Hour 1 – Making sense of the Fed’s move this week from a macro prospective

I hope everyone is having a good Easter weekend. This is not what any of us had in mind for this weekend but hopefully things will get better very soon.

This week the Fed stole the headlines by announcing a $3.2trillion loan program aimed at supporting the economy. I spend a couple extended segments making sense of what it all means for the economy and you.

I also dedicate a couple segments to the resource investor focusing on royalty companies and Great Bear Resources.

Please keep emailing me to share your thoughts on the show, companies you would like to see on the show, and any of your other thoughts – Fleck@kereport.com.

- Segment 1 – Extended segment – Jesse Felder kicks off the show by focusing on the Fed’s announcement this week. We look to the long term implications and market expectations. Click here to keep up to date with Jesse’s market thoughts.

- Segment 2 – Extended segment – Marc Chandler continues the discussion on the Fed actions but also looks around the world to the other central banks and government actions this week. Click here to follow along with Marc daily writings.

- Segment 3 – Brien Leni and I shift focus to the resource sector and discuss investments in royalty companies. Click here to visit the Junior Stock Review website.

- Segment 4 – Chris Taylor, President and CEO of Great Bear Resources wraps up the show by recapping the recent drill results that hit more high grade gold. Click here to read over the drill results.

Exclusive Interviews this week

- TriStar Gold – Updating the drill program status and expected future news flow

- O3 Mining – Updating new drill results from the Pontiac East Zone

- LexaGene – Outlining the opportunities for testing for COVID-19 and updating the status of the testing device

- Eclipse Gold Mining – More information on the maiden drill program at the Hercules Project

These individual segments should all be up to date now. Sorry for the error earlier today.

You have last week’s show on for the 1st hour, at least as of 7:58am EDT. Please correct!

Gold price leaps to $1,750

Frik Els | April 9, 2020

Fed Chairman Jerome Powell said that the bank was committed to use its powers “forcefully, pro-actively, and aggressively until” the US economy is “solidly on the road to recovery.”

“Bloomberg reports the gap between New York futures and spot prices in London for physical bullion have widened to roughly $40, a sign of lingering concern over future supply and the difficulty of shipping bars around the world amid the pandemic:”

https://www.mining.com/monetary-madness-lifts-gold-price-to-7-year-high/

The OVERHEAD resistance………..is coming to an end……..$2000 will be shattered in no time…..MONEY printing assures the fact.

+2000

As mentioned yesterday, maybe $1,752 Gold isn’t exciting enough for folks and it will take $2,000 for generalists to realize that the miners represent great value here.

https://www.bloomberg.com/quote/GC1:COM

___________________________________________________________________________

I’m interested to see what happens when the Q1 2020 quarterly reports start hitting in a few weeks for the Gold #producers and if this wakes up Wall Street and Bay Street from their stupor regarding the mining sector; (and if they start connecting the dots on where things are trending). Yes, miners can make money at $1500-$1600 Gold, and have even zestier economic margins at $1750 Gold (once they can start producing again)

New generalist investor money flows into the Producers first when their economic margins go up substantially on the increasing Gold prices. Last year and earlier this year we saw the Majors & Mid-tiers responding much more than Jr developers & explorers.

When critical investors & analysts start looking at the big boys pipeline of projects, then it will become clear that they need to replace their reserves being depleted in operations. When this need to replace mined reserves registers with companies and analysts alike, and they realize prices are going to stay elevated, then sector sees more mergers and acquisitions in 2 main subsectors: The acquisition will be from the more advanced & defined deposits of the Developers, or many larger producers will also scoop up bolt-on smaller Jr Producers.

> Looking forward in the pick up of M&A later in 2020 and moving into 2021.

Speaking of M&A and as a call back to last weekend’s show:

The conditions are good for smaller Jr teams to concede to the larger companies if they want an escape hatch, but there have still been a few acquisitions going on even recently:

1) Osprey (OS) merged with MegumaGold (NSAU)

2) Excellon (EXN) acquired Otis Gold (OOO)

3) Endeavour Mining (EDV) taking over Semafo (SMF).

I had mentioned these last weekend but for some reason failed to bring up the merger between Argonaut (AR) and Alio Gold (ALO), which was big news.

Ironically, I had given up on Alio to get their act together last year and sold my position, and was still a bit bitter about how Rye Patch Gold (RPM) had fumbled their Florida Canyon operations for over a year, sold their Rochester Royalty to Coeur (CDE) for a short-term cash grab but longer term value and revenue loss (especially with rising metals prices), and then panic sold their company to Alio Gold (ALO).

I’m a big fan of the turnaround work, operational success, and exploration/development success that the current team over at Argonaut Gold (AR) has experienced, and believe the offer an amazing revaluation opportunity. Once the market wakes up to how big of an effect Cerro del Gallo and, in particular, Magino will have on their production profile, I expect (AR) to be trading many multiples higher.

Just 2 weeks ago, Argonaut (AR) has moved to acquire Alio Gold (ALO), so once again Florida Canyon will be be back in my portfolio. Apparently I can’t escape this mine, so I’m going to embrace this change, and if anyone can run Florida Canyon more efficiently it will be the team over at Argonaut Gold.

In addition to that, Argonaut also picks up the large development project in Mexico, Ana Paula, from their acquisition of Alio Gold, which is the old flagship of their company, before Alio acquired Rye Patch.

So in a nutshell, Argonaut Gold, who already had a substantial pipeline of projects, with 2 producing mines, and 2 large development projects, has expanded into true Mid-Tier territory with a 3rd producing mine, and a 3rd large development project.

AR is turning out to be an exciting story as solid producer, but even more exciting developer and project consolidator. I remain bullish on Argonaut for the future and see so many interesting catalysts in the next 1-3 years where they can bring into production a 4th, 5th, and 6th mine.

It just seemed worth pointing out that there are still M&A deals happening now, and company roll-ups into larger entities (like what Equinox Gold and Endeavour Mining have successfully executed these last few years). We’ll see more of these mergers and acquisitions as the metals prices stay high, and companies get creative to combine strengths into few, yet stronger organizations.

(AR) (ARNGF) Argonaut Gold and (ALO) Alio Gold Announce Friendly At-Market Merger

March 30, 2020

> Creates Diversified Intermediate Producer:

– Diversified platform with production from four operations totaling more than 235,000 gold equivalent ounces annually.

– Enhanced asset portfolio and Mineral Reserve and Mineral Resource base.

– Improved geographical diversification with assets in Mexico, USA and Canada.

> Captures Significant Operating and Jurisdictional Synergies:

– Argonaut has demonstrated operational excellence in open pit, heap leach mining over the last decade.

– The Florida Canyon mine is in close proximity to Argonaut’s corporate headquarters.

– Synergies at corporate and asset level G&A.

> Robust Growth Pipeline:

– Strong internal growth optionality from strengthened asset base.

– Mexico: Ana Paula and Cerro del Gallo.

– Canada: Magino.

> Improved Capital Markets Scale:

– Appeals to a broader institutional shareholder base.

– Increases research coverage.

– Improves trading liquidity.

> Financial Flexibility:

– Pro forma $55 million cash and $25 million debt as at December 31, 2019.

– $31 million available from Argonaut’s existing revolving credit facility.

– Improved credit potential from cash flow growth.

I was feeling really bullish about gold until yesterday…..long story short I have a friend who has found our best contrarian indicator. Football player client who chats up all his investments. The guy is late to every trend and he mentioned he wanted to buy gold yesterday…..my friend told him good luck there’s no physical gold available anywhere these days…..my only hope is he doesn’t get any.😉

Uh-oh. Well let’s hope this friend and “greater fool” that buys at the top doesn’t get any and mark a temporary top in Gold’s advance. 😉

Or if he buys here, maybe he can give us one more good boost to allow us to lighten up more on our positions for a corrective move.

Thanks for the heads up Wolfster!

For what it’s worth, Christopher Aaron put out this video where he is exercising caution as it relates to a higher Gold price in the near term, and believes it will pull back down some from here, to reduce the Gold:Silver ratio.

_________________________________________________________________

(skip to the 7:40 mark as there is a bunch of preamble about surviving the coronavirus and some of his personal anecdotes for the first part of the video before the TA section starts)

>> Gold & Silver Price Update + Coronavirus Strategies

iGold Advisor – Christopher Aaron – April 10, 2020 #TechicalAnalysis #Chart #VIDEO

NONE of the Gurus……….have been here before…….we are in unchartered waters….

This is true, but none of the Gurus have been in any new day before, and 50% of the time they don’t know how to read their charts and go sailing over waterfalls. (lol!)

I only post other technicians videos on charting and their interpretations as food for thought, ideas for consideration, and infotainment. Everyone has to do their own research and come to their own conclusions for how they should proceed.

Sail away, sail away, sail away….

And many thanks to you for posting the news…….

And here’s the news…

:))

I am following Alio Gold some wihle

Their Florida Canyon mine is very low grade, even for a heap leach operation

Ana Paul is located in one of the most difficult parts of Mexico (Torex had problems in the past)

Yes, I’ve been following Alio Gold since they took over Rye Patch, who was operating Florida Canyon before Alio. Neither did a stellar job, but Alio was finally getting the mine to be profitable, and Argonaut are much more competent operators, so they likely see the opportunity to improve things further or they wouldn’t be purchasing Florida Canon.

As for the Ana Paula development project, yes it situated along the Guerrero Gold Belt on trend with Torex’s ELG & Equinox Gold’s Los Filos operations.

Alio has invested $47 Million into Ana Paula in the last few years, and simply didn’t have the bandwidth to work on it, the money to work on it, nor the expertise. They stated in the most recent Corporate Presentation that they ceased work on the project because “Alio Gold is not in the business of greenfield project builds.” Their strategy was to JV out the project to a larger operator, but in this case they just got acquired by the operator. Same thing, where more competent operators will move the project forward at Argonaut.

Gold shows few signs of return to normal with spreads still wide

Bloomberg News | April 9, 2020

“People are paying the premiums over in the physical market and I think it’s rolling into the futures,” said Peter Thomas, a senior vice president at Chicago-based broker Zaner Group. “It’s safe-haven buying. People are scared.”

“While the market is disrupted, the fallout from the coronavirus crisis has boosted gold’s appeal as a store of value. Futures are set to close at the highest in seven years on Thursday, supported by the latest signal of weakness in the economy — U.S. jobless claims reached a new record for a third straight week.”

https://www.mining.com/web/gold-shows-few-signs-of-return-to-normal-with-spreads-still-wide/

I still don’t get this week’s Hour 1. It looks right, but the first person I hear is Trader Vic. I wonder what gives, since it seems other people are acting like it is the correct first hour.

Evidently some of us got reruns.

Weird. My kicks off with Jesse Felder.

Maybe the KER intelligence knows you didn’t fully value the prior episodes, and you are not permitted to proceed to the new show until you finish your homework. (haha!) 🙂

That was my first thought. Maybe I need to listen closer or participate in class more. Maybe ask better questions or bribe someone. I pay the maximum membership fee.

Haha! Pay to play…

Looks like you are right. My response was deleted and was nothing but humor.

Same experience. The 1 hr. segment is OK. The individuals are discs or tapes of previous recordings. Cory said he was very, very busy!

U.S. Economy Deteriorating With Alarming Speed

April 9, 2020 – Gary Wagner #TechnicalAnalysis #Chart #VIDEO

https://thegoldforecast.com/video/us-economy-deteriorating-alarming-speed

Ira Epstein’s Metals Video (4/9/2020)

Technical Analysis, Gold, Silver, Copper, Platinum

Newmont Leads The Upside Parade

(04/10/2020) Morris Hubbartt – Super Force #PreciousMetals #TechnicalAnalysis #Video

I bought some more Newmont for the small retirement account I manage when it dipped. Great buy and Thursday’s action was fantastic. However, it is now looking a little stretched IMO and might be due for a pull back.

I quit working for a salary back in 1981 in order to be an investor. I made 3 1/2 times my 1981 annual salary on just my NEM shares on Thursday. Life is good!

That’s awesome Bonzo! I’d like to think I would be in the same position in 10 years, but we will see.

Charles, in 10 years gold may be $10k and NEM @ 1000. I just hope we will still be alive and healthy.

Ronald Stewart @RonaldS_AuCu

“#Exploration is a value creating activity. #Gold grade is one of the best differentiators of value. Here are our 36 #ExploreCos, showing Grade Vs. Log EV/oz.”

“Six names stand out: $BGL.A; $SIL, $LIO; #OSK; $MKO & $AUG. Not a bad basket, IMHO.”

A good response to that tweet above from Ronald on exploration grades, as it really does depend in the type of mining as to how relevant the grade is. Many companies heap leach gold in Nevada at .40-.60 g/t where underground mines may need 4-6 g/t gold to be economic.

___________________________________________________________________

Public Heel @PublicHeel Apr 4 Replying to @RonaldS_AuCu

“A lot depends on the kind of mine/processing needed. MKO is a shallow O/P going after a deposit flipped to the horizontal. BGL is underground, and its CUTOFF of 3.5 is higher than most of the grades on that chart. Auryn’s Canadian projects are currently too small for development.”

Personally I own 3 of the stocks out of the 6 Ronald showed on that chart:

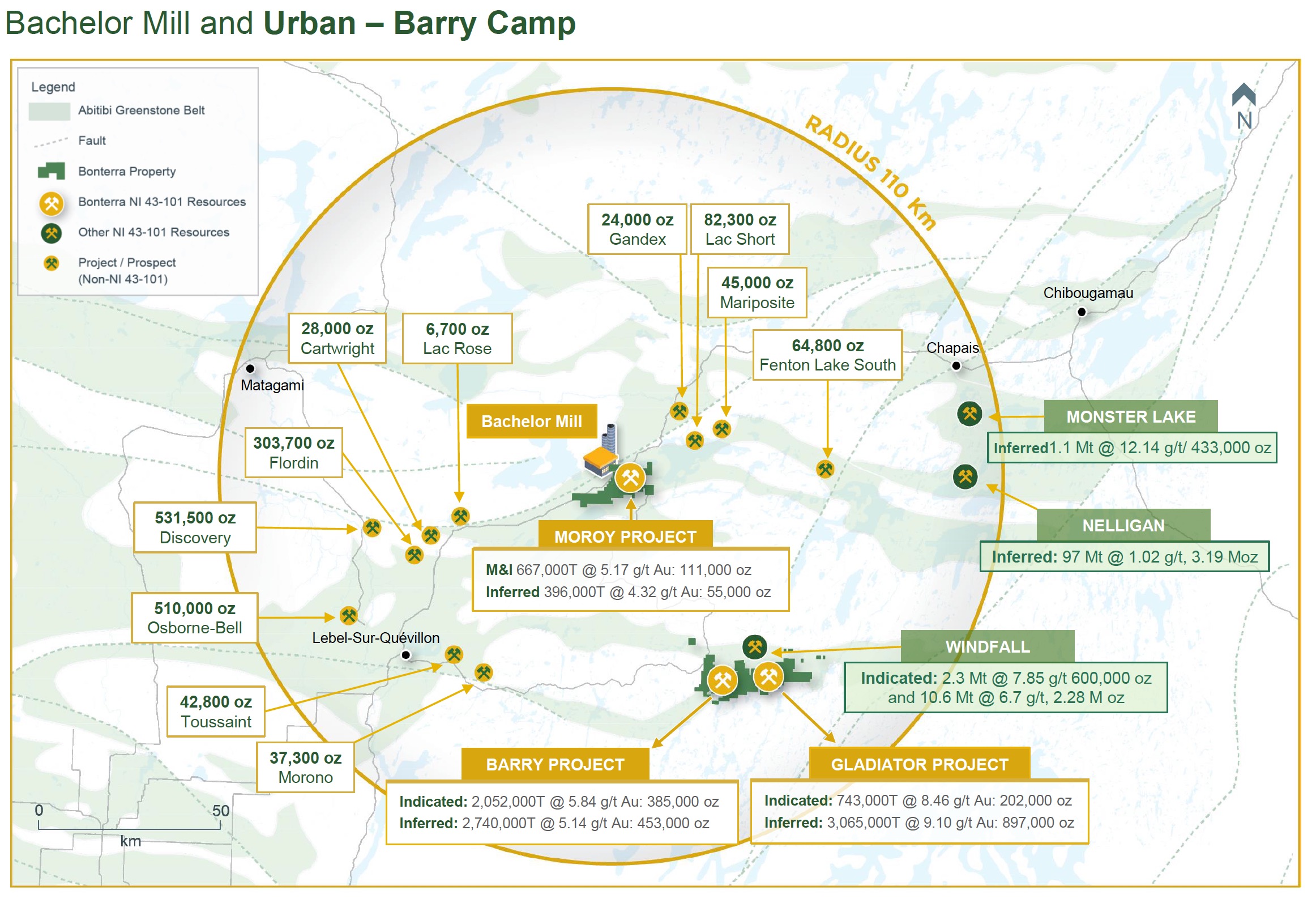

(SIL) – Silvercrest, (LIO) – Lion One, (MKO) Mako Mining, and also have a position in (BTR) Bonterra right next to (OSK) Osisko Mining at the Windfall Lake / Urban-Barry area play.

Grade isn’t everything but it sure helps!

I bought an initiAl tracking position in Bonterra, and bought a bunch more on the recent dip.

Nicely done Charles. I’m looking to top up my BTR position at one point soon as well, and feel it is quite undervalued considering beside the same prospective land package and multiple high grade discoveries, like Osisko Mining, they also have one of the only processing mills in the area, which gives them a huge advantage.

They could bring in other miners ore for processing and do some toll milling:

https://btrgold.com/projects/bachelor-lake-mill-abitibi-greenstone-belt-quebec-canada/

Here is a larger visual map of that area where Bonterra’s Bachelor Mill is located.

It is very easy to imagine them deploying a hub & spoke methodology for reaching out to the surrounding mines to assist in processing their gold.

{kind=link}

Thanks Ex! I like that mill. Offers a lot of operating leverage to the company and could be a reason for a bigger miner without a mill to acquire them. A pretty awesome situation really.

I was going to post this the other day….from Bullion…..but here it is from zero…

https://www.zerohedge.com/commodities/bullion-bank-nightmare-lbma-comex-spread-blows-again

Let’s hope this doesn’t become the norm in Mexico: https://www.mining.com/web/armed-group-robs-mexican-gold-mine-flees-in-plane/

The good news is that a robbery is less likely at a Silver miner as they’d have to steal Zince & Lead concentrates, so not nearly as attractive as gold dore.

Aint this last weeks show?

Lets all wait and see what Clive Maund has to say. Maybe gold is on the verge of a precipitous fall, maybe its on the verge of a new all-time high or maybe it goes sideways for god knows how long???

All the gurus…..are lost at this point……Everyone of them has never seen anything like what is happening in the markets and the pretend…Crimex, etc.

Sorry Clive, thats abit of a cheap shot! Couldnt help myself though.

Poor Clive has always had the need to abruptly change his views and it has cost him. For example, he turned bearish way too soon in 2016.

I really liked the interview with Bear Creek Mining. A lot of great information about how they are thinking about the mine. Thanks Cory.

Charles, the interview was with Great Bear Resources (GBR) in segment 4, not Bear Creek Mining (BCM). I just didn’t want you to buy a Silver developer instead of the Gold explorer featured in this interview by accident. May the Schwartz be with you!

Yes. I saw my error and responded that I got my bears mixed up LOL!! I guess my response didn’t go through, but thanks for having my back in any event!

No worries. There are a lot of bears out there….

Just to muddy the waters there is also the new Russian Silver Producer Silver Bear (SBR)

GDX is again above the 200 day MA:

https://stockcharts.com/h-sc/ui?s=GDX&p=D&yr=1&mn=0&dy=0&id=p40674266362&a=724328673

It is also above important speed line resistance as well as an important Fibonacci fan resistance (blue):

https://stockcharts.com/h-sc/ui?s=GDX&p=W&yr=8&mn=3&dy=0&id=p68073313171&a=685496339

Price is again above the 30 week MA which is now pointing up so we are probably in for another good week…

https://stockcharts.com/h-sc/ui?s=%24GDM&p=W&yr=4&mn=5&dy=0&id=p85383449376&a=731189324

$GDM and GDX have closed above the 50 day EMA for the last 4 days and are now above the 50 day simple MA:

https://stockcharts.com/h-sc/ui?s=%24GDM&p=D&yr=1&mn=0&dy=0&id=p88003027287&a=734136732

In real/purchasing power terms, the USD has been in a cyclical bear market for 4 years…

https://stockcharts.com/h-sc/ui?s=%24USD%3A%24GOLD&p=W&yr=6&mn=6&dy=0&id=p87066101136&a=723235012

Thanks for the charts Matthew. I was happy to see Impact end the week strong. Brixton didn’t move yet.

Brixton looks very close to moving. BBB is up 43.5% since the low on 3/12 and just had its biggest volume since December 19…

https://stockcharts.com/h-sc/ui?s=BBB.V&p=D&yr=1&mn=5&dy=0&id=p69204781036&a=705725762

I forgot to mention that an insider purchased 100,000 shares on Tuesday.

Thanks for the info Matthew. I bought more shares after we last spoke.

I particularly liked Segment 3 with Brian Leni, from this weekend’s show here at the KER.

The royalty companies are an interesting subsector of the PM space, and I’d agree with the general point that Brian was making that the larger companies are seen as safe accumulation companies, whereas some of the smaller Jr Royalty companies are a bit more speculative.

However, even though there is more risk in the Jrs over the Srs, the Jr Royalty company is still not anywhere close to the same risk profile as the single or dual asset explorers are. He mentioned them both being risker than the Sr Royalties, so at that point he’d just want the exposure to the individual explorer. While I love exposure to a few high quality explorers, they are not nearly the same thing, and still have radically different risk profiles.

There are 5 primary reasons Jr #Royalties companies are far less riskier than Jr #Explorers:

1) because some of the Jr Royalty companies like (Maverix, Metalla, EMX, Sailfish, Anglo Pacific Group, Altius, etc…) do in fact have paying NSRs (which explorers don’t)

2) As for the Development projects in their royalty portfolios, these assets actually have exposure to known deposits with ounces locked in the ground, and with a far higher likelihood of making it into production than an explorer with so many unknowns does. Known ounces in the ground get re-rated higher with rising metals prices, and marketing fluff from most explorers does not.

3) The Jr Royalty company is far more diversified across a half dozen or often dozens of projects, where a Jr Explorer has exposure to 1-4 main projects, and likely only has the budget to drill or explore 1-2 of them at any given time. The Jr Royalty company has drilling and development going on so many more projects, which increases the likelihood of success. While this may also limit upside on a discovery, it also allows for multiple discoveries in one season, and again, also limits downside if a company doesn’t find an economic deposit. It is just far less risky is the point.

4) The G&A & operational expenses of the Jr Royalty company is substantially less than most explorers, and the staffs are much smaller, no helicopters, no winter camps, no building of roads, etc… Which also brings up the point that most Jr Royalties don’t continually dilute their shareholders to oblivion, raising money several times a year to drill, drill, drill and possibly hit pay-dirt, like the Jr Explorers have to. Jr Royalty companies have optioned out or sold out their properties to other companies retaining the NSR and future payment stream off production, but don’t have to do any of the work, or may have only done limited work before optioning the project out. That’s a big difference, as the waves of dilution and spending from Jr Explorers has to hit enough and often enough to grow the value of their project, or they will eventually fail and punish shareholders in the implosion.

5) Jr Royalty company often gives an investor exposure to multiple Jurisdictions, and greatly reduce the Jurisdiction Risks associated with most Jr Explorers. There are a few diversified Jr Explorers, but that is less attractive, because it splits their focus, logistics, abilities to work in both areas simultaneously. With the Jr Royalty companies the work is all being carried out in multiple Jurisdictions by their respective operators, and they are enjoying the fruit of that labor.

The royalty/streaming model is definitely less risky than the miners but then the metals are much less risky than the royalty companies.

More risk still equals more upside potential, generally speaking.

When pension funds start to look for yield would they go to streamers or major miners first.

They may go with either, or I could see them getting exposure to the ETF (GDX) which already has a basket of the larger streamers & royalty companies and the larger producers.

When big funds look for capital appreciation, they will look at miners first.

Newmont is up almost 50% versus Franco Nevada in the last 3-4 weeks and 90% versus Royal Gold since last August.

https://stockcharts.com/h-sc/ui?s=NEM%3ARGLD&p=W&yr=3&mn=11&dy=0&id=p48219888973

In 2016, FNV roughly doubled and RGLD went up 3.5 times but well-chosen miners did far better. My three largest positions averaged more than 1,000% for that move.

The royalty stocks are great but they lack the lottery ticket potential that miners can offer.

Yes, the royalty companies are for more conservative steady growth, for a portion of one’s portfolio for less risky growth, or for investors or funds that don’t want the higher risks of individual miners. I could see a pension fund that is more conservative opting for the royalty companies or an ETF over individual producers, but could see hedge funds and smaller family funds preferring the individual stocks.

The royalty model is extremely appealing. My problem with such companies comes from the fact that they do their best exactly when the miners are the least risky and doing their best: in the middle of a strong bull market.

I know it’s hard for most here to imagine now, but there will come a time when the down days are consistently outnumbered by the up days and corrections less protracted. Bargains will become hard to find as a large speculative bid will semi-permanently underpin the market. So the opportunity cost of holding the royalty plays could be great but most won’t believe it until they see it (i.e., it’s too late). Of course I could be wrong but I don’t think so. Those seeking maximum leverage to the metals will find it in the miners.

I own some shares of FNV in the small retirement account I manage, and we thinking of selling it for something with a bit more torque, either a smaller royalty or a large cash flowing miner with a good low cost structure. I was thinking Agnico Eagle as I already own NEM and GOLD in the account, or maybe Abitibi Royalty which I believe has the royalty on the Malartic Mine that Agnico owns. Not sure either is a great buy here, but thought I would though it out for others thoughts. Thanks for any better ideas?

Agnico Eagle is one of the best run Senior Gold companies so it is a solid pick.

As for the royalty companies you could step Franco Nevada down to one of the mid-tier’s like Sandstorm or Osisko Gold royalties, or in the Junior Gold Royalties Maverix, Metalla, EMX, Abitibi Royalties, and Ely Gold Royalties are all solid picks with incoming cash flows.

Sailfish has 1 royalty paying from Endeavour Silver’s El Compass, but it will really hit it’s stride when Mako Mining goes into production in the next year or so, or when Watertown gets Spring Valley & Moonlight going.

Globex Mining also has 1 Zinc royalty starting this year, but other royalties about 1-3 years off.

Golden Valley Mines has 45% stake in Abitibi Royalties (as GZZ is the parent company that spun out RZZ), and it has other Net Smelter Royalties with Bonterra, Sirios, and Val-d ‘Or Mining.

Coral Gold & Sabina Gold & Silver both have nice single royalty assets n their portfolios, but I believe those will get sold or monetized by one of the other royalty companies eventually.

As mentioned up above and also Brian brought these up in his Segment 3, there are also Altius & Anglo Pacific group that are both cash-flowing Base Metals, Coal, Uranium, Oil & Gas, and limited PMs royalty companies.

(RZZ) (ATBYF) Abitibi Royalties – Corporate Presentation:

(GZZ) (GLVMF) Golden Valley Mines – Corporate Presentation:

https://www.goldenvalleymines.com/investors/presentations/GZZ-Jan2020-Website.pdf

(ELY) (ELYGF) Ely Gold Inc – Corporate Presentation:

https://elygoldinc.com/assets/docs/presentations/2020-04-01-CP-ELY.pdf

(FISH) (SROYF) Sailfish Royalty – Corporate Presentation:

https://sailfishroyalty.com/wp-content/uploads/2020/01/FISH_Corporate-Presentation.pdf

(EMX) EMX Royalty Corp – Corporate Presentation:

https://www.emxroyalty.com/site/assets/files/3325/emx_royalty_corporate_presentation.pdf

(MTA) Metalla Royalty & Streaming – Corporate Presentation:

(MMX) Maverix Metals Inc – Corporate Presentation:

https://www.maverixmetals.com/site/assets/files/3748/mmx_presentation_february_2020.pdf

Agreed Matthew. I love speculating in the higher risk Explorers, or even the Developers & Small Producers with a lot of exploration upside. Cheers!

Royalty companies are a different risk profile in ones portfolio and are more like the PM version of dividend paying blue chips of the generalist investor portfolios.

GDX:GLD looks good. Note the 233/377 MA golden cross…

https://stockcharts.com/h-sc/ui?s=GDX%3AGLD&p=W&yr=5&mn=6&dy=0&id=p44772994888&a=728086896

Silver is up 38% since bottoming at 11.64…

https://stockcharts.com/h-sc/ui?s=%24SILVER&p=W&yr=7&mn=3&dy=0&id=p39848673486&a=547788271

Gold is worth 77 barrels of oil. That’s more than 12 times what it was in mid-2008. Miners are no doubt locking-in a bunch of it near the current price.

https://stockcharts.com/h-sc/ui?s=%24GOLD%3A%24WTIC&p=W&yr=15&mn=0&dy=0&id=p21675652216&a=729961718

Datacloud, $TV Trevali partner to boost orebody evaluation efficiency

Amanda Stutt | April 10, 2020 #Zinc

“Seattle-based mining technology company Datacloud has partnered with Trevali on orebody evaluation at their Caribou mine in New Brunswick, Canada and at Rosh Pinah in Namibia, using cutting edge technology to provide information on ore-waste boundaries and to identify mineralized zones.”

https://www.mining.com/datacloud-trevali-partner-to-boost-orebody-evaluation-efficiency/

3-Phases of a Baer Market

https://seekingalpha.com/article/4332439-profits-and-earnings-suggest-bear-market-isnt-over

Are we in Phase 2 now?

Some nice technical chart analysis of the current situation compared to the Dot.com (2000) and Fincial Crisis (2008)

https://realinvestmentadvice.com/technically-speaking-fed-goes-all-in-whens-the-bear-market-rally/

DOC‘s opinion on this would be interesting

4-Phases of a Full Market

https://seekingalpha.com/article/4336397-technically-speaking-4-phases-of-full-market-cycle

Are we in the Distribution Phase?

Nobody has really talked about Uranium much lately. Are we there yet?

Hi Charles – I’ve brought up Uranium news, company updates, spot price green shoots, etc.. here but hardly anyone ever responds (although Snowy & Wolfster had some good comments recently, and Mr T occasionally touches on Uranium)

Really Ceo.ca and Twitter are a bit better platforms for Uranium sector updates, but with Cameco shutting down Cigar Lake for an unknown time period with Covid-19, Rossing Uranium mine not dealing with certain countries, and the Kazakhs curtailing some production, it is a perfect storm of supply destruction. The working group for the Trump Administration has advised buying some for a strategic supply, and it was line-itemed in the proposed budget, but there is no telling what will and won’t make it into that budget. Spot prices moved up for the first time in the while last week breaking above the $24-$26 channel up to $28+ and many of the miners responded strong to this. I posted some of the double-digit moves in the miners earlier this week.

World’s Largest Uranium Miner Cuts Production; Price Starts to Run

April 7, 2020 – Derek Macpherson | VP, Equity Research Analyst – Red Cloud

“Pandemic related production cuts have translated to the uranium price increasing as the 2020 supply deficit grows. Kazatomprom announced that as a result of COVID-19 countermeasures being implemented in Kazakhstan, 2020 production guidance was reduced by 4,000 tU (~10.4M lbs U3O8e). This production cut along with already announced shutdowns from other producers of at least ~2.4 Mlbs U3O8e drives our current estimate for 12.8 Mlbs supply deficit in 2020, which is 6.7% of estimated market demand. It is important to remember that only a few weeks ago we had expected the market to be roughly balanced (~0.2M lb deficit). The sudden and now substantial market deficit has resulted in the spot uranium price increasing 14% since March 23, 2020.”

https://s3-us-west-2.amazonaws.com/cdn.ceo.ca/1f8sk0p-20200407-Kazatomprom-Curtailment.pdf

Uranium Squeeze Creates A Bull Market For A Fuel In Decline

Tim Treadgold – Apr 8, 2020

“Uranium, however, has become the best example of supply being withdrawn from the market with a trickle of mine closures becoming a flood over the past four weeks, starting with Cameco, Canada’s uranium leader, mothballing the world’s biggest uranium mine, Cigar Lake.”

“The southern African country of Namibia, which has a big uranium industry, dropped out of the market after it followed the example of its neighbor, South Africa, ordering the closure of all mines.”

“But what ignited the latest upward surge in the uranium price to $28.70 a pound was a move by the government of Kazakhstan to place restrictions on its big uranium industry, a move which could see global supply of the nuclear fuel reduced by up to 10%.”

John Quakes @quakes99

“TD now estimates 124M lbs 2020 #uranium production + 24M lbs secondary supply + 7M lbs inventory sold = 155M lbs Supply vs 179M lbs #nuclear fuel demand (excluding Cameco Spot purchases & 3X initial fuel loads for X/53 reactors under construction) = -24M lbs #U3O8 2020 deficit.”

Thanks. I need to review some charts. I am totally out currently.

Hey Ex……after pointing out the orezone warrants that don’t expire til 2023 I looked at the risk/reward and put a bid in last week that got filled. I’m remaining bullish about gold despite the contrarian indicator.😎

Hi Wolfster – Do you have a ticker for those warrants?

Hey Charles. They trade on the venture ore.w

Nice. I’ve got a position in Orezone with the just the general shares, and am happy to hold that for now, but you may be wise to have nabbed those warrants.

Looking forward to what happens next with Orezone:

1) Do they develop it into a mine on their own like Hummingbird and Roxgold?

2) Do they get bought out by a bigger producer that will takeover the project?

Their plan is to have first Gold pour in 2021, so they’ll either raise the capital and build it themselves, bring in a JV partner that can build and operate the mine, or get bought out at this point. We’ll see how it goes…

(ORE) (ORZCF) Orezone Gold Corp:

Gold squeeze potential

https://investmentresearchdynamics.com/a-slow-motion-short-squeeze-in-gold/

Matthew and Excelsior, Is this a good time to buy silver, or should I wait for a pullback after its big gains the last 2 weeks? Thde silver futures are down over 35 today.

Bono, personally I would buy some now and more on a bigger pullback even if that pullback starts from a higher level.

Thanks, Matthew. I did buy some PSLV last week, but want more.

Yeah, nothing wrong with buying in tranches to average into a good cost basis. No reason to go all in on any purchase with so much volatility, but also no reason not to get a tier in place.

Gold up 30%…in a yr……

No reason, it can not go higher………jmo

Big thanks to Cory & Big Al & all the KER contributors for another great week of daily editorials and another weekend show.

Ever Upward!