Hour 1 – Looking Past The Recent Volatility With An All Star Generalist Guest List

This weekend show is packed with generalists all weighing in on where they see opportunities in the markets. I found it very interesting how they are all looking to safe havens as a solid long term play.

Please keep in touch by emailing me at Fleck@kereport.com. I hope you all enjoy this weekend’s show.

- Segment 1 – Mike Larson kicks off the show by sharing the strategies that have been working for his newsletter. With a buy the dip mentality still in US markets there are some other opportunities that he sees as being more opportunistic.

- Segment 2 – Dana Lyons outlines his trading strategy for US markets, gold, and oil. His proprietary risk model is starting to shift for the broad averages.

- Segment 3 – Marc Chandler helps us all take a step back from the recent news and understand how money flows are showing future direction of US markets, gold, and the USD. We also touch on the multitude of news events that will drive markets next week.

- Segment 4 – Trader Vic wraps up the show with a summary of his thoughts on where the markets will move throughout this year.

Exclusive Company Updates This Week

- Metalla Royalty and Streaming – Now Trading On the NYSE Here’s What’s Coming In 2020

- Revival Gold – Recapping the milestones of 2019 and the significant news coming up in 2020

- FPX Nickel – A look ahead to 2020 plans and the potential in the EV market

Good post from @ValueInvest on the symmetrical nature of the Gold recovery, feeding the “U-Shaped” bottom that has been discussed on here a few times.

______________________________

@ValueInvest – “There is an interesting Symmetry occurring in the US $GOLD chart. I drew the middle line at the High of 2016. (1) The Inverse Head-and-Shoulders basing pattern was symmetrical, (2) the breakout at $1,365 was symmetrical, and (3) the AUG-2019 top at $1,565 was symmetrical as well. Will this symmetry in $Gold continue? If so, what are the following targets? If the symmetry continues, then the chart is indicating: (4) a US $Gold price of $1,800 by April-May 2020, (5) then a steep correction down to $1,565, (6) then all-time highs ($1,920) by May 2021…”

http://cdn.ceo.ca/1f1irgl-GOLD%20-%20XGLD%20-%20BRK%20UP.png

{kind=link}

Drivers Behind The Recent Gold Rally

Adam Perlaky – 10 January, 2020

“Gold rallied nearly 4% in December, mainly in the second half of the month, and recently moved to an intraday high of US$1,613/oz as the US-Iran confrontation unfolded. We believe there are a few likely reasons for the move:”

> A technical breakout

> Bullish positioning in derivatives markets

> Light trading volumes

> Portfolio rebalancing at the end of 2019 especially as investors hedged risk asset allocations

> Federal Reserve (Fed) repo activity

> Increased geopolitical risk

https://www.gold.org/goldhub/gold-focus/2020/01/drivers-behind-recent-gold-rally

A Volatile Week for Gold

Gary Wagner – Jan 10, 2020 #TechnicalAnalysis #Chart #VIDEO

“On Wednesday gold traded to its highest level in seven years. After breaking above $1600 trading for a brief moment up to an intraday high of $1613, before breaking and closing below $1600 per ounce. The last time gold was trading at or above $1600 per ounce was March 2013.”

“Yesterday gold traded to its lowest price point this week when on an intraday basis the most active February futures contract hit an intraday low of $1541 per ounce. The greatest price range this week occurred between Wednesday and Thursday resulting in a price range of $72.”

Ira Epstein’s Metals #Video

Jan 10, 2020 – #TechnicalAnalysis #Chart Gold, Silver, Copper, Platinum

Thanks Cory & Big Al for another great week of editorials and the weekend show.

Trader Vic please explain, early in interview your looking for 1750 gold by end year but later in interview you call 1750 in first half of year.???

Bonzo, the R2 Pivot for gold in 2020 is at 1760. If gold exceeds that pivot by 6% like it did in 2019, we will see 1865. That’s a possibility based on precedent not a prediction.

R2 was exceeded by 7.5% in 2011 and 17% in 2006. Going back much further, it was exceeded by 10.4% in 1993, 14.5% in 1986, 160% in 1979, 26% in 1978, 48% in 1973 and 45% in 1972.

I ignored the the years in which there was just a small poke above R2 and notice that it has been 40 years since we had back-to-back years with significant moves above R2 but that happened twice in the 1970s.

https://stockcharts.com/h-sc/ui?s=%24GOLD&p=W&yr=5&mn=0&dy=0&id=p18581607960

Notice the new record weekly volume and back-to-back closes above the Bollinger Bands.

Thanks, Matthew. Makes me glad to have so much gold and silver in my portfolio., about half.

For those that don’t have Platinum, Palladium, and Chrome in their portfolios, (JLP.L) (JUBPF) Jubilee Metals Group is worth a look.

_______________________________________________________

Jubilee Metals – All of the Upside and very little of the down

Crux Investor 17 Nov, 2019

Interview with Leon Coetzer, CEO of Jubilee Metals Group (AIM:JLP)

“Mining but with none of the risks of mining. Tailings is the next big thing in the mining space and Jubilee is set to take the lead.”

“Great set of results yesterday and the announcement of a capital raise of $6.5M to reinvest in to the deliver a raft of new project with 50-75% margins. This group of solid, technical management are starting to scale up and have the capital and people to be able to deliver continued growth for shareholders in a prudent and realistic way. Very excited to see if they can continue this momentum.”

Three Palladium Stocks to Watch as Palladium Hits Record High of $2,139

January 12, 2020 by SSTS Editor

“Spot palladium closed at $2,096 on January 10th, 2020, an year to date gain of 8%. Palladium has done extremely well in 2019, rising 60% in the last 12 months. The majority of palladium’s demand comes from the auto sector as the metal is used in catalytic converters that reduce emissions in gasoline engines.”

“The precious metal is currently benefitting from the overall safe-haven optimism amid rising geopolitical tensions, as well as its own tight supply-demand fundamentals…”

> Palladium Stocks to Watch

– Generation Mining Ltd. (CNSX: GENM)

– Palladium One Mining Inc. (TSXV: PDM)

– Group Ten Metals Inc. (TSXV: PGE)

(PGE) (PGEZF) Group Ten Drills 272 m of 1.90 g/t Pt Equivalent (0.42% Ni Equivalent), Starting from Surface and Including Continuous Palladium, Platinum, Gold, Nickel, Copper and Cobalt Mineralization, at the Iron Mountain Target Area at Stillwater West

December 18, 2019

(PGE) (PGEZF) Group Ten Metals – Corporate Presentation:

Grade. Scale. Location. Infrastructure – Platreef-Style, Bulk Tonnage PGE-Ni-Cu Project – Stillwater District, USA

https://grouptenmetals.com/site/assets/files/3631/2019-1-09_groupten_short_presentation_final.pdf

Thanks, Cory. Thanks, Big Al.

https://www.zerohedge.com/markets/markets-repo-addiction-getting-worse-latest-term-repo-operation

I think most people are stuck in the horns of a dilemma:

Will the liquidity problem cause a monetary collapse, from which I must protect myself, or will people be throwing risk to the wind and this market could still be a runaway. We call that a melt-up and produces prices too high, but we don’t want to miss out on such an opportunity. But then if there’s a shock, we and the market will come back down to Earth . Timing is everything.

I feel exactly like that. However, I’ve felt like that for the last few years, been defensive and paid the price. My gut feeling (contrary to what I usually feel) is that this will be a melt-up year as the central banks will do whatever it takes to keep markets elevated. Yes, the crash will be horrendous when it comes but I think that could be at least 12 months away given they will print and print and print. Therefore, I’m going to invest (aka gamble) 50% of savings on the idea it will be a melt-up. Don’t know what else to do given people who have no concept of risk keep making 30% every year by taking the dumb option

Hi CFS, what do you look at with regard to timing?

As long as the Fed keeps pumping away< I see the stock market rising and the dollar falling and eventually price inflation…… the rate dependent on what other countries are doing.

When I see the Fed stop, I hope I will have mostly cash and real stuff (gold, land, housing, food, etc.) (As insurance, I have enough stuff to provide for the rest of my life anyway, but I don't want to lose the vast majority of my assets which are in the stock market.)

I should add: We are in the LONGEST period of expansion in modern American history.

Experience says this has to end sometime.

The market was up in 2019, not because of fundamental economic growth, but because of liquidity injection.

It is a proven (?) fact that the Fed cannot expand the money supply indefinitely.

The conclusion I reach is that the Fed will slow monetary injection as we approach election time.

I believe this will cause the stock market to fall.

The real question, then, is how much panic will occur.

With great panic, and it does not matter if justified economically or not, could come a collapse.

Thanks CFS, Nigel

CFS:

We are in the most dangerous waters I have ever seen. I am not alone in my view of the danger.

I’ve stated my position but this guy is just about the best I know at thinking.

This Is Nuts & Why We Reduced Risk On Friday

https://realinvestmentadvice.com/this-is-nuts-why-we-reduced-risk-on-friday/

“I believe nothing the government reports, nothing. Zero confidence in what they say.”

GOOD FOR VIC SOPRANO! We need more people to wake the f up and realize the goooberment is nothing but a lying, criminal entity!

Too true!

Iran Attacks vs. Trump – War? – Gold & Silver – January 9, 2020 – Special Broadcast

iGoldAdvisor – Christopher Aaron #Video

Sprott weekly wrap:

Glad Eric Sprott discussed in the last 1/3 of the interview taking his stake if JAG Jaguar Mining up to 48%, and a nice endorsement of DV Dolly Varden Silver’s exploration potential around their past-producing mine in the Golden Triangle of British Columbia.

Good to know; I must own the other 52%.

Nice Doc! I’m looking forward to what you and Eric do with JAG moving forward.

It should be a very constructive year with the price of gold higher than in years past, and with their plan to get back to around 100,000 ounces of gold production this year.

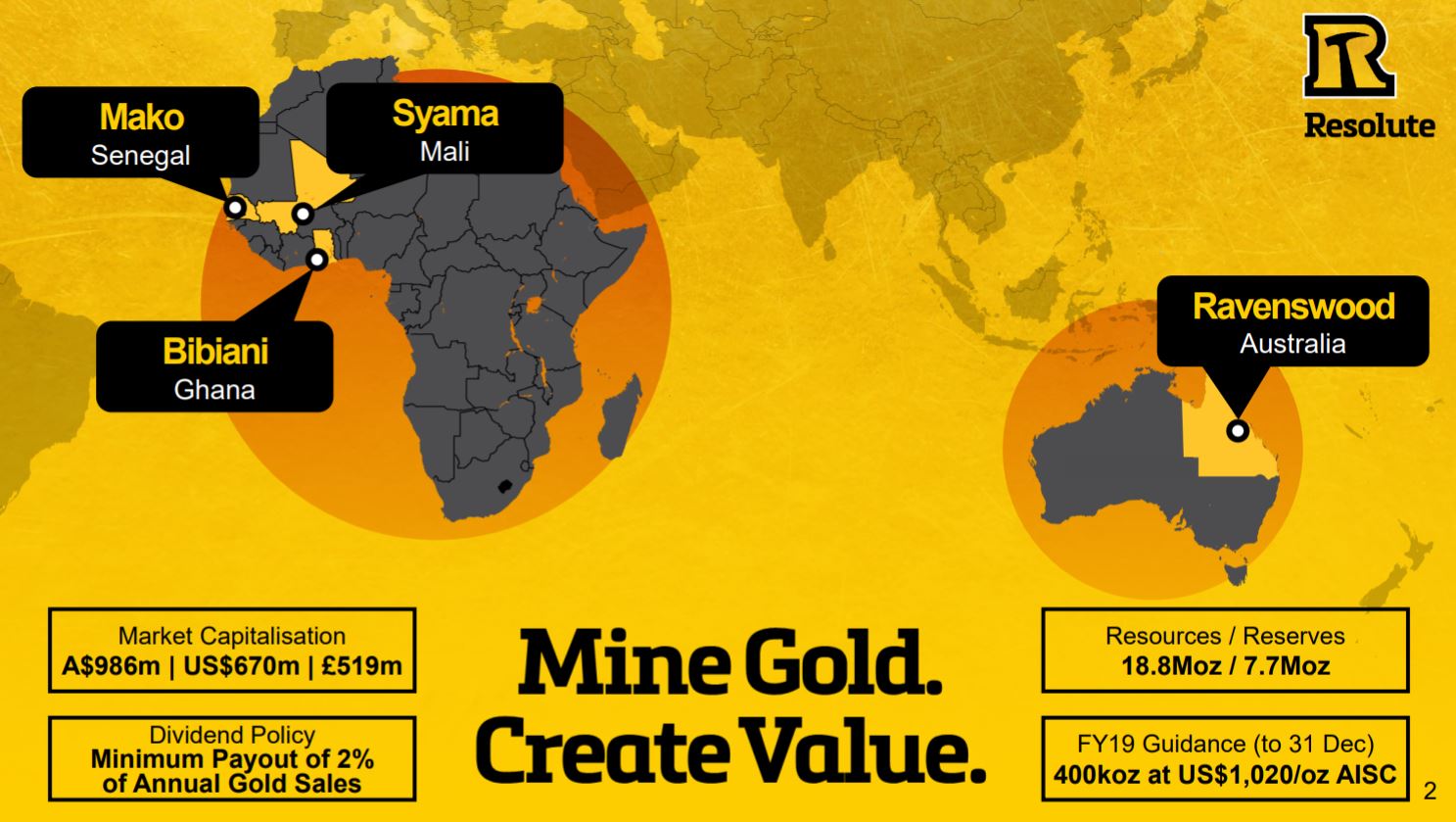

I’ve just started a position in the Mid-tier Aussie company Resolute Mining (RSG.AX) (RMGGF) that is doing 100K ounces of Gold production per quarter. It seems to be doing all the right things and is incredibly well run, but hasn’t gotten much love from the marketplace.

_____________________________________________

(RSG.AX) (RMGGF)Resolute Mining – December Quarter Production Update

8 January 2020

• Gold production of 105,293oz for December 2019 Quarter (up 2,092oz on September 2019 Quarter)

• FY19 gold production of 384,731oz relative to guidance of 400,000oz (for the 12 months to 31 December)

• Syama sulphide roaster successfully repaired in December; operating at nameplate capacity

• Syama autonomous fleet fully commissioned and 400,000 tonnes of high grade underground ore stockpiled

• Mako delivers another exceptional production result with 42,997oz of gold poured for December 2019 Quarter

• Stage 1 of the Ravenswood Expansion Project completed

• Cash, bullion and listed investments as at 31 December 2019 of A$181 million

Ex, I don’t know whether you have been following any of the helium juniors, one in particular went up 500% last week. DT

Thanks for the heads up DT.

Sounds like they are full of hot air! 😜

Resolute is interesting

What about the juristictions? Mali seems not the best place to operate?

Any information about insider transactions? Management seems not to hold many shares?

HI Thomas. Those are some good questions to consider for Resolute Mining (RSG.AX) (RMGGF).

Resolute is one of the premier larger operators in West Africa & Australia, and they have 9 mines in 4 countries and have been at it for 2 decades.

Many North American investors are reserved about going into African miners (which is why they trade at a discount to their Canadian & US peers), but West Africa has dozens of producers, developers, and explorers operating successfully. I’ve personally been investing in West Africa miners since (TGM) True Gold Mining with Mark O’Dea’s Oxygen Group successful takeover by (EDV) Endeavour Mining [one of biggest miners in West Africa]. I also had a nice success there in 2016 with (GPHYF) Gryphon Mineral’s takeover by (TGZ) Teranga Gold [another great mid-tier producer in West Africa], and in 2017 when (AVK) Avnel Gold was taken over by (EDV) Endeavour once again. Currently I hold shares in (ROXG) Roxgold, (ORE) Orezone, (HUM.L) Hummingbird, and (SWA) Sarama Resources, beyond my new holdings in Resolute Mining once again. I’ve held shares in Resolute off and on for the last few years.

________________________________________________

Regardless, initially Resolute started with their Australia mines (and also had stakes in a few Aussie gold miners like Northern Star), and expanded into Tanzania (a much more challenging African jurisdiction) and earned their stripes.

Over time Resolute got more interested in the vast Gold opportunities in West Africa (like most African Gold producers not relegated to South Africa) — adding in their assets in Ghana, and then in 2003 eventually the Syama Gold mine in Mali (which they picked up from Randgold).

Sayama is now a world class asset, and they are deploying cutting-edge self-driving vehicles and greatly reduced their workforce there, minimizing the labor risks, but harnessing technological efficiencies.

So after operating in Mali for 17 years, through all kinds of political cycles, they’ve become entrenched in the community as a viable company and partner, and are in the lower part Southwest part of Mali, where most of the conflict is up around the Northeast boarder of the country. That isn’t to say there isn’t risk in West Africa in any of the jurisdictions, but simply that they are very experienced operators there and have stood the test of time.

Over the years Resolute has also expanded into Senegal, which is a great jurisdiction and is getting a lot of interest lately from Gold miners.

This graphic does a good job showing their 4 main areas of operations at present:

http://cdn.ceo.ca/1f1mg3j-Resolute%20Mining%20Operations.JPG

{kind=link}

As for the insiders, I don’t really know their exact ownership, but keep in mind this is $1 Billion producer, and not a $10 Million explorer, so it would be unusual to see management with 5-10% of the companies shares.

Here is a nice slide showing their 10 Ten Investment firms though:

http://cdn.ceo.ca/1f1mhfo-Resolute%20Mining%20Stock%20Information.JPG

{kind=link}

In addition, I expect Resolute to acquire a few more companies in 2020 or 2021 to grow through acquisition, and here are a few of the key strategic stakes they have in Jr Explorers & Developers in Africa:

http://cdn.ceo.ca/1f1mhkb-Resolute%20Mining%20Strategic%20Investment%20Partners.JPG

{kind=link}

Attached here is the Resolute Mining Corporate presentation from November.

They dedicate pages 7 – 16 just for Syama and what they are doing there using technology and autonomous vehicles and is the kind of model I’d expect more miners to embrace over time. Really great strategy, implementation, and execution.

Thinking back on the Gryphon takeover by Teranga a few years back, I was pretty jazzed about the company that Teranga (TGZ) would grow into, and haven’t been disappointed. They are another very well run Mid-tier Producer in West Africa, and with the exploration work they are doing at Golden Hill, I hope they eventually get bold and acquire my (SWA) Sarama Resources position, which is one of the Jr explorers that has languished in my portfolio.

Teranga has the growth profile to add another mine at Golden Hill, and the lands Sarama has all around it make a takeover of SWA by TGZ a real potential.

I still really like Sarama’s land position, and like that they have their South Houndé Project back to 100% ownership, from Acacia Mining, now that Barrick is divesting non-core assets and reigning in the wackiness of Acacias issues. This took away the big road block to acquiring Sarama, because that whole deposit was going to be stuck in no mans land with Acacia as they worked out their insane tax issues with the Tanzanian government. Now they are free from that whole quicksand, and can shop SWA around to companies like Teranga, Semafo, Resolute, Roxgold, or Endeavour mining to get at that project and Bondi, and other exploration projects unencumbered.

In addition, Sarama’s JV partner at a few different projects, Savary Gold (SCA), was acquired last year by Semafo (SMF) another solid mid-tier producer operating in West Africa. For a while (SWA) Savary moved higher in sympathy on the takeover news of (SCA) by (SMF), but it is back in the “forgotten” bin for most investors.

Check out how strategic the lands are that (SWA) Sarama has in relation to Teranga, Roxgold, Semafo, and Endeavour mining:

https://saramaresources.ca/wp-content/uploads/2018/05/sarama_south-hounde_project_location_map.jpg

{kind=link}

Developing Burkina Faso’s next gold district. – (SWA) (SRMMF) Sarama Resources:

“Located approximately 350km southwest of Ouagadougou, Sarama’s 100% owned South Houndé Project is situated in the prolific Houndé Belt, which is home to three operating mines including Semafo’s Mana Gold Mine, Roxgold’s Yaramoko Gold Mine and Endeavour Mining’s Houndé Gold Mine.”

“The belt is highly prospective and remains relatively underexplored, demonstrated by recent exciting discoveries at Teranga Gold’s Golden Hill Project and Endeavour Mining’s Kari Pump Deposit.”

“The South Houndé Project has an Inferred Mineral Resource of 2.1 Moz(1) at 1.5 g/t (43 Mt at 1.5 g/t Au at a 0.3-2.2 g/t cut-off) and contains a high-grade component of 1.5 Moz Au at 2.1 g/t (at a 1.2 g/t cut-off). The mineral resource includes 0.6 Moz Au of oxide and transition material and oxide heap leach investigations achieved 87% gold recovery in column leach test work.”

https://saramaresources.ca/portfolio-posts/south-hounde-project/

In that post about West African successes with so many new and established gold miners, and thinking back on True Gold and Mark O’Dea, I’ve always felt good having their team involved. Mark also spun off his nickel company to Royal Nickel Corp a while back and I was a prior investor of RNX (and may be again one day soon).

Mark went over to the board of (NXE) NexGen Energy for a few years, which is hands down the best explorer/developer in the Canadian Athabasca Basin, so they know how to pick the winners. Mark stepped down though to get more focused on Gold/Silver/Copper again with his Oxygen Capital Corp, and I’m glad he’s out there.

I’m invested with them at (PGM) Pure Gold Mining [gold developer and near term producer], and (DSV) Discovery Metals [Silver Developer/Explorer, considered (SUNM) Sun Metals for Copper/Gold explorer, and missed the boat so far with (LGD) Liberty Gold, but may still jump in this year. Hell, I may just collect the whole set and grab some SUNM when copper gets perkier.

Many guest and pundits discuss backing good management teams, and I believe the Oxygen Capital Corp team are solid and deliver on their strategies.

Ex, thanks for all your great info

I also had Endeavour via True Gold. That’s why I also like Leagold. I sold my Endeavour shares because of the risks with Burkina Faso. I think Mali is risky too. Ghana and Senegal are probably the best you can get in West Africa.

I like to see management buying shares in the open market. Leagold and Equinox are probably the best examples (Guistra and Beaty). Have not found any info about Insider transactions in Resolute. Not sure If there is a site for ASX stocks to research this.

Sure Thomas. Glad to share ideas. Yeah, the risk profile for Burkina Faso is up in certain parts, but most of the mining action from Roxgold, Endeavour, Semafo, and Teranga has been relatively safe in the part of the country they operate in. Yes Ghana and Senegal are pretty safe as is Ivory Coast.

As for the insider buying, I agree it is a good signal to the marketplace, but I haven’t found a good SEDI like site for Aussie Miners, and the amount shown by insiders is unknown on a few financial sites like Yahoo or Bloomberg.

Yes the Leagold and Equinox merger is a solid rollup and the insider buying from Frank and Ross are encouraging. EQX is going to morph into a real powerhouse producer over the next 2 years.

Gold price hits all-time record high of Rs 42,000 level in Indian spot market

Over the last year gold has made record highs in many currencies all over the planet.

Thanks for the show KER!

Gold looks like it is going to have a big move versus oil this year and that will be great news for the miners since energy is a major cost component of doing business.

https://stockcharts.com/h-sc/ui?s=%24GOLD%3A%24WTIC&p=W&yr=4&mn=3&dy=0&id=p29340931570&a=712746354

The above bodes well for more great gains for gold vs commodities in general:

https://stockcharts.com/h-sc/ui?s=%24GOLD%3A%24CRB&p=W&yr=4&mn=3&dy=0&id=p74772395438

Gold looks remarkably good considering the week it just had. It now has back-to-back higher weekly closes than its previous high close back in August…

https://stockcharts.com/h-sc/ui?s=%24GOLD&p=W&yr=4&mn=3&dy=0&id=p43593164341&a=712774405

KWN quote of the week:

Sven Henrich: “If you don’t count any of the 96 million Americans not in the labor force then the unemployment rate is at historic lows. If you don’t count any of the items with prices going up then inflation is non existent.”

https://kingworldnews.com/

An interesting article I found at 321gold:

COMMITMENT OF TRADERS (COT) DATA SUGGESTS GOLD IN RALLY MODE

https://www.thetechnicaltraders.com/commitment-of-traders-cot-data-suggests-gold-in-rally-mode/

The author didn’t mention it but it looks like the commercials covered some shorts at a loss during the last reporting period. That is very unusual and bullish.

Catching Up With Doug Ramshaw At Minera Alamos (MAI) (MAIFF)

January 11, 2020 by EconomicAlpha

The general flow of the conversation was focused on these primary themes:

(1) Santana Construction and Budget

(2) Exploration and Resource Update

(3) Other

(4) La Fortuna

https://economicalpha.blog/2020/01/11/catching-up-with-doug-ramshaw-at-minera-alamos/

@TheGalvanizer (Doug Ramshaw)- “Couple of pics added now the explosives and detonator storage facilities have been constructed at site.”

Rick Rule on Canadian oil and Gas:

Why traders playing oil like it’s 2010 are ‘getting their heads handed to them’

Emily McCormick – Yahoo Finance – January 11, 2020

“Crude oil traders who bet on a major price surge after U.S.-Iran tensions flared last week ended up losing big as those tensions subsided.”

“Dan Dicker, a veteran energy trader and found of The Energy Word, tells Yahoo Finance that the prevalence of algorithmic trading today has made it that much more challenging for human traders.”

“Instead of humans playing the market, there really are machines playing the market,” he added. “And yes, we’ve all had to become used to that, because those traders who have been playing the game as if it were, you know, 2010 or 2000 or 1995 have gotten their heads handed to them.”

Ex, are you sure you aren’t an algorithmic advisor, if we had a look inside your cranium I’m sure the wheels would be spinning like a swiss timepiece. I hope the deep state doesn’t clone your brain and put it in an algorithmic trading machine. The humanoids are amongst us. I think they should send you to the Galapagos Islands as an endangered species. LOL! DT

Haha! Thanks DT, but this is more like it:

https://tse1.mm.bing.net/th?id=OIP.2C4aKk1ZJ4ZrSo4vAnucuwHaHa&pid=Api&P=0&w=300&h=300

This is you after the deep state clones your brain and sends you to the sanctuary. LOL! Dt

200111155929-diego-tortoise-2-exlarge-169

haha! That’s how I feel already DT. Man you know how inspire someone! 😮

🐢🐢🐢🐢🐢

> Canada Gold Reserves

“Gold Reserves in Canada remained unchanged at 0 Tonnes in the second quarter of 2019 from 0 Tonnes in the first quarter of 2019. Gold Reserves in Canada averaged 7.56 Tonnes from 2000 until 2019, reaching an all time high of 46.20 Tonnes in the first quarter of 2000 and a record low of 0 Tonnes in the first quarter of 2016.”

Canada with 0 gold reserves. Great plan!

Gold Stocks: ETFs Or Individual Miners?

Jan 10, 2020 – Morris Hubbartt – Super Force Precious Metals #TechnicalAnalysis #Video

Morris makes a solid point on this SILJ chart. ETFs are often full of the larger clunky companies, and an investor is stuck with their weightings, and often they only feature the smaller Jr nano-cap companies in insignificant amounts or not at all.

#BuildYourOwnETF and actively manage the positions and weightings.

http://www.321gold.com/editorials/sfs/hubbartt011020/sfj_silj.png

{kind=link}

Here are the holdings/weightings inside of SILJ: the “Junior” Silver EFT (cough)

Company Name – Holding Allocation

Pan American Silver Corp. 12.27%

First Majestic Silver Corp. 11.55%

Hecla Mining Company 11.19%

Coeur Mining, Inc. 10.52%

SSR Mining Inc 4.71%

Hochschild Mining plc 4.57%

MAG Silver Corp. 4.40%

Yamana Gold Inc. 4.37%

Silvercorp Metals Inc. 4.37%

SilverCrest Metals, Inc. 3.90%

Hudbay Minerals Inc 2.49%

Endeavour Silver Corp. 2.36%

Alexco Resource Corp. 2.01%

Americas Gold and Silver Corp. 1.96%

Bear Creek Mining Corporation 1.88%

Fortuna Silver Mines Inc. 1.85%

Maya Gold & Silver Inc. 1.62%

McEwen Mining Inc. 1.55%

Sierra Metals, Inc. 1.42%

Sabina Gold & Silver Corp. 1.37%

Gold Resource Corporation 1.31%

Excellon Resources Inc. 1.22%

Minaurum Gold Inc. 1.11%

Great Panther Mining Limited 1.10%

Trevali Mining Corporation 1.07%

Kootenay Silver Inc. 0.96%

Mandalay Resources Corporation 0.91%

Canada Cobalt Works Inc. 0.41%

Minco Silver Corporation 0.39%

Pan American Silver Corp Contingent Value Rights 2019-22.02.29 0.39%

Short Term Investments Trust Treasury Portfolio Institutional 0.31%

Golden Minerals Company 0.30%

Mirasol Resources Ltd 0.26%

U.S. Dollar -0.09%

Most of the heaviest weighted companies are not really Jr miners as they are the mid-tier to major Silver producers, or there are primary gold producers like Yamana, McEwen, Mandalay, or Base Metal focused companies like Hudbay, Sierra Metals, Hudbay, Trevali, etc… Yes, they may have a little silver exposure, but they shouldn’t really be featured in a “Junior Silver mining” ETF.

Then there are bizarre weightings like MAG Silver one of the larger developers that has been stalled getting into production for a decade and hasn’t performed nearly as well as smaller more torqued Jr Developers like Alexco or Kootenay, positioned than actual silver producers featured like Silvercorp, Americas Silver, Excellon, Maya, etc…

Speaking of Producers, they don’t even have 3 of the best performing Jr Silver Producers – Impact Silver, Santacruz Silver, GoGold Resources (WTF?) In addition, Silverbear & Avino Silver & Gold are missing as Jr Silver producers. While ASM hasn’t performed as well as some of the other producers, it is a far more established Jr Silver stock than Mirasol, Minarum Gold. Canada Cobalt Works, Golden Minerals or the aforementioned Gold and Base Metals focused companies included in this “Junior Silver Miners” ETF. What a mess…

Along the lines of the Silver Developers and Explorers – They could have left out half of the companies on here and honed in some of the more interesting actual Junior Silver stocks like Discovery Metals, Bayhorse Silver, Silver One, Southern Silver, AbraPlata, Aurcana, Defiance Silver, Metallic Minerals, Dolly Varden, Vizsla, Aftermath, Orex Minerals, Silver Bull, Silver Spruce, or New Pacific.

SILJ is an interesting basket of stocks, and will do well if someone wants to plop money in it and not do all the research or manage their own basket, because it does have a few big companies like First Majestic, Coeur, and Pan American weighted heavy, but they aren’t Juniors, and as mentioned, many of the good Juniors that are included are not weighted high enough. A Junior Silver mining index shouldn’t include those big companies, and could do without many of them ( like the above mentioned, or Hochschild, SSR, Pan American, Hecla, MAG, Hudbay, McEwen, Mandalay, etc…) in a Jr Silver index.

SILJ, like most supposed “Junior” ETFs is really a freakshow mashup of Larger Silver companies, Gold & Base Metals companies, and then insignificant weightings to non-existent weightings in many of the more interesting actual Junior Silver companies.

It makes sense to diversify across a basket, as mining companies are extremely risky, and there are no shortage of unforeseen problems that can blindside any mining company, but many of the top performers in the Silver Jr stocks for last year aren’t even included at all, so an investor that takes their time to really research the sector can have better picks and better weightings in those picks if they build their own ETF.

Ex:

Excellent analysis. It will interesting to see how the unrepresented Juniors do against the Indexes. Managed money will probably go for Indexes at first as they have considered miners as “no mans land” for so many years. Managed money also wants to treat miners as anything other than functional operating businesses with profit/loss business plans. Maybe this time the investment world will figure out that the dysfunction is not with miners but the brokerage system itself. Great comments and I vote for your insight being accurate in the months to come.

David, the best “real” juniors performed twice as well as SILJ or better in 2016. SilverCrest has to be the best performing example by far.

Some of the problems with the smallest ones are a lack of liquidity and a lack of assets in the ground or even real exploration prospects. So the more speculative ones would easily underperform SILJ. So even if someone did manage to throw such an ETF together, I’m not at all sure it would be superior and it really could be very inferior.

The time to launch one would be near a bubble or “mania” top since that’s when the greatest demand for such speculative stuff appears (as in any sector). While everyone is dreaming of the next lottery ticket, the launching of such an ETF would push our individual picks much higher AND give us something to short once silver becomes exhausted. Such an ETF would crater with leverage to SILJ following a major top.

Thanks David. I agree managed money and new generalist investors will likely go for the ETFs first, and that makes sense. GDX, GDXJ, SIL, and SILJ still did great in 2016, or in the Q1 rallies in 2017, 2018, 2019 or in the big summer rally last year.

As mentioned, some of the larger producers like First Majestic, Coeur, and Pan American may pull along their averages, as will some of the Mid-tiers like Silvercorp, Americas Gold & Silver, and Fortuna or the Gold companies like Yamana & McEwen. It just seems like those would be a better fit for SIL as the larger miners, and not SILJ as the supposed “Junior Miners”

However, imagine if they weighted higher or included in the first place the Jr Producers like Santacruz, Impact, GoGold, Excellon, Silver Bear, etc…, or had bigger allocations to developers like Silvercrest, Alexco, Kootenay, Bear Creek, (or allocations at all) to Discovery Metals, Silver One, Southern Silver, Bayhorse, Aurcana, Metallic Minerals, etc

There are a number of Silver Mid-tier Producers, Smaller Silver producers, and Advanced #Developers, that had reasonable liquidity and were up 50%-250% during the surge last year (like Silvercorp, Americas Gold & Silver, Santacruz, GoGold, Excellon, Impact, Silver one, Southern Silver, Alexco, Bear Creek, Discovery Metals, Vizsla, Aftermath Silver, Defiance, Kootenay, etc…) that were under-represented or not represented that outperformed the index.

Personally, I have a position in First Majestic, and have held Coeur in the past, so I have no problem holding a position in the higher torque big boy producers alongside a basket of curated picks in the Jrs (as that is where most of the SIL and SILJ performance came from anyway). I’d rather pick 1-3 of the better movers in the larger to mid-tier producers than get bogged down with most of them.

I just don’t have much interest in having exposure to some Silver companies like are slower to rise in previous rallies like Fresnillo, Hochschild, SSR Mining, Pan American, Hecla, Fortuna, etc… because I’d rather have the higher torque smaller to mid-size Producers in those slots. The nice performance in SILJ isn’t coming from those larger laggards anyway.

Going into 2019, my biggest position was in the highest margin Silver producer on the planet (SVM) Silvercorp, and it was the top performing medium to large producer last year at 160% gains on the year (yet farther down their weighing in their index and far outperforming SILJ). My largest 2019 position in a smaller producer was in (SCZ) Santacruz up 250% at one point last year as the top performing producer period [not even included in SILJ but crushing it’s returns 5:1]. On that summer surge higher, I did trim some of the position back in early August

and moved more funds over to (IPT) later in the year to position for 2020, and am pair trading those 2 as far as allocations at present.

On the developer side, I also had bigger stakes in (AXU) Alexco, (DSV) Discovery Metals, (KTN) Kootenay which were up 120-150%+ last year, far outperforming the index, and DSV isn’t even in the index. (BHS) doubled at one point on the news of their trial mining and success with the oresorters, but sold off later in the year, but I expect it to break out in 2020.

Bottom line, there were fundamental reasons why all those companies outperformed and got the investor money last year, so for anyone doing the homework, none of those were a surprise and should have been selected more heavily than the indexes.

The same could be said for the moves in (SIL.TO) Silvercrest [which I don’t hold any longer) for their epic exploration results at a developing Tier 1 asset, which is the reason behind their amazing share-price out-performance. Even SilverOne, [which I don’t own at this time] outperformed most of the pack for fundamental reasons, but once again, it wasn’t even included in SILJ, and it was plenty liquid to do so.

Overall 2019 was incredibly lucrative in the Silver miners, but I believe it will pale in comparison to the moves higher we see in these miners in 2020 and 2021.

Good luck to all the Silver wingnuts in 2020!

To the mainstream investor, SILJ is very much an ETF of juniors:

Investopedia:

A small cap is generally a company with a market capitalization of between $300 million and $2 billion.

— — —

The reason I am less critical of SILJ than GDX”J” is that there are much fewer good silver juniors to choose from than gold juniors. In addition, even silver “seniors” (most big ones really aren’t very big) offer junior-like leverage right now due to the economics of most projects with silver at these multi-year lows so why take huge risks on the tiny explorers at this stage? If this bull is the big one that many of us think it is, we will have years to play the riskier ones in the future when silver is high enough that our Impacts and Alexcos lose leverage and discovery and very low grade prospects are where it’s at.

Unlike gold, silver is extremely cheap on an inflation-adjusted basis so it needs to do some catching up before there’ll be a ton of speculative interest in the sector. While it does catch up, companies with production and/or assets in the ground are very likely to perform the best.

Companies like Kootenay will really come into their own at $20+ silver.

Matthew – That’s a good point in comparing the Gold miners to the Silver miners, and I agree GDX”J” is far worse and hardly has any of the higher torque Juniors, and is mostly larger to mid-tier companies.

I guess to most generalist investors or funds SILJ is still “junior” enough for them, but the bigger companies are 1 Billion – 6 Billion, so compared to many Jr miners in the $5 Million to $300 Million range they are large in comparison. They’ll offer good leverage because there are so few when money piles in, but yes I agree the smaller companies like Kootenay with a 74 Million market cap will have more room to run.

For me there’s no clear market cap cutoff where a junior becomes a mid tier. For example, a $500M producer that operates in one district and has only one producing mine has the risk profile of a junior whereas a smaller more diversified miner might have the risk profile of a much larger company. Remember when Osisko hit $5B as an explorer about ten years ago? It definitely did not have the risk profile of the average senior but was priced like one.

If I thought that the bull market would establish itself very convincingly to the average onlooker sooner than most expect, I might buy a pile of $5-$10M mcap companies on the gamble that they will rise 5-10 times for virtually no good reason. There was a lot of that last time and established sub-$30M companies became harder to come by.

Studies have shown that smaller caps tend to outperform, all else being equal.

Yes agreed. I usually prefer a Mid-tier to be based on having 2 or 3 operating mines, and want to see a certain level of production from them on an annual basis, more so than a specific market cap…. but once they’ve achieved that they usually have a $300 M – $1 B market cap. I agree that the smaller market cap companies will move more in wild bull market, and believe we’ll see that later in 2020 or maybe in 2021. I like having a few mid-tier or even the occasional larger producer mixed in during earlier parts of a large intermediate or major move when the generalist money starts coming back into the sector, and then moving further down the food chain in the smaller market cap Jrs as things pick up the pace. For now I have a nice blend of producers, developers and explorers, but have been more heavily weighted to the Mid-tiers and smaller producers and the most advanced Developers, and will likely decrease some of that over time and increase the early stage developers and explorers later in the cycle.

My Big Trend Analysis for Silver Investor – Part I

Everyone seems to be focused on Gold recently and seems to be ignoring the real upside potential in Silver.

Chris Vermeulen – Jan 12, 2020

“With all the global economic issues, military tensions, geopolitical issues, and other items continually pushed into the news cycles, it is easy to understand why traders and investors may be ignoring Silver.”

“Silver has really not started to move like the other precious metals. Gold is up over 45% since 2016. Palladium is up over 350% since 2016. Silver is up only 29% since 2016. The Gold to Silver ratio is currently at 86.7 – very near to the highest level on record going back over 25 years.”

https://www.fxempire.com/forecasts/article/my-big-trend-analysis-for-silver-investor-part-i-625269

(SIL) (SILV) SilverCrest Announces Closing of $13.2 Million Private Placement with (SSRM) SSR Mining

10 Jan 2020

https://ceo.ca/@newsfile/silvercrest-announces-closing-of-132-million-private

(EXK) (EDR) Endeavour Silver Produces 4,018,735 oz Silver and 38,907 oz Gold (7.1 Million oz Silver Equivalents) in 2019

10 Jan 2020

https://ceo.ca/@nasdaq/endeavour-silver-produces-4018735-oz-silver-and-38907

Great stuff guys. I hope and believe both of you are right about the favorable Junior market in the future. Overtime (2001 to present) I have held most of the established names mentioned above but have taken profits and reduced my holdings to a portion of my First Majestic and Kirkland and have none of my Silver Corp or Goro. I am in to about two thirds of those you mentioned above with heaviest orientation in Great Bear, Irving, Novo, Lion One, Discovery, Vizsla and decent share holdings in Pure Gold, Minaurum, Impact,kootenay, Minera Alamos, Mako, Precipitate, Santa Cruz and Wallbridge. Lesser amount of shares in many of the others you mentioned including some Pilbara throw money down the hole shots. I feel like the next goal I pursue is crossing the Interstate with ear plugs and blindfold.

David those are all great picks and I hold a number of those myself like First Majestic, Silvercorp, Lion One, Discovery Metals, Pure Gold, Impact Silver, Kootenay, Minera Alamos, Mako Mining, and Santacruz Silver.

I did own Novo and have considered getting back in at one point once there is more confidence in the mining method, and have considered every one of the others you mentioned like Irving, Minaurum, Precipitate, and Wallbridge. Precipitate has actually been on my watch list for a while and I should have pulled the trigger on it long ago. Same with Wallbridge. I do own Balmoral though (their neighbors) for that hot Gold area play by Detour, but also for their large nickel project that seems underappreciated by the marketplace. I still may add Wallbridge (but it feels like chasing it at these levels, and many others haven’t moved nearly as much yet).

Boy – Vizsla is the one that really surprised me last year. I realized that they had a lot of newsletter coverage and made a big deal about launching and buying the old property with infrastructure in place, but I couldn’t believe how much it kept going up just based on financing news. (VZLA) was the #1 performing Silver stock of 2019 going up 470% and I just kept asking myself – Why? They hadn’t done any meaningful exploration work or drilling yet to warrant such a huge move, but I noticed tons of folks who never even owned a silver stock before take a position in it pushing it higher and higher. I’m thrilled that they are finally drilling at present, and look forward to seeing what they may have on their hands. Hopefully the enthusiasm will be well-deserved, but it makes me nervous when a stock runs up so much prior to putting out any drill results. We can all think of dozens of examples of companies over the last few years that went up 500% or 800% that put out some results and pulled back, and put out a second batch of results and did a round trip right back down. There are a lot of savvy investors over at ceo.ca that I respect their opinions that are just crazy-animated about VZLA and I’m worried I hesitated because I felt it was getting too frothy, and may have missed the next Silvercrest. I’m just more comfortable waiting until post discovery in most cases, but I have to tip my hat to anyone that got into Viszla on the move higher last year.

Cheers!

Wow look at that VZLA chart. That was quite a move last year, and congrats once again!

Yeah I missed the boat on vizsla too…..was waiting for it to pullback when all the touting stopped or slowed down but it never happened….even jokingly told a friend we should buy just cuz of the name it was sign since he had a vizsla

It happens Wolfster. That is funny on the name and your friend.

If VZLA truly is the next Silvercrest, then the first few rounds of drilling will confirm or dispel this notion, and if they are the real deal, then I’ll start averaging in as there will be plenty of time to take the escalator higher, just like Silvercrest has run for years now. I truly hope they do hit paydirt as this sector needs some real discovery news and excitement and just a few big wins get many more eyeballs watching and speculating in this tiny sector.

Ever Upward!

Vzsla: I got in in-time to catch a good move so far. The Canadian market is pushing the price. The US market maker is a little squirrelly but the CEO is trying to fix that. In the meantime, the US price often lags the Canadian equivalent. Some days you can get a deal, some days you have to check Canadian and compute Canadian to make a guess at the ask, and someday it just gaps up (or down) playing catch up.

Santacruz looks dirt cheap, but it seems that only Zimapan generates profits and depends on a deal with Penoles? Their own mines seem to need silver at $30+ or $40+? Do I miss anything?

I believe they need about $20-$21 Silver on the other 2 mines, but yes the new mine at Zimapan is more economical and they’re still working on working it out with Penoles so that they own it outright versus lease it.

This is precisely why Santacruz is so leveraged to rising prices as few bucks higher and they shift from right under profitability to then making money. Like a near term optionality producer, with exploration upside.

Forgot: still holding my Silvercrest as still waiting for JPM to get their boot off silver’s neck. They are still finding more, so I am still holding like Great Bear.

Well David, I’m going to have to check out anything else you mention, because Silvercrest is the #1 Silver explorer/developer out there, and Great Bear was the #1 Gold explorer/developer out there last year. Both teams have just done a stellar job and both stocks were home runs for their shareholders. I follow their news and keep tabs on what others are discussing but sadly don’t own either one.

OK – I gotta ask, which Silver or Gold explorers or developers are you most excited about for 2020?

Matthew: should we be heeding this T.A guru’s warning to Gold Bulls?

https://www.youtube.com/watch?time_continue=194&v=hRtIXSjpjRM&feature=emb_title

Confused, no, not at all (actually NO! is appropriate). There will be plenty of warning if things turn in his favor and they haven’t yet, not by a long shot.

Thanks Matt,

I got a sense that guy was waayaay too confindent to be credible. Must be working for peeps who want to buy more gold shares.

Matthew, Excelsior, Doc, Al, Cory, et al, I am wondering if you are voting your Detour Gold shares in favor of the KL bid? It seems like a low offer to John Hathaway. I have not voted yet. I just hope KL will not appoint Hunter Biden or the Duchess of Sussex to its board.

Hi Bonzo b. – I don’t hold shares in Detour Gold, and haven’t held shares in Kirkland Lake since after they took over Newmarket Gold, but there doesn’t seem to be any competing offers and it seems like an accretive transaction for all parties. KL is a solid company and is really a Major producer now doing near 1 million ounces a year in Gold production, but that’s a bit too large for my tastes. Good luck though and yeah, hopefully they won’t put Hunter Biden on the board (haha!).

I have been watching the Kirkland Lake interest in the Windfall lake area play. I had bought into Metanor shortly before they did, which was since acquired by Bonterra with their Urban Barry Project (NSR to Golden Valley Mines), and believe that since Bonterra now has Metanor’s permitted and prior producing mill, that (BTR) will have a solid advantage as things proceed in that area. However I also noticed that (KL) took out a stake in (OSK) Osisko Mining, so they are playing both sides of the fence. My theory has been that Kirkland Lake will acquire Bonterra first, and then Osisko Mining to keep those deposits as decades of future production.

KL is also invested with Novo in the Pilbara so they have that iron in the fire as well, but that may be longer dated.

Cheers!

I had Metanor too, but sold them, because management never delivered and diluted to hell.

Yes, I’d agree that Metanor was poorly run, but it was actually reading about their implosion and fallout with most investors that got me watching them for a turnaround play, after most of the damage had already been inflicted. They had just done a share consolidation in early 2017 and restructured, so I figured it was a fresh start for them, and that they’d be raising money right afterwards.

I was researching small producers in mid 2017 and I liked that they were active in production and had the only licensed mill in the whole area and got in position. I believe Sprott Inc did the capital raise, and that was another vote of confidence, they had a few high grade drill hits, and then Eric Sprott and Kirkland Lake got in for more capital raises after that and there were some changes to their board.

It was about a year later and that (BTR) Bonterra took over (MTO) Metanor, and I’m happy with their team is at the helm, and with Sprott Inc, Eric Sprott, and Kirkland Lake as key investors.

Bonterra eventually put the Bachelor Mill on care and maintenance focusing more on drilling at Urban Barry and Gladiator, which makes sense, but I see that mill as key for the entire area and as the pearl inside of the oyster. It isn’t easy to get those permitted there, so that gives BTR a real ace in hole, but of course hitting so much high grade right next to Osisko Mining that is also hitting so much high grade is where the economical ounces in the ground come in.

I’d like to see the rising metals prices bid up both BTR and OSK for a while before any larger suitors start sniffing around for a buy, so I’m glad KL is going to be busy for a while with their takeover of DGC. Maybe they’ll wait on the Urban-Barry/Gladiator/Windfall lake area until 2021 and that will give investors some time for a measured increase and for more drilling and economic studies to be completed.

Cheers!

If I owned Detour I’d vote against the deal since it greatly favors KL.

KL would be parting with expensive and EXTREMELY overbought shares (90+ QUARTERLY RSI(14) reading!!!) so KL management is doing right by its long term shareholders from that standpoint.

Detour, on the other hand, is nowhere near long-term overbought and has a tremendous asset that will provide very good leverage to gold as gold rises. So the deal should only makes sense for Detour holders that are afraid of a political problem or/and gold failing to perform.

If the deal succeeds as it seems it probably will, I’d be inclined to sell KL or sell Detour before the deal is complete (it currently trades at a small premium to the .4343:1 exchange ratio).

Without the deal, KL is very likely to dramatically underperform the rest of the sector in the months straight ahead. With the deal, the same is still true unless gold rises materially to add significant value to the Detour asset.

Eric Sprott was wise to sell a big chunk of his Kirkland Lake position in mid to late 2019, and redeploy it into the more speculative Jr producers and developers, as KL is and has been overbought for some time.

There is not doubt that KL is a very well run company, and this created a herd movement from investors that like the larger producers out of some of the other Majors and into Kirkland Lake over the last few years as is rose from Mid-tier to Major. The Newmarket Gold assets (that were originally with Crocodile Gold) really helped fuel the move higher as the KL team got those mines optimized and kit big with exploration and expansion. It was one of those “safe bets” the last few years when things seemed more uncertain in the Gold miners, but I agree it has gotten very bloated in it’s current valuation.

It would seem the markets are behind the takeover move to grab Detour, but Detour would have much more room to run in this metals cycle if it wasn’t acquired. KL is right to grab them now and it is a good move and rare asset for Kirkland Lake to acquire for their shareholders.

I know all this interest in Detour has sure spiked the valuations of both (BAR) Balmoral and (WM) Wallbridge, who have both been doing a bang up job with their exploration as well. That whole area is very well-endowed, and I hope Balmoral spins out their Nickel assets into a new company, before someone tries to grab them on the cheap and ignores their huge base metals value, aside from their Gold projects all around Detours mine.

http://cdn.ceo.ca/1f1n1ru-Balmoral%20Resources%20Area%2051%20Detour%20Gold%20Trend.JPG

{kind=link}

Again, if the KL deal doesn’t work out with Detour, they could always buy both Balmoral and Wallbridge, but would need to develop them into mines — whereas Detour is already running a well oiled machine.

If that doesn’t work out then I revert back to KL taking over (BTR) Bonterra, and then eventually (OSK) Osisko Mining.

{kind=link}

This is a bit better map of the projects Bonterra (BTR) has at Urban-Barry and Gladiator, near (OSK) Osisko Mining’s Windfall Lake area play.

It is obvious why Kirkland Lake has strategic stakes in both companies, and doesn’t hurt that Eric Sprott saw the value in the Bachelor Mill 2 years back when it was with Metanor (prior to Bonterra acquiring them for next to nothing). Osisko also acquired Beaufield to further consolidate that area. Kirkland Lake may get the last laugh on that whole area though.

{kind=link}

Don’t get me wrong. KL does not “need” to fall. Long term overbought readings can remain in place for years (though that is less likely in this sector) and KL is currently far from overbought on the important weekly chart. The risk-reward just does not look appealing relative to so many others in the space at this time, especially with the huge potential that exists for another big sector-wide move to the upside.

After struggling for the last 7 weeks, it did manage to take back the 30 week MA but I’d be looking for signs of distribution in the weeks ahead to go with that big high-volume drop in November.

https://stockcharts.com/h-sc/ui?s=KL&p=W&yr=3&mn=11&dy=0&id=p80955656186

Ex:

I am in no way in your and Matthews ballpark but rely heavily on input from people like the two of you who I consider credible. I often start with names of miners that I hear repeated and then go read about their management and drill results. I also like to read the visit reports of those that go on site and attempt to gage their enthusiasm and bias. I also like to search after conference panel discussions and corporate presentations. Again, looking for momentum type statements that separate one from the other. I am no mining expert so if PRs vet too technical for me, I try to find someone who can interpret the reports. I like Quentin Hennigh, but go to ceo.ca to see if someone can translate his comments.

Anyway: If you look at my dollar allocations going into 2020, I appear to have this order: Great Bear, Silvercrest, First Majestic, Irving, Lion One, Novo, Vizsla, KL, Discovery.

In total shares: Discovery, Vizsla, Lion One, then (tie) Metallic, Minera Alamos, Precipitate; then (tie) Pure Gold, Wallbridge, Irving; Kootenay, GFG, Aston Bay, then (tie) Brixton, Novo; Ely.

I guess you can interpret a preference but if something starts moving more than others like Vizsla recently, I will move some money from others. Total shares may mean more than total money in 2020 expectations (hope). In the ceo.ca. Contest I have Discovery, Vizsla and Theralase. Theralase kind of a ringer as they are in Phase 2 human testing of their cancer treatment and are pending a report on their first couple of patients.

David thanks for kind words and for sharing your picks. Just so you know I put a high value on your comments as well, becuase those are excellent companies, and I can tell you do a great job separating true value from the noise, and positioning in trades that outperform their peers. You’ve done very well with those larger allocations and there are so many overlaps in our two portfolios, and the ones at the top of my wishlists are the other ones you mentioned. I had shares in GFG earlier but sold them after some of the run up to reallocate, but want to get back in to Claude 2.0 : ) . I’ve put in stink bids on Aston Bay several times that just barely missed getting filled and then it popped up. Again, with Precipitate I’ve hovered my finger over the buy button a few times, and should have jumped in, but one can’t own them all or dance with all the pretty ladies.

It is interesting that you brought up Theralase in the Biotech space, as they were a KE Report show sponsor for years and always seemed interesting, but I just don’t understand how to value the IP or evaluate if the trials and tests of products to know how that translates into what economics for the company. I have friends that are as nuts in bio-tech and swing trading those as I am in the resource companies, and we often say we can’t understand the drivers of the respective sectors. I know there is big money in bio-tech and leverage and crazy gains to be made, but I generally steer clear of it simply from lack of knowledge in that space.

I guess if Vizsla hits it could go parabolic, even considering how much it has already risen, and I’ll be watching for the results/reactions as they come out over the next few weeks/months. I’ve had more gold bugs ask me about it privately than any other Silver stock last year, and thought it was unique in how many of them picked it as their only Silver stock and then it surged 470%. Granted most got interested after it ran up the first 100-200% but still, it just kept climbing and climbing higher. While I feel great about my largest picks in the Silver sector the last few years, I struggle the most with taking a position in a hot exploration play that has really surged higher as 3-5 bagger. That is why I passed on Great Bear, but again, it kept climbing higher and higher (granted on continuous great drill results). Vizsla still needs to prove itself with the truth machine (drill results), but so far it is off to a bang up job with tons of market support, so it has captured investors attention in this crazy space and that is not easy to accomplish. Ever Upward!

ELY is another I’ve considered for a royalty play, but I’m in Golden Valley, Sailfish, and Maverix at present, and actually want to add to each of them, but also get a position going in Metalla, get my position back in EMX and and then maybe put a little in Ely.

I guess as things get more peppy over the next year and if I feel certain positions are getting too frothy, then I’ll store some of the gains in more royalty companies.

Right now I want the risk but potential upside of more individual miners, but I’m a big fan of the royalty and streaming companies business models. I actually would like to put some more funds into SAND as well as I sold out of it a while back.

Ely: their kick start could be their interest in Wallbridge.

That’s good information David. I haven’t really dissected the royalties that Ely has yet, but if they have one with Wallbridge, that could end up being very significant, as it really looks like they are onto something, in harmony with Balmoral, and Detour Gold.

It’s definitely in the cue, but my plan is to get at least a position in Metalla in place and add to Maverix before any other royalties. Maybe I’ll move Ely up ahead of EMX for the the one after that though. Thanks again!

Vizsla:

What I find potentially attractive is the limited drilling in the combination of properties. The description sounded like the land has had a lot of prospectors with success but limited mining company activity. Sounds like limited drilling below the water table. This is near First Majestic, Silvercrest, Mako, Goldplay, etc and those companies have had success below the water table. So historical shallow finds on the properties and other successful miners near by that have gone deep. So maybe good, maybe not…

I agree it’s the right neighborhood, and this is likely what animates folks like Eric Coffin, Goldfinger, and Doug Ramshaw about their potential.

Their drilling is underway, and if they hit big, there are so many people watching, that it may get pretty crazy. I hope they knock it out of the park, but personally don’t want to chase it until the results come in and get digested by the market.

__________________________________

Vizsla Begins Drilling at Panuco Silver District in Mexico and Outlines 2020 Exploration Plans

9 Jan 2020

https://ceo.ca/@newswire/vizsla-begins-drilling-at-panuco-silver-district-in

Vizsla: As I mentioned about the US market maker being somewhat squirrely, US current Ask is US $1.25 and bid $.43. I guess he is in the bathroom or something. In the meantime, Canada has passed its daily average volume and is green. CEO working on it.

Yeah, that’s quite a spread. Sometimes the US-based OTC markets can have wild arbitrages, as you mentioned.

Theralase is my largest share holding and 4th largest money expense. I have added every time they have had a positive release over the last 5 years, but I have stopped that habit until they succeed or fail.

Wow. That is a very strong endorsement David.

I reviewed Theralase a few times when Cory or Big Al would do interviews over the years, but I remembered a period a year or two back when investors were grumbling about how things were going. However, if they are on to actual phase 2 testing on humans, then they’ve moved the concept along nicely. I’ll have another look at it, but feel out of my element with the Bio-tech sector.

Thanks for sharing your picks and position sizing. Very much appreciated!

Theralase: Here is the real concerning thing about the stock. I would have to estimate that I have been in the green maybe as many as 10 times. But, the stock runs between .20 and .40 over and over. When the CEO seemed to pull off the kereport, it appeared to be backlash over issuing below market warrants. They have continued to do that over time and it could be that as long as they are going to do it, shorts are going to push the price back to the warrant price until some news changes direction. Anyway, I am disappointed that price is not much higher in view of successes.

Again, I am by no means a biotech expert either, but from a PR perspective, they have achieved the following. The science is comprised of a drug and a laser. The procedure can be administered in an out patient setting. Initially testing was on animals and was successful. The one surprise that happened to me was that they elected to re-enter the disease in animals that were previously cured, and rather than have to re-administer the process, the initial treatment had a “memory” and self cured.

They have received patents in Canada, US and I think Europe. They were approved for Phase 2 Human testing in Canada but are pending US. They have indicated delaying European testing due to cost. They have started Phase 2 testing in Canada after Health Canada approval and have designed Phase 2 testing to meet US FDA standards to make that transition when approved.

Human safety testing, phase 1, was primarily conducted through coordination with Princess Margaret Hospital’s Oncology and Research Dept. Safety test was ended early because initial testing proved to have little or no side effects. Review of results was concurred in by a group of experts outside the Theralase community. I just remember one from MD Anderson in Houston as I grew up there. I am not clear on whether all patients were cancer free or just those that got full dose…but there are cancer free P1 patients that were testing safety. The test is for non muscle invasive bladder cancer. Patients have to have tried all bladder treatment options short of removal of the bladder. (Theralase does not limit cancer treatment to bladders only but believes it will have many applications and hopes to expand phase 2 as things progress).

I checked the Princess Margaret site to cross check the MDs and PhDs working on the program and they do work there, they do write papers and make presentations at scientific conferences.

The person developing the drug is Dr Sherry McFarland (I think her first name is Sherry) who was at the the University of North Carolina but recently moved to the University of Texas at Arlington. She also is for real and has been recognized for her discoveries.

So obviously this is on the verge of success or failure , but past history appears to be encouraging. Treatment success doesn’t have to be 100% when considering life saving procedures. When you listen to all the commercials on TV that have a list of possible side effects and only limited treatment success, imagine one with a high degree of success with little or no risk.

So …back to the original concern. Why all the years of moving forward and no stock movement. I don’t know … but it leaves open the question of a “glitch” until success is shown. (Phase2 is planned for100, but they hope they get fast tracked). That’s about all I got. Do your own DD as usual. Price is cheap if successful. There are Stockhouse and ceo.ca sites. Can TLT, US TLTFF.

So far, the positives for the theralase methodology is as good as you can expect with the various modalities used for treating cancers. The stock and methodology has not grabbed the attention of the mainstream media yet. If Phase 2 is effective and the side affects are as minimal as they are currently, this stock is worth holding on to. Also encouraging are similar positive results on other cancers in lab animals, especially multiforme glioblastoma which is essentially non-curable and resistant to surgical ablation in its’ entirety. The only negative in my view at this time are the shares outstanding. Being in the medical field I’m currently enthralled with the results. I own a bunch at low prices and consider it a realistic speculation as regards the results up to this point in time.

Thanks David and Doc for unpacking more about the share count, the below market warrants, the successes with animal testing, and the promise of this Phase 2 human testing. I thought that point that when re-entering diseased animals that “the initial treatment had a “memory” and self cured,” was a strong point as well. Lasers in healing are very appealing and there is much that can be done with focused light, so it is an intriguing line of research. It sounds like it is worth taking another look at.

Doc:

Thanks for some Professional words from someone who speaks Theralase’s language. I understand cancer free but glioblastoma leaves me wondering if I missed that day in Spanish Class. Thanks for confirming things still appear to be on track.

What also makes TLT.V intriquing is what ex mentioned about the “memory”. What this means is that it appears when the light source initiates the photo dynamic compound response, it appears the PDC over time stimulates an immune response to the cancer which if true adds an ongoing positive reaction and is huge.

What keeps Rick Rule up at night:

His wife, if he’s lucky.

Thanks for the show. Great to hear Vic say he thinks gold will go up to 1750 or more this year. Let it be, let it be!