Doc’s thoughts on the gold market

Doc and I recorded this interview right before the tweet by Trump regarding more tariffs on China. This tweet drastically swung the markets but the long term picture we discussed remains the same.

There are several errors in that article by Jeff Thomas. First, when you deposit money in a bank, you are loaning your money to the bank. There is a debtor-creditor relationship. When you deposit your money in a bank, the ownership of your money really does not change. It is the control of your money that changes. Thomas says “if you deposit money in the bank, it becomes the property of the bank”. Sure, your deposits becomes the property of the bank in the sense that it is in their possession which means that they have control of it but that is not the same as actually owning it outright. The same is true when the bank loans you money. That money does not belong to you. It is the banks money which you are legally required to pay back. People mistakenly believe that if your money is listed on the bank’s balance sheet as an asset then your money is no longer your money but legally belongs to the bank. I disagree with them. If that was the case then why can depositors file a claim as a creditor to get their money back when a bank becomes insolvent. After all, if the depositor’s money no longer belongs to them then they should have no right to try to take money that legally belongs to the bank. The same is true if I close out my checking account. If that money does not belong to me then why is the bank required to give me money that is owned by the bank? If I loan my brother $10,000 and he puts it in his safe, is that still my money or is it now his money? It is still my money even though it is in his possession. Now if he were to die my money would be listed as an asset of his estate. I, of course, would have to file a claim against his estate to get my money back which I am legally entitled to do.

Thomas is also wrong about Greece freezing all bank accounts. No bank accounts were frozen. What they had was certain restrictions (capital controls) on the money that was in bank accounts. Depositors could still make online electronic transfers inside Greece just as before however depositors were limited to the amount of physical cash that they could withdrawal to just €60 per day, per account holder, and per bank.

Thomas also wrongly states that “a law was passed in 2010 that allowed any bank, if it declared a bank emergency, to confiscate deposits”. That is false. Banks have no authority to confiscated deposits (bail-in). It is the banking regulators like the FDIC that have the authority to do bail-ins but only for financial institutions deemed to be systemically important which would exclude most banks.

cfs, when it comes to credit unions, I see very little difference between banks and credit unions as a whole. The larger credit unions have derivatives. Also while credit unions do make local mortgage loans they also have a good amount of auto loans and unsecured loans, some of which are sub-prime. They also have the same regulations as the banks including Regulation D which allows banks and credit unions the right to require at least seven days written notice if you wish to withdrawal money from certain types of accounts like money market accounts or savings accounts. In fact some credit unions even say that they have the right to require up to 60 days notice for certain accounts as seen in the example below:

“We reserve the right to require you to give not less than seven (7) and up to sixty (60) days written notice of your intention to withdraw funds from any account except checking accounts.”

https://www.usccreditunion.org/wp-content/uploads/disclosures.pdf

And back in the 2008-2009 financial crisis the four largest corporate credit unions failed. These corporate credit unions are sometimes referred to as “the credit union’s credit union” since they provide liquidity, investment and payments services to credit unions. Also back then the National Credit Union Share Insurance Fund (NCUSIF) went broke.

Yeah, the bankster class knows…

“The secret to success is to own nothing, but control everything.”

—Nelson Rockefeller

WOW. Great post JMILLER. Your posts always containing good facts. We need you to post more often.

US Dollar- Gold relationships.

https://www.youtube.com/watch?v=3SFAXjsSC0c

Note that BOTH Gold AND the US Dollar ARE SAFE HAVEN ASSETS at this time.

(No inverse relationship at the moment)

The dollar is only rising because inferior currencies are falling faster. In real terms, the dollar is falling and is therefore no safe haven except in the very short term.

Lookout below $USD to $.94

If it goes there, it will likely go lower…

https://stockcharts.com/h-sc/ui?s=%24USD&p=W&yr=3&mn=3&dy=0&id=p00295462014&a=672280269

You may be right Matthew. But does not “inferior currencies are falling” imply strength in dollar, and is not “strength in dollar” possibly a move to safe haven?

Certainly the dollar is not rising because we have a trade surplus…..we have a large trade deficit.

Cklearly both the dollar and gold are volatile on a short term basis. On a short term basis they do NOT show a correlation.

However, over the last year, it is very difficult to explain the rising trend in BOTH dollar and gold except as a move to safety, on top of the usual inverse correlation.

Relative strength is not the same actual strength. Falling less quickly is not the same as rising. The dollar index rises even if all the dollar is doing is falling less quickly than the euro, etc.

Other than inflationary changes in purchasing power, I guess I do not understand the difference between relative strength and actual strength.

MATTHEW, I have done a series of calculations, intended to show safehaven effects in US dollar using the US $ index and the WSJ US $ index and gold price, including deviation error analysis and my conclusion is that the variability is too large to obtain any safehaven data, which depend much too much on starting and ending points.

(The possible error range signic\fically exceeds effect !)

Purchasing power is the heart of the issue. The dollar can be relatively very strong if measured in a plunging currency yet actually very weak when it comes to holding purchasing power.

Beginning in 2014, its relative strength was accompanied by actual strength. So much so, in fact, that it made gold appear weaker than it really was. In other words, the real price of gold (gold vs real stuff, not paper) remained higher than its dollar price action might have led you to guess. Why? Because the dollar didn’t rise only against gold, it rose against all commodities along WITH gold but to a greater extent. So gold actually soared vs commodities yet still appeared to fall in value because it is priced in a currency that had outperformed commodities by an even larger margin. The real price of gold went up while the USD price of gold went down. The opposite happened in the mid-2000s; the dollar made gold look stronger than it was. Gold was actually doing poorly vs commodities at the time which is why the gold miners did poorly overall vs gold. For example, gold bottomed at roughly 6 barrels of oil per ounce in 2005 and peaked at under 12 barrels in 2007. The 50 year average is about 15 and it hit 43 barrels in 2016. Today, it’s 26 barrels.

The gold miners fell more than 80% vs gold between their 1996 peak and 2015 trough and the low real price of gold for much of the period is the reason. Despite quintupling vs the USD, gold wasn’t particularly strong most of the time, the USD was weak.

The USD price of gold says a lot more about the USD’s health than it does about gold’s health.

If the USD index measured real value rather than relative value, gold would be around $330 today. That’s what gold was in March, 2003 when the USD index was trading at the same level as it is now.

The bottom line, never mind the USD as portrayed by the USD index, if gold is going up, the USD in your pocket is losing purchasing power. The USD index is a smokescreen for a massive and relentless wealth transfer.

Keep in mind that it is also possible for the dollar to rise in real terms even as the dollar index falls. This would happen if it were to rise versus gold while still underperforming the euro. It happens.

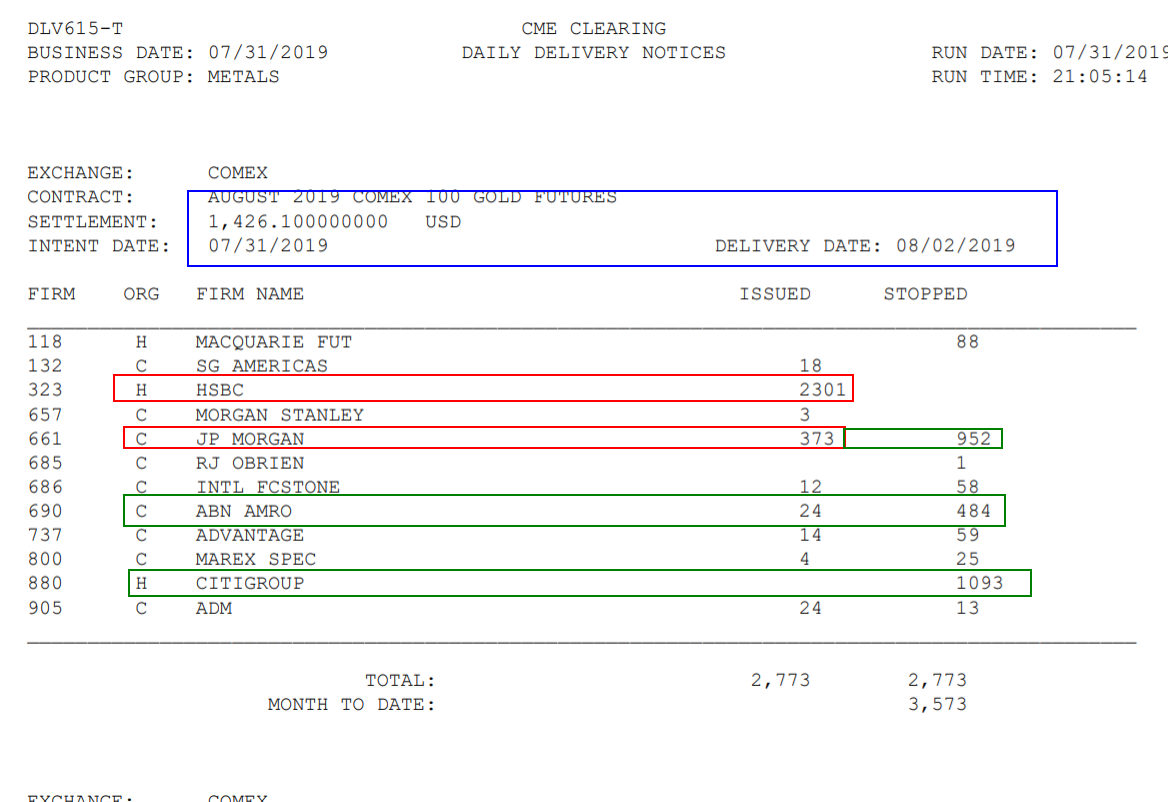

CitiBank was rumored to be a big Bank gold short, doing exactly the OPPOSITE of all other reporting banks. They were grabbing fistfuls of gold contracts the past few days, as you can see on the CME clearing report below.

https://4.bp.blogspot.com/-RpnRlAJkJk4/XUNI4EMoLhI/AAAAAAABboM/QKr0Z_1lb5cUK0GORlp9M6vSHmOuPcuMQCLcBGAs/s1600/cmeclearing1.png.PNG

{kind=link}

(makes you wonder about insider info?)

I wonder if Seth Rich will be named.

Doc, are you going to cruise down the Mississippi next week? I bought some MAC@32.25 today. It owns premium grad A shopping malls and turned down a buyout@ $95 from Simon SPG a couple of years ago. it goes ex on Aug 16, so if you buy now you’ll get 3.75 in dividends in the next 54 weeks, a yield of over 11% How much lower do you think it will go? Bon voyage!

https://www.youtube.com/watch?v=tDo40HN_sko

USAWatchdog

METALS REACT TO FED SHOCKWAVES – READY FOR NEXT MOVE

August 1, 2019

https://www.thetechnicaltraders.com/metals-react-to-fed-shockwaves-ready-for-next-move/

Thanks………silver has a little more work to do…….long term looking good……jmo

Gold hit an all time high for a few minutes in canadian yesterday, today its decisively higher.

I guess were on our way to the moon.

Finally… one giant leap we can believe in.

Looking good……

CFTC……got a new director……not that it matters….news at GATA…

Maybe, ……..Trumper needs the rule of law to prevail , so he can get reelected…..wishful thinking on the rule of law….. 🙂

The odds are low that an intermediate term correction is/has begun. In fact, the odds are decent that the low for this pullback happened yesterday (even if we need several more days of consolidation).

Relative to the 377 week MA and EMA, you can see how much better GDX is doing now than in 2016…

https://stockcharts.com/h-sc/ui?s=GDX&p=W&yr=6&mn=11&dy=0&id=p61937299180

Gold is hanging onto that important speed line support for the 4th week in a row.

(It’s also plain to see how important it was to take back that 600 week MA in December. I said so at the time but some weren’t buying it!)

https://stockcharts.com/h-sc/ui?s=%24GOLD&p=W&yr=6&mn=0&dy=0&id=p43119101345&a=613254309

https://youtu.be/hsCaNFO-6jo?t=13

Ira’s morning

Soros must be stopped

From the LEFT coast there is an extremely worrying attempt to destroy democracy.

Much of the leadership of Silicon Valley is far left wing atheist and totally determined to change politics in the US towards socialism.

From Facebook, twitter and almost ALL of the social media firms there is a conspiracy to fox the 2020 election by non-overt means:

https://www.youtube.com/watch?v=Z5NzDLvVBdA

The use of secretive computer algorithms, social media WILL BE moved leftwards.

Righwing, conservative or Christian leaning material will be demonetized or receive fewer ads, or simply disappear on some sites.

The insidious nature of this socialist/Marxist activity stems from its hidden nature.

Youtube, Facebook, twitter, etc. publish a set of community guidelines, but keep their algorithms that actually do the censorship highly secret.

They will discriminate, but YOU WILL NEVER KNOW EXACTLY HOW OR WHY.

Google is a major leader in this effort to destroy democracy, and defeat Trump in 2020.

For those that believe there will be a banking crisis, this is good reading, even if you know much of it:

http://www.321gold.com/editorials/thomas/thomas080119.html

May I also suggest there is some safety in spreading risk.

e.g. If there is not confication of your money by banks, but a restriction in withdrawals, then spreading out your cash on hand into a number of different banks, might help.

If you relize Credit Unions primarily re-invest deposits into local mortgages, it is possible that credit unions, might be safer than banks.

Regional banks may be safer than national banks.

Savings and loans might be safer than banks.

Spreading out the risk may be safer than all eggs in one basket, even if it is less convenient.

I can guarantee moving any significant amount of US. dollars (more than 5 figures) will possibly prompt an I.R.S. audit, but as long as no laws are broken, an audit is little more than an inconvenient waste of your time.