesn’t mean that the explorers can’t move bigly on good news like IsoEnergy after their initial exploration success, or Purepoint’s discovery success on trend with Fission and Nexgen. Like all explorers they can really run hard while they have the wind in their sails.

_______________________________________________________

Currently my Uranium holdings are as follows:

(UUUU) – Energy Fuels – Producer

(URG) – Ur-Energy – Producer

(UEC) – Uranium Energy Corp – Developer with a processing center

(AEC) – Anfield Energy Inc – Developer with access to processing & hardrock mill

(NXE) – Nexgen Energy – World Class Advanced Exploration & Development project

________________

My next acquisitions will be:

(DNN) Dension Mines – closest Canadian Developer to ISR production, 20% interest in one of the 3 Uranium Mills in Canada, consulting for Uranium Participation, remediation business, strategic position in GXU

(AZZ) Azaraga Uranium – Near term ISR Producer in US

(LEU) Centrus – Uranium enricher/processor/reseller in US

(LTBR) Lightbridge – Nuclear fuel rod cladding – better fuel, avoids meltdowns, more efficient, and they have the French nuclear giant Orano (formerly Areva) as partners

(ISO) IsoEnergy – best Uranium discovery of 2019, and connected to team at Nexgen

If money allows, then I’d grab (PTU) Purepoint or (SYH) Skyharbour. SYH is more of a Uranium Prospect generator, like UEX or CVV.

That’s my 2 cents on the Uranium Miners, but everyone has their own approaches, goals, biases, investing rules, and perceptions on any sector.

Ex:

And a great Rant it is/was. I printed it out, read about them all last weekend and made some choices. Thanks!

Thanks David. My hope is that a good rant gets some thoughts going for other, I like to periodically crystallize my thinking more and after typing out a stream of consciousness rant, I realize why I’m holding certain stocks, or why I want to acquire other ones. Also, I’m always curious what other companies or macro thoughts others have in any given sector.

Thank you Excelsior. My uranium holding are more on boring Cameco and I do hold significant among of Denison,UEX,URE,UEC,EFR,CVV,SYH,PDN… I am betting on the price rise in the next two years. But according to Rick Rule, the rise will be much slower than we hoped, unfortunately.

My holdings are mostly Canadian stock and focuses on Athabasca Basin

It seems Nexgen is a good uranium company which I never pay attention to. I have put a low ball bid for now and will do more research on it.

Dragonite – Nice uranium stock picks. I think you’ll do very well as the price recovers, and again I don’t hate Cameco or anything, it’s just a bit large and clunky for me and I think they’ll have underground water issues to contend with because they are going so deep at this point in both their mines.

DNN Denison is a solid company and pick for all the reasons previously mentioned above and is one I’ll be adding back next.

CVV Canalaska & SYH Skyharbour are both interesting U explorers and really more Prospect Generators with many JVs with larger companies. This diversifies their risk across more assets, and gives them a good potential of finding something valuable, or having one of the larger companies of eventually take them over.

UEX is similar with a few JVs, but they actually do a bit more of their own exploration work each year and have high torque when things are going good and the U space. Still they don’t have anything very close to development or production at this point after over a decade.

If you like the Athabasca Basin, then it doesn’t get much better than Nexgen (NXE). They have the best undeveloped asset in the whole area with the high grades like those of Fission’s or Denison’s hardrock projects, but due to their location underground in the sandstone, none of the underground water issues that plague other projects in the Athabasca, where they have to do freeze walls etc…

Nexgen (NXE) will be the most coveted asset, with solid economic studies completed, the underground inclines in place, and likely will be bought by one of the larger companies like Cameco, Rio, BHP, etc… They are dual listed now, with decent liquidity, their resource will get treated much higher as the spot prices move higher.

There are a growing number of investors that feel for Cameco to save their rear ends, that they are going to have to purchase Nexgen, and put that deposit into production before trying to salvage their 2 older deep mines. Despite the cost to develop Arrow at Nexgen., the return on investment for Cameco would be so much greater for the long term, than all the work that they’d have to do down in Cigar Lake ore McArthur River.

The other theory investors have is that eventually a company will buy both Fission and NextGen, and combine them both into one massive company. This of course drives the Nexgen. Investors crazy because they love to hate on Fission, but it is an interesting idea to consider and I wouldn’t rule it out completely.

Hey Ex. I saw your comments regarding orezone yesterday. yes its nice to see it trending higher. You brought my attention to it at just the right time. as I said I bought the warrants since they are good til 2023 and by then it will either be taken out or producing. already doubled. The other gold I own that’s looking nice is pure gold. The volume was over 3M yesterday. there are .85 warrants expiring in a couple of weeks so once that overhang is gone I see no reason for it not to get into $1+ range. especially since they will be a producer this year if all goes well

Hey Wolfster – Congrats on the Orezone warrants doubling man! That is awesome, and you were spot on. I only hold the general shares in Orezone but have been pleased with the steady rise as it is starting to get re-rated for their producing mine and their exploration success at their 2nd development project = Mine #2.

As for Pure Gold, yes, I’ve been sitting on my shares wondering when the higher gold prices were going to be factored into their economics being so much more robust, and it finally has started to move after flat-lining during the boring “orphan” phase of a development project and is now heading towards their “Golden Runway” phase of development into first production. Bring it on!

I clearly have not woken up yet this morning, as my comments above about Orezone were meant to be about Roxgold, also in West Africa (regarding mine #1 and development of mine #2).

I know Orezone is a development project, and just got my wires crossed mentally with Roxgold for some reason. The whole reason I bought into Orezone was when they tanked after needing to restate their resources after their 1st economic study was released, and the market over-punished them for this 2 years back. Most sane investors realized they had a great resource there, but it just needed to be adjusted, and I really respected their team for stating they didn’t have confidence in the block modeling, and were going to completely redo their resource estimate and do more definition drilling to fill in the gaps.

Now, fast forward 2 years and their economic studies are much tighter than most companies, and I have so much more confidence in their project after being double-sure that it is a go, and far prefer a company delaying going into development, construction and production until they have the details worked out correctly. Now Orezone is set to jet and will have very economic mine in West Africa and I believe that makes them a key takeover target from one of the larger mining companies, or they’ll bring in the operations team to move it forward on their own. Either way (ORE) has a winner on their hands and it is one of the better development projects on the market today.

(ORE) (ORZCF) Orezone Corporate Presentation – April 2020:

“Developing the Low Cost, High Margin Bomboré Gold Project”

https://orezone.com/site/assets/files/5476/2020-04-17-_orezone_corporate_presentation_web_na.pdf

(ROXG) (ROGFF) Roxgold Inc – Corporate Presentation May 2020:

“West Africa’s Next Multi-Asset Gold Producer”

https://s22.q4cdn.com/726251528/files/doc_presentations/2020/05/Investor_Presentation_-_May_2020.pdf

A few investors used to meet on Fridays below TD bank on Bay and King Street and the running jokes were Pure Gold which had the nickname of Poor Gold and Alamos Gold was called Almost Gold. It always made me laugh, but things have changed. DT

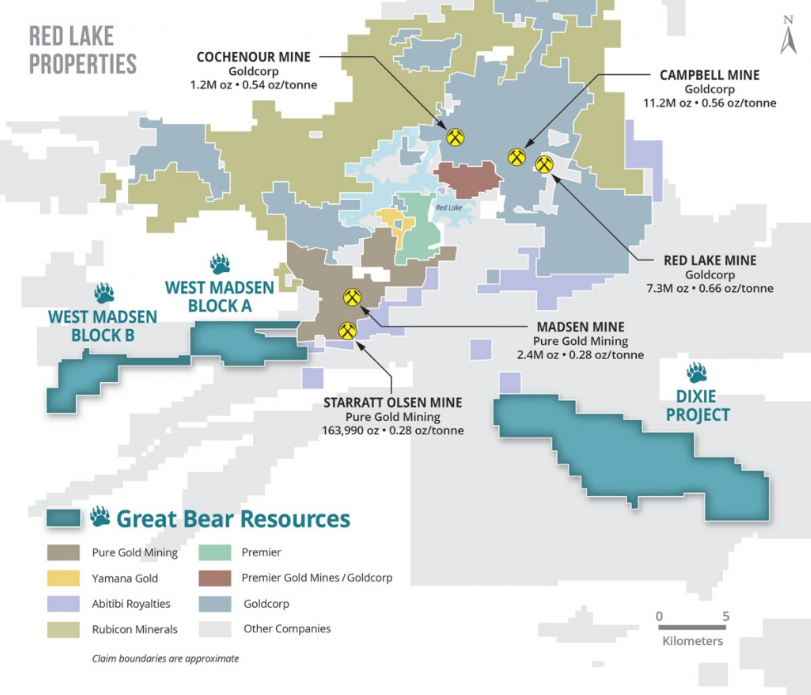

Yeah, Alamos Gold is a solid Mid-Tier Producer now with great costs, and Pure Gold is one of the more attractive development projects in Red Lake, and is neighbors to the very popular Great Bear Resources.

I’m also a fan of Mark O’Dea and his Oxygen Capital Corp, currently the team behind Pure Gold, Discovery Metals, Sun Metals, and Liberty Gold.

With regards to (PGM) (LRTNF) Pure Gold, here is their latest Corporate Presentation:

“Welcome to the heart of Red Lake. Canada’s Fort Knox.”

Here is a good map of Red Lake, that shows Pure Gold sandwiched in between Great Bear Resources on one side, and the Red Lake Mine that Goldcorp sold to Evolution Mining a few months back. Premier Gold is also squeezed in there as well.

Red Lake is definitely the right area for high grade gold mining:

https://static.seekingalpha.com/uploads/2019/2/11/13760932-15499227679255633_origin.png

{kind=link}

You follow way more plays than I do Ex so I’m sure it gets easy to get them confused with one and other…..Im pretty sure you’re confusing Orezone and Roxgold(which I own as well and I think it was you who pointed me in that direction as well.lol)….Roxgold will be releasing first quarter results on Tuesday and has been getting stellar drill results on its seguela project that should have a PEA in the second quarter…..

my slow typing shows up as you’ve corrected yourself in a longer post and in quicker time. lol

Haha! Thanks for having my back Wolfster, regardless. Much appreciated.

Yeah, I have a lot miners juggling around for position in my mind, and I do it mentally by region and just had Roxgold interfering with Orezone for some reason when I was typing that response. After I submitted the comment and actually read what I had written, and I shook my head and thought, I’m talking about the wrong damn company, but it took seeing it in writing to wake up my synapses.

Sorry a simple response about Orezone has gotten a bit messy and convoluted now. 🙁

no worries here EX….your mention of both of these has lead to green on my screen . 😎

Nice. I love green on the screen!

https://www.profitconfidential.com/wp-content/uploads/2019/09/iStock-896259360.jpg

{kind=link}

Wolfster – Congrats! When I saw your note about the warrants I thought about purchasing some, but wasn’t sure if I could in my Schwab account. If you come across any other warrant Oferings that look juicy please let me know.

No problem Charles. I don’t come across many and I can’t say whether you can buy them through Schwab…I will say they are usually either on the tmx venture or the cse exchange……….and usually requires Ex steering me in the right direction.😎

Next week looks like it will be a good one for silver and the miners, silver juniors in particular.

https://stockcharts.com/h-sc/ui?s=%24SILVER&p=D&yr=1&mn=5&dy=0&id=p85486604946&a=647228156

Back-to-back daily closes above the 50 day MA for first time since February:

https://stockcharts.com/h-sc/ui?s=%24SILVER&p=D&yr=1&mn=0&dy=0&id=p10085360662

SILJ: The daily chart does not look great for new buying…

https://stockcharts.com/h-sc/ui?s=SILJ&p=D&yr=1&mn=2&dy=0&id=p36023689790&a=726315882

But the weekly chart is just getting started and shows room to run much higher…

https://stockcharts.com/h-sc/ui?s=SILJ&p=W&yr=5&mn=7&dy=0&id=p07943400288&a=724116257

Important resistance just above…

https://stockcharts.com/h-sc/ui?s=SILJ&p=W&yr=4&mn=5&dy=0&id=p72358252604&a=716410329

Weekly close above 30 week MA which is pointing up:

https://stockcharts.com/h-sc/ui?s=SILJ&p=W&yr=4&mn=5&dy=0&id=p10769891142&a=751750067

Positive speed line and Fibonacci fan action:

https://stockcharts.com/h-sc/ui?s=SILJ&p=W&yr=4&mn=4&dy=0&id=p04047096180&a=632309494

Pitchfork, MA, and Fibonacci resistance just above for silver:

https://stockcharts.com/h-sc/ui?s=%24SILVER&p=D&yr=1&mn=2&dy=0&id=p17295768867&a=751756191

SILJ is bullishly leading silver:

https://stockcharts.com/h-sc/ui?s=SILJ&p=D&yr=1&mn=2&dy=0&id=p87331419596&a=751760176

I hope you are right. My silver stocks all look pretty coiled.

Don’t tell anyone but I couldn’t be more bullish. It still might not be easy in the short term but everything is shaping up very well. How silver performs versus gold is more important than how it performs versus any currency and it now looks ready to move up.

Silver:Gold just closed above the 50 day MA for the first time in four months and above the upper Bollinger Band for the first time since last year.

https://stockcharts.com/h-sc/ui?s=%24SILVER%3A%24GOLD&p=D&yr=1&mn=0&dy=0&id=p68700019003&a=751955672

The quarterly charts for the $XAU and $GDM/GDX haven’t looked so good in more than 15 years. They are now above the 50 quarter MA for the first time since Q1 2013 and are well above their quarterly Bollinger Bands which are pointing up. If we get a quarterly close above the upper BB, it will be the first time since 2010. In addition, the quarterly RSI(14) just broke out to a new 8 year high while indicators like the MACD and various Stochastics look excellent. Quarterly Ichimoku Cloud resistance is just above which NEM has already defeated. More surprisingly, even PAAS has defeated it. That’s a bit of a shock considering how far silver is behind gold technically. Even Barrick hasn’t matched PAAS (or NEM, of course).

I believe the miners will now do a lot of catching up to king gold and gold looks better than ever from a quarterly perspective. It is working on its 5th straight quarterly close above its quarterly Bollinger Bands and now sports a quarterly RSI(14) reading above 70. Sure, that RSI reading could soon be multi-month dangerous as it was in 2004 but I think the odds favor what Q3 2005 kicked-off: a 30 quarter/7+year stretch in which that reading remained above 70 and even hit 95. The yearly chart is slightly more overbought with a yearly RSI(14) reading of 73. It remained overbought along with the quarterly chart last time and reached 90 when it peaked over 8 years ago. The yearly upper Bollinger Band is now at 1922.65, just $1.05 away from the all-time high and I bet gold will get there this year.

I really would not be surprised if gold were to take out its all-time high in the next 4-6 weeks but I don’t hope for that.

I’d rather see the miners do more catching up to gold first, as you mentioned above, before seeing gold making any more moves higher. While I believe that event of taking out it’s all time high will get more attention on the PM sector, it would be nice to see the miners move a bit first before the masses wake up what is going on.

Yes, since real gains are best measured in gold, I want gold to stay where it is as the miners price-in their new bullish reality.

I really don’t care what comes first. The golden goose or the golden egg as long as I’ve got a basket full…………lame attempt at the chicken/egg argument…….bottom line is I hope to see $2,000+ gold this year cuz I know my PM stocks will fly for sure too..

Best daily and weekly close since early March for the silver-gold ratio:

https://stockcharts.com/h-sc/ui?s=%24SILVER%3A%24GOLD&p=D&yr=1&mn=2&dy=0&id=p56176806415&a=751766353

An interesting micro cap prospect generator with tight share structure, 63 million, RRI,

Riverside Resources. For the long run of this bull market.

https://www.mining.com/rick-rule-buying-this-may-be-the-best-opportunity-in-exploration/

Rick Rule’s family trust owned 6% of RRI 8 years ago:

https://microcapclub.com/2012/08/prospect-generators-the-mining-worlds-sleeping-giants/

Outstanding shares at the time was just 35M.

Mr Rule is of course biased when he recommends it to be maybe the best opportunity in exploration but It could very well be this time when the golden bull is continuing and getting more aggressive.

Hi Blue, I don’t know about it being the best exploration property when there are so many other whoppers out there like Walbridge , Great Bear, Lion One, Irving, Auryn, Adriatic, Osisko Mining, or even some of the recent results at Freegold Ventures or other new grassroots discoveries.

I believe what Rick Rule liked was with a prospect generator spreading the risk over a number of different targets, and just like any of the prospect generators, having other companies foot the bill for the exploration costs. I like the management team at RRI and feel they have a disciplined approach in discovery and being frugal with their money. I wish you well in that investment and have considered a position myself.

Which of their target properties do you feel is the most prospective?

Their 100% owned Los Cuarentas silver project in Mexico, located just 17 km from Silvercrest Metals’ Las Chispas project looks very interesting. We all know Silvercrest Metals success. Also RRI partnership with BHP is in the right direction.

Thanks for the heads up Blue. I’ll check out their Los Cuarentas silver projects, because if it is on trend with Silvercrest’s Las Chispas, then it could be quite prospective if the mineralogy is the same. SILV definitely found the goods at their project, so if it is similar, then it could be a solid exploration target.

Yes, having BHP is definitely partnering with one of the “big boys.”

Thanks Blue. Yeah sandwiched between Premier Gold and Silvercrest is a good place to be, and I noticed Adrian Day had a sizeable position as well. I didn’t realize Riverside had picked up those properties from Millrock (another good prospect generator). I’ll be keeping a closer eye on Riverside now and appreciate the heads up.

I have been watching the price of helium rise due to shortages. I like Desert Mountain Energy (V.DME)a primary stand alone producer with a low share count. I haven’t purchased any yet but might buy a few shares of DME just to keep my end in so I don’t forget about them. Recently Stockhouse did an interesting write up on Desert Mountain. If you are interested in shortages and potential upside this article is a good read. DT

https://stockhouse.com/news/newswire/2020/05/05/tapping-into-potentially-world-s-best-helium-resource

I also looked at American Helium (V.AHE.H) and Royal Helium, both junior explorers but not worth the mention. DT

DT – Hope you have a gas!

Thanks Ex, me too, ever upward! LOL! DT

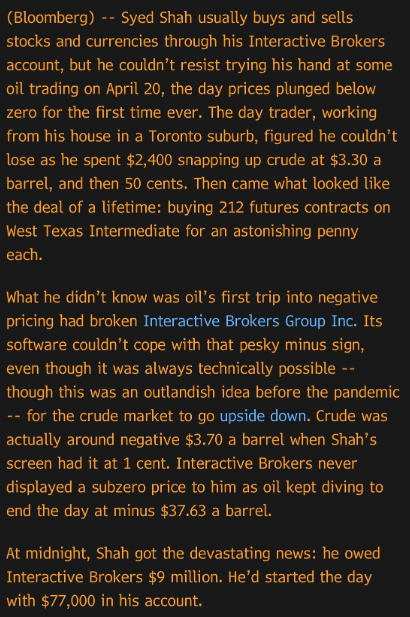

@Goldfinger – Welcome to 2020 ~~~>

“Daytrader with $77,000 account loses $9,000,000 in a single day” [Gadzooks!!]

{kind=link}

Losing 9 mil when you really don’t have it near by seems like it would be somewhat stressful.

+9

Stressful? naaa pocket change.

The inevitable is happening here and now, people are boasting how they just walked away from a cheap condo ($1 million+ these days) that is in construction but has already lost 20%. That means their $50,000 plus down payment is gone but what they don’t want to know is that you can’t declare personal bankruptcy on mortgages, and they are still on the hook for the difference their unit eventually sells for. DT

I guess the lesson is don’t buy anything anymore unless you can pay cash. Then wait to see how long before the bankruptcy rules change. One thing probably won’t change is the banks will not be on the wrong side of things.

Jim Paterson: Start Paying Attention to the Junior Miners Before its Too Late

https://www.youtube.com/watch?v=j8QAGL6XVGE

This evening I am going to have Sunday dinner with some craft beer. This Sunday also happens to be Mother’s day, Sunday always comes to mind because Sunday dinners are a family event around here. DT

The only concern I see going forwards for the PM’s is that seasonality is working against a breakout. In fact a pullback/ consolidation into the summer would be the norm.

I think the usual seasonal factors will continue to take a back seat to the developments in stocks, bonds, and the gold sector over the last two years.

The “sell in May” crowd was very wrong last year and I bet it will be wrong this year.

Most people believe that the virus was/is the biggest problem for their stock and bond portfolios but they are wrong. There is little chance that the stock bear has seen its low and big money knows it so gold will have a strong bid year-round from here. Of course it will still get ahead of itself and correct sharply but I doubt that action will follow past seasonal patterns with any consistency.

China and India suffered huge year-over-year collapses in demand in Q3 last year and gold didn’t care because big/smart money didn’t need the virus to know that a bear market was a certainty.

Q3:

China: -12%

India -32%

https://www.gold.org/goldhub/research/gold-demand-trends/gold-demand-trends-q3-2019/jewellery

The only flaw in your logic is that I’m onside with the big money…..let’s hope big money is able to overcome the contrarian indicator

My point was simply that such a decline in demand from China and India would have had a negative impact in the past. Today, gold is still about $150 above its Q3 peak and even the plunge in March ended above Q2 levels so it wasn’t dumb money that caused gold to rise in the face of falling Chindian demand.

Gold is now in a situation that cannot be compared with any other in modern times, if ever, so I will be surprised if seasonal patterns hold up in any useful way.

It looks like gold has been forming a bullish pennant for the last month but even if that breaks down, it probably will find support around 1650…

https://stockcharts.com/h-sc/ui?s=%24GOLD&p=D&yr=1&mn=1&dy=0&id=p25644963912&a=752776781

I’m hoping that bullish pennant breaks to the upside and gets up into the $1800’s and maybe even a run at the 2011 peak of $1921.

Picked up SILV @ $7.07

I’m trying to post this for the 3rd time:

(SOLG) (SLGGF) SolGold PLC Announces Royalty Funding Package for Alpala Project

by @accesswire on 11 May 2020

“The Board of Directors of SolGold (LSE & TSX: SOLG) is pleased to announce that SolGold has entered into a US$100 million Net Smelter Returns Financing Agreement with (FNV) Franco-Nevada Corporation , with an option to upsize the financing to US$150 million at the Company’s election, with reference to the Company’s flagship Alpala copper-gold project and the remainder of the Cascabel license in northern Ecuador.”

https://ceo.ca/@accesswire/solgold-plc-announces-royalty-funding-package-for-alpala

(ADT.AX) Adriatic Metals to Acquire (TETH) Tethyan Resource Corp, Creating a Leading Polymetallic Explorer and Developer in the Balkans

by @newsfile on 11 May 2020

https://ceo.ca/@newsfile/adriatic-metals-to-acquire-tethyan-resource-corp-creating

Matt & Excelsior,

just found some more money since the last time we spoke regarding “safeish” gold investments. Sandstorm has been quiet since I bought it, but I’m not too fussed about that. I see it hitting $14 CND resistance within the next 3 months.

Anyway,

now that I have discovered more money, I would like to move it into some “safe-ish” silver plays (risk is relative!). I own a few hyper volatile silver-exposed juniors like IPT and BBB. The only big silver I own is First-Majestic. Now based on the charts, should I be moving into MAG or PAAS or First Majestic? I’m leaning towards MAG right now…as it is down %5 today and rockets when silver jumps a few bucks at a time. I would be open to any great 4-10 CND$ safish-ish silver plays too if they exist. There seems to be only a few great ones out there. Sometimes less choice makes life easier:) Any thoughts on the above would be appreciated.

Alexco- AXU- will be the purest silver play if/ when they get their water permit. Looks like production now is 2021 as they were hoping 2H/ 2020

Agreed Marty. Alexco is a great pure play development company moving towards production, and continuing to nail their exploration as well.

Hi Confused – I don’t usually use the word “safe-ish” with most mining stocks, especially the volatile Silver stocks, but as mentioned above with Alexco, or you comments regarding Mag Silver, (and this would apply to Silvecrest as well), these developers have known ounces in the ground that will get rerated higher as Silver prices run higher. So AXU, MAG, SILV are all “safe-ish” speculations.

As for the producers you mentioned First Majestic and Pan American. Both definitely have jurisdiction and operational risks, but they are solid companies and have mostly Silver exposure. Fortuna (FSM) would be a relatively “safe-ish” play as well in the medium-sized producers.

Most of the other larger Silver companies are more base metals conglomerates, like Hochschild, Sierra Metals, and Fresnillo, or have gone more Gold focused than Silver, like Hecla, Coeur, SSR Mining, or even Wheaton Precious Metals.

My largest Silver producer position that I feel is relatively safe is Silvercorp (SVM), since they have such low costs and AISC, from their 2 mines and base metals credits, but some don’t like that they are operating in China, and that is likely why they are trading double where they are now. They are in the process of taking over (GUY) Guyana Goldfields to expand into gold production, which appears to be the trend lately, (as noted above). This increases their South American exposure, because they also own about 28% of the Silver explorer (NUAG) New Pacific Metals in Bolivia.

(USAS) Americas Gold & Silver is also one of my larger Silver & Gold positions, and their asset mix is turning from more base metals production (Zinc/Lead/Copper) to more precious metals production with 75% of production in 2021 slated to be from Gold & Silver. I feel it safe-ish, but could really run more than some of the more bloated larger companies.

Personally, I’m not in the Silver miners for safety, and like some of the more full throttled and highly torqued smaller producers like Impact, Santacruz Silver, Excellon Resources, and Endeavour silver. I also have a number of Silver developers like Alexco, Bayhorse, Kootenay Silver, Discovery Metals Corp, and Orex Minerals. Lastly I have a few irons in the fire with riskier explorers like Dolly Varden, Vizsla Resources, Metallic Minerals, Brixton Metals, and Defiance Silver.

There are some other interesting companies I didn’t mention, but that’s the general idea.

Am I missing something? Silver will account for 70%+ of AXU’s revenue while zinc and lead will account for the rest. IPT, on the other hand, saw 95% of its 14 years of revenue come from silver. For Q3 last year, it was 89% silver and 5% gold with the remainder coming from zinc and lead.

The RSI is not confirming the recent price gains so it will remain vulnerable to a short term pullback until the RSI makes a new high (green line):

https://stockcharts.com/h-sc/ui?s=AXU&p=D&yr=0&mn=11&dy=0&id=p32724721063&a=709369195

For the record, I do agree that AXU will perform very well whether I am missing something or not.

That is correct Matthew, so I don’t see you missing anything. You may be responding to Marty’s comment about it being the purest Silver miner, in your response, where you are correct that Impact is more pure. However, I believe Alexco’s silver Concentrate is the purest in the world, with the least smelter penalties and it is their combination of Zinc and Lead concentrates being so “pure” that has smelters fighting over it to be able to blend with other companies concentrates. Maybe that is what Marty was referring to.

________________________________________________________________

Like you, one of the big appeals to me as an investor in Impact Silver is very pure exposure to Silver on a percentage basis — more so than any other producer.

However, for most of the remaining Silver-focused Producers like First Majestic, Santacruz Silver, Excellon (prior to recent Otis gold acquisition), Fortuna, Endeavour, Hochschild, etc.. they are doing good to produce 60-70% silver, so Alexco doing 70% in Canada, versus being located in Mexico.

The other positive for Alexco is their lower AISC than most of the above-mentioned companies at an all-in sustaining cost of $11.94 per ounce of Silver all in. So when one factors in a new primary Silver producer, with a low AISC, and couple that with the fact that their mill is built and the inclines have been dug into Flame & Moth and Bermingham, then it makes Alexco one of the most attractive and “safe-ish” Silver miners out there.

Silvercorp is my largest Silver position, but Impact Silver and Santacruz Silver are in 2nd & 3rd place as the 2 highly torqued smaller silver producers on steroids, and Alexco is in 4th position as my favorite Silver developer hands down, and then Americas Silver is in 5th position as hybrid Silver/Gold/Base metals company.

I bought a chunk of Alexco recently. Looks goooood!!!

{kind=link}

Hello Fleck,

No link to the TRISTAR presentation.