First Cobalt Update – The US Cobalt Acquisition Is Closed, What’s The Strategy Now?

First Cobalt President and CEO Trent Mel joins me to provide a recap of the energy metals, particularly cobalt and lithium. We then discuss the takeover of US Cobalt and how the Iron Creek Project in Idaho plays into the move toward production strategy. With a fully permitted refinery in Ontario the Company is undertaking a study to weigh it’s options on how to maximize cash flow in the near and long term.

If you have any follow up questions for Trent please email me at Fleck@kereport.com.

Click here to visit the First Cobalt website for more information.

Click download link to listen on this device: Download Show

Or You HAVE “SMART MONEY” EXITING…………….

https://www.zerohedge.com/news/2018-06-05/smart-moneys-bailing-markets-become-too-complacent

This new system is slowing down the process of input…….and a pain……for real….

Entertainment………….35,000 Indictments ………..

https://www.youtube.com/watch?v=nfkqmrIEcX4

This is not an endorsement on the subject matter ……just info. on the sealed indictments , I thought might be of interest to those following “Q”

$hui with black candle so far today. If it closes black, it strongly suggests today’s tiny pop in silver is going to be reversed soon.

SIL and AXU also saying today’s pop in silver is bogus. Of course this could change by the close, but as of 12 est, it’s not looking good.

I’ll still maintain that silver and the silver miners aren’t going anywhere this year. If SIL can can get it’s 50 WMA to solidly cross above its 100 WMA, you’ll know I’m wrong.

When the 50 WMA crossed below the 100 WMA in most silver miners last year, it was a very clear signal that the silver miners were going to be dead money for a long time.

$XAU’s 50,2 daily bollinger bands are the narrowest in their history.

Everything up big, dollar down big….

PM miners flat to down. The whipping boy of the investing world loves it.

(??) Silver & Gold miners were up today overall.

Here is the reality in the Silvers for those that care about facts over whiny narratives.

> Symbol – Silver Producers – % Chg

SMT.TO Sierra Metals Inc. +3.77%

BHS.V Bayhorse Silver Inc. +3.13%

EXK Endeavour Silver Corp. +2.89%

AG First Majestic Silver Corp. +1.82%

TAHO Tahoe Resources Inc. +1.72%

SSRM SSR Mining Inc. +1.56%

USAS Americas Silver Corporation +1.46%

HL Hecla Mining Company +1.34%

CDE Coeur Mining, Inc. +1.03%

EXN.TO Excellon Resources Inc. +0.71%

HOC.L Hochschild Mining plc +0.64%

FSM Fortuna Silver Mines Inc. +0.54%

MYA.V Maya Gold and Silver Inc. +0.39%

PAAS Pan American Silver Corp. +0.08%

>> Symbol – Silver Explorers & Developers – % Chg

NNA.V New Nadina Explorations Limited +14.29%

SDRG Silver Dragon Resources Inc. +11.84%

BNKR.CN Bunker Hill Mining Corp. +10.53%

SMI.AX Santana Minerals Limited +9.09%

IVR.AX Investigator Resources Limited +8.33%

MMG.V Metallic Minerals Corp. +7.41%

G1A.AX Galena Mining Limited +6.90%

AHNR Athena Silver Corporation +6.33%

REX.V Orex Minerals Inc. +4.00%

BCK.V Blind Creek Resources Ltd. +3.85%

GRG.V Golden Arrow Resources Corporation +3.37%

MTR.L Metal Tiger plc +2.94%

SVB.TO Silver Bull Resources, Inc. +2.70%

NUAG.V New Pacific Metals Corp. +1.35%

BCM.V Bear Creek Mining Corporation +1.04%

SIL.V SilverCrest Metals Inc. +0.78%

MAG.TO MAG Silver Corp. +0.47%

(GDX) VanEck Vectors Gold Miners ETF – up (+0.45%)

(SIL) Global X Silver Miners ETF – up (+0.49%)

(SILJ) Prime Junior Silver ETF – up (+1.35%)

Gold price: Investors are pouring $1 billion per month into ETFs

Frik Els | about 11 hours ago

http://www.mining.com/gold-price-investors-are-pouring-1-billion-per-month-into-etfs/

This kind of super flat MACD for silver on the daily chart pretty much guarantees a very sharp drop soon. See Nov-Dec 2017 as the last example. Silver never ever starts a sustained bull run from this type of MACD action. Any pop up is nothing but a shorting opp. before the plunge.

All they need is 5-10 days to destroy silver price.

yup, Dent could still be right.

And the sasquatch might roam a flat earth!

+2 haha!

Dent has been calling for $500-700 Gold as “iminent” for years and years and could not have been more terribly Wrongo in the Congo.

The fact that people give him more than 10 secs of their time more that once is amazing.

iminent = Imminent

A crash in Gold to $700 or $500 was BS for the last 5 years and people that jumped on the Dent bandwagon have a dent in their heads.

Just for fun,

can you tell me how that is any dif from the people on this site and others saying “buy buy buy” “any day now” “here we go” etc etc for years as we came down from the high?(which you were both a party to)

Mathew and his ipt comes to mind, repeated “Im adding” etc and where it go?

(Mat wouldnt stop posting about ipt)

Thats just one of course.

Im sure Mat will have lots of explanation why he was right all along and Im nuts,

but ever since jumping from 11 cents in jan 2016 it really hasnt done much.

yes yes yes, 11 to $1 + is good. But $1 to 40 cents is not.

And yes you can “rifle” approach others but I think its rather obvious metal hasnt been the place to be.

My point, is just that you guys like to jump on Dent, or maybe anyone that doesnt agree with your outlook, and the thing is, you have not been any more “right” and a good argument can be made that you have been less “right” than guys like spanky for example.

I just dont think you should be so quick to judge and know Dent is wrong.

Personally, I have no idea and dont claim to.

OK, now tell me about all his bad stuff, but be fair and dont leave off all the bad stuff from the guys you like so much too.

Like S Thompson etc

“gold will never go below $1500 again” J Sinclair

“silver will never go below $30 again” David Morgan

Dent has easily been as “right” as these guys.

This is all just for fun remember.

Ex, why dont you write another post about the deep state or religion or aliens or sumtin, you come up with great stuff.

It would help relieve the boredom of watching our metal rust away. lol

With all do respect b, I posted about IPT a helluva lot more last fall as it was on its way to making a major low. Contrary to your childish (and bitchy) characterization of my posts, they tend not to contain your dumb phrases (“buy, buy, buy”, “here we go”, or “any day now).

Following that heavy focus of mine, it went up 120% while most of its peers went nowhere or down. At the moment, it is still up 55% since December and is in Stan Weinstein’s stage 2:

http://schrts.co/5rny3f

I don’t know if you’re nuts or not, but something is clearly wrong with your understanding of the situation for you to take Dent seriously.

Sinclair and Morgan don’t have much to do with anything but at least they understand the macro drivers of the metals. Dent does not.

You consistently provide no useful analytical commentary, b, but plenty of head-shakers like the following contradictory sentences:

“I just dont think you should be so quick to judge and know Dent is wrong.

Personally, I have no idea and dont claim to.”

{kind=link}

I can’t speak for others, but my approach for 6 years here has been to trade the rips and sell the dips in the mining stocks, and when reviewing the metals I take a technical approach looking for support and resistance levels.

I’ve never said “buy, buy, buy” or “here we go” unless I was discussing short or medium term moves. I’ve never been in the Gold to $5,000 or $10,000 later this year like Bo Polony and most of the KWN crew.

Both extremes are tiresome, and that is why I focus on the technical set up in the metals for the macro picture of how things will effect the individual Jr miners. I also spend 2/3 of my time on looking for unique stories in the Jr miners on a Fundamental basis that may cause them to outperform.

Thanks for the compliment on the other treads (ie deep state, religion, and aliens, etc…). I try to keep those posts limited to the appropriate editorials where those topics come up unless a wild discussion breaks out. 😉

You guys have never said “its a good time to buy?”

ok.

I got a giggle from the response tho.

Some people are kinda easy to get a reaction from. lol

I understand completely you guys are after a few points here and there.

I think weve been all over that.

Not my thing but there are a few ways to play the game.

to itch his own.

PMs will get going again, I sometimes wonder if I’ll be alive to see it, but it will move again.

From Ricks emails he’s been hitting some winners but not with PMs as far as I can tell.

Pots been ok and could be a profitable hold for awhile.

Cant see too many people jumping on Dents bandwagon, I would think the gamblers would be shorting the dow or nasdaq, gold has been boring.

Mentioning Dent is a guaranteed rise outta you guys tho.(always fun)

About your comment that I dont give valuable analytical info? sumtin like that,

I was the person saying to buy a half cent share just before the jump in 2016, analytical or not 1/2 cent shares blew your recommendations away.

Not that they were bad, just not as profitable as mine.

You did ok tho, for a chart guy.

I was the person said POT POT POT!!! lol just before it went from…what was that?

50 cents to $14? with lots of trade-able moments.

you were focused on metals.

hmmm, whose recommendations were better at the time?

Analytical?

Thats the thing, when you say I dont provide info etc what you mean is, not YOUR info, not a CHART guy info about metal.

There is more than one way to play markets.

Maybe this weekend I’ll post some steller Dent stuff.

Perspective matters. For example, AXU is well below its 2016 high but still 6x its 2016 low…

No one is saying new bear market lows…

Look at AMD’s weekly chart from about 2006 to present. I don’t think it dropped below its 2009 low, but it did essentially triple bottom over a span of 7 years before really looking legit.

> On January 24, 2018 at 11:36 am,

spanky says:

“Like I said Matthew, some day, some day.”

“Some day I will be dead and buried. Maybe then these miners will catch a bid.”

“When gold puts in a short term top, the silver miners are going to test if not break their December lows. Where is the smart money? Still shorting apparently.”

> On March 16, 2018 at 10:38 am,

spanky says:

“Unfortunately $silver is not going to do squat ahead of the FOMC meeting. Needless to say it looks extremely sick on the weekly charts in pretty much every aspect and even a tiny nudge lower could send it into a prolonged downtrend. Honestly is looks like 2000 all over again, where it based out for a couple of years prior and then broke down along with the stock market and drifted lower for 2 years.”

“The fact is since 2016 silver has made higher lows and lower highs. That’s not exactly a screaming bull market. Looks more like multi year basing to me with the possibility of new multiyear lows just like from the mid 90’s through 2002.”

I bought a lot of Brixton Metals today has it had a nice shakeout similar to the one AXU had 2.5 years ago.

http://schrts.co/tdgzLp

Nice. I’m well positioned in both both Brixton and Alexco and expect them both to surge higher later in 2018 and moving into 2019.

Advancing High Potential Gold & Silver Projects – Brixton Metals $BBB $BXTMF

Cambridge House International – May 22, 2018 Corporate Presentation #VIDEO

This was another high grade hit: #DrillPlays

(BBB) (BXTMF) Brixton Metals Drills 1.98% Cobalt, 15,436 G/T Silver over 1M Within 7.87M of 2,787.26 G/T Silver, 0.27% Cobalt and intersected 70.65M of Nickel – Cobalt – Silver in Archean Basement

May 9, 2018

Invest Yukon panel discussion at CMS 2018

#TheNorthernMiner – May 25, 2018 #VIDEO

Panelists: Stephen Mills, Deputy Minister Energy Mines and Resources, Government of Yukon; Graham Downs, President/CEO , $ATC ATAC Resources Ltd; Clynton Nauman, President/CEO , $AXU $AXR Alexco Resource Corp.

Building out a World Class Silver Asset – Alexco Resources (AXU) (AXR)

Cambridge House International – May 22, 2018 Corporate Presentation #VIDEO #Yukon

(AXU) (AXR) Alexco Resource Corp. Announces Increase to Bought Deal Offering of Flow-Through Shares

June 4, 2018

“Gross proceeds from the sale of the Flow-Through Shares will be used to fund a surface exploration program, continue the underground drilling program at the Bermingham deposit, and also continue development of the Flame & Moth decline at the Company’s Keno Hill Silver project by incurring qualified expenditures. ”

https://ceo.ca/@nasdaq/alexco-resource-corp-announces-increase-to-bought-a553e

Agreed Matthew. Many of the Silver stocks held onto a big chuck of their 2016 impulse leg up and are set up to climb much higher once the spot gets back up into the $18-20 range.

Another example is (EXN) Excellon Resources. It surged from it’s low in early 2016 of $.19 up to a high of $2.40 for an 11-bagger (a huge move indeed), and then has trended sideways to down to $1.42 today; a 44% retracement of that initial uptrust.

Excellon has fared much better than many PM Jrs that pulled back 50-90% of the first leg of the new bull market. Definitely one of the better performers in the #Silver space, and it outperformed most of the Gold miners as well.

The nice thing to consider is how much further $EXN still has to go to even get close to its 2011 highs, and this time it will have dry mining conditions and much better costs 😉

> This Chart will put things into perspective, but it is a pretty nice set up so far off the 2016 bottom:

EXN also gave back half of its 2016 gain but has held up well compared to many.

However, it is currently less appealing than many of those peers and I will be somewhat surprised if it remains a top performer during the next rise in the sector.

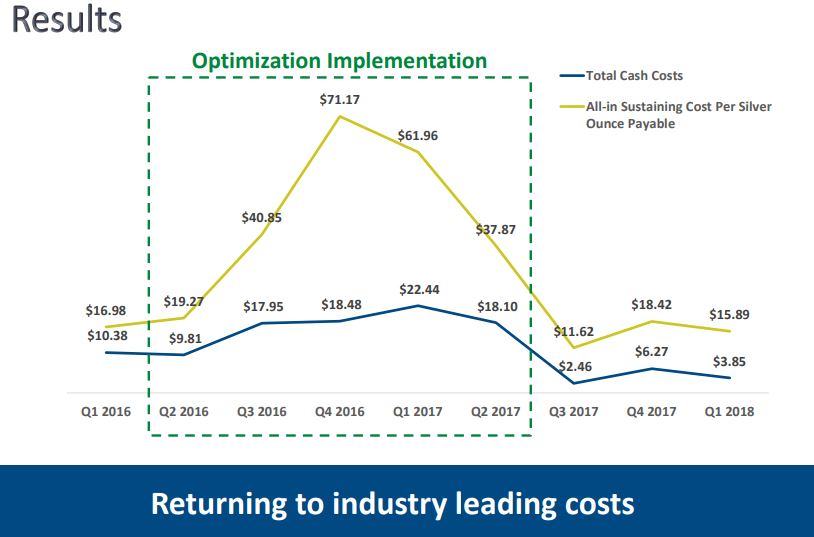

Yes, it has held up well compared to many, but also has many good fundamental drivers. They spent 2015-2017 in a rough spot processing old lower-grade stockpiles as they dewatered their mine, so their AISC shot up high, but now costs about 1/4 the of where they were at the 2016 peak.

___________________________________________________________

Here is a visual on how their costs went up during the last few years when processing their old low-grade stockpiles and dewatering and how they are currently trending:

http://cdn.ceo.ca/1dhbqeh-Returning%20to%20lower%20costs.JPG

{kind=link}

___________________________________________________________

They are also absolutely nailing it with exploration results that are super high grade over and over again. There is real value creation going with their expansion of the deposit around their La Platosa Mine and they are also getting ready to start focusing more on their next exploration/development project Miguel Auza (which had a previously operating underground mine in the past).

What is also encouraging about the La Platosa is how much larger that deposit can grow. Most CRDs on their trend are about 10-20 times larger, so there is plenty of room to grow the asset base there.

> Here is a map showing the average size of other Carbonate Replacement Deposits along trend in Mexico:

http://cdn.ceo.ca/1dhbq96-Excellon%20-%20In%20the%20CRD%20shadow%20of%20Giants.JPG

{kind=link}

(EXN) (EXLLF) Excellon Drills 2,318 G/T Silver Equivalent Over 6.76 Metres At Platosa

July 26, 2017

http://www.excellonresources.com/news/details/index.php?content_id=169

(EXN) (EXLLF) Excellon Drills 2,255 g/t Silver Equivalent Over 11.1 Metres At Platosa

September 6, 2017

http://www.excellonresources.com/news/details/index.php?content_id=171

(EXN) (EXLLF) $EXN Excellon Drills 2,648 g/t Silver Equivalent Over 9.1 Metres At Platosa

February 22, 2018

http://www.excellonresources.com/news/details/index.php?content_id=181

(EXN) (EXLLF) Excellon DrillS 3,428 g/t Silver Equivalent Over 10.2 Metres At Platosa

May 31, 2018 – #DrillPlays #Exploration #Production #Mexico

High-grade results from existing mantos include:

– 2,148 g/t Ag #Silver, 19.2% Pb #Lead and 9.7% Zn #Zinc or 3,428 g/t AgEq over 10.2 metres

– 1,153 g/t Ag, 8.2% Pb and 3.4% Zn or 1,662 g/t silver equivalent over 5.3 metres

– 870 g/t Ag, 13.3% Pb and 12.4% Zn or 2,034 g/t AgEq over 6.7 metres

http://www.excellonresources.com/news/details/index.php?content_id=187

The only other companies hitting regular drill hits of that high of grade are Alexco & Metallic Minerals in BC, and Silvercrest in Mexico.

Ex, what you’re missing is that all that “quality” is precisely (and seemingly perversely) what could hold it back. As any investment prospect becomes more of a sure thing, you can usually expect less upside.

Leverage comes from a risky place, not from fat profits and/or few unanswered questions. This is why SIL and even SILJ were smoked by many very small juniors in 2016 yet generally outperformed during the correction that followed.

Note that had IPT held up as well as EXN, my position would probably be just 10 or 20 percent of what it is right now. As I pointed out last fall, I had only 45,000 or 50,000 shares by the time it went below 60 cents last year. By January, I had over 1,000,000.

I prefer to bet on the companies that deliver consistent leverage and have less of their potential already priced-in.

Hi Matthew – Yes, I completely get that point the riskier the perception then the correlating torque to the upside as it surprises the markets by increasing revenues on a larger percentage basis versus more established companies.

This is precisely my point on Excellon (EXN), as it is still very much an underdog with a bad past perception that is working hard to blaze a new trail, and when it get’s rerated upward by the marketplace, it should have quite a move.

EXN is still not seen as a “sure thing” by any stretch of the imagination, despite all their good work. There have been plenty of investors mocking it as simply an Eric Sprott/King World News pump and dismissing all their great drill results and improving cost structure.

Recently some blog commentators went after EXN for not being as profitable as they would have guessed based on the high-grade drill results, but it completely escapes those dingbats that Excellon sunk millions into their mine to drop 2 wells and install the pumps to access the high grade portion of their mine, and as a result, they processed old low-grade stockpiles and this is why their costs were so hy and profits were so low. Hardly anyone is running numbers based on their new costs or the significantly higher grades.

Some still believe their mine is totally flooded or that they have water issues, when they’ve spent year effectively pumping down the level of the aquifer and now have dry mining conditions for the first time in years and are just now hitting their high-grade ore (unbeknownst to most drive by observers).

Lastly, people always knock on how small La Platosa is, but that was my point above (and the point they make in the Corporate Presentation) that most CRDs on their same metals trend in Mexico have deposits that are about 10 times as large.

None of this is being factored into their current share price, and the market yawned a their killer drill results, to chase other shiny exploration narratives that mostly blew up on them. Eventually investors will wake up to just how much Excellon is doing right, and how much they’ve turned their company around.

It is exactly the “risky” nature that many perceive that is why I still hold the EXN position as I expect a major rerating over the next 1-2 years once they put a few more quarters together to prove to the marketplace that they are executing.

None of this is being factored into their current share price?

You’re making some wild assumptions there, Ex. My approach is the opposite. I tend to assume that the price makers at any given time have deep pockets and a thorough understanding of value. In fact, when ipt and usa traded at .11 and .05, respectively, I made the case that they were properly valued considering the difficulties of the time. My bet was that silver was about to move and that that would change things for the companies.

Some smart people are following exon and they know exactly what the drill holes mean.

Exn not exon.

Following its own shakeout on Monday, EXN’s daily does look good to go…

I’m not making wild assumptions Matthew. I follow the comments over at ceo.ca, stockhouse, hotcopper, other stock boards and most are discounting Excellon’s ability to grow their deposit larger, only looking at their quarterly income statements without considering how processing the lower grade stockpiles or all the money put into dewater affected their profitability, and I see comments all the time about how their mine is still flooded, which is divorced from the reality that they have dewatered a considerable part of that aquifer to access the high grade mantos and now have “dry stockpiles.

Just this week the Angry Geo put out a hit piece ripping on some of those same things and many followers of hers blindly cheered the grilling.

That tells me very clearly that most investors are not getting the message and it isn’t being properly valued at present. When Silver prices rise it will surprise folks not paying attention as their economics will improve suddenly and provide nice leverage.

I’m sure a few noticed the high grade drill results, but it shocking the disconnect from many of the hyped up discovery narratives, versus some of the more legitimate developers and producers with economic deposits that are hitting much better grade and not barely moving.

I’ve reposted their drill results a few times when people get giddy over 200-600 g/t silver narrow .05 – 2 metre incepts on other explorers still trying to figure out if they have an economic deposit, and in contrast EXN has 1000-3000 g/t wider 6 -12 metre silver incepts and have a real mine & mill where things can be monetized.

If those hot exploration stories had those results the stocks would be going parabolic and some days the EXN even pulled back after putting out stellar exploration results.

It isn’t wild assumptions, as I’m watch some of these stocks every day like a hawk, and check on the sentiment from a number of sources. I’m not saying EXN will be the top performer, or is without legitimate risk, but when the next few quarters of results come in with them mining the higher grade stopes with lower costs, then a significant rerating should be in order.

BTW – Monday was when the ridiculous hit piece came out against them that didn’t factor most of the points laid out above into the sloppy analysis. Proves the point.

Ex, that’s not analysis. Who cares what the peanut gallery has to say about the stock? Those bashers are probably helping it since bull moves end when everyone has drunk the kool aid.

Learn to read charts; exn is quite loved. Fundamentally, it is also not cheap when compared to its peers — both small and large.

Yes, it’s a pretty wild assumption that it should be higher and that the market doesn’t get it but you do.

I maintain that it’s an ok value that can become much better as silver moves up and plans are successfully executed.

IPT represented a very good value at the December low which is why it doubled versus the metal it mines while the metal went nowhere. EXN has done the opposite and is down significantly versus silver ytd.

EXN:SLV http://schrts.co/hina4i

True, deep values don’t tend to last long and are usually brought about by some external circumstance (like Resolute dumping IPT; a strike; or a general market crash).

IPT:SLV

http://schrts.co/vvVTGU

With the Jr miners the “Peanut Gallery” are the very ones that bid up a stock or run for the exit doors, as these equities are very thinly traded. It doesn’t take much volume to send them screaming higher or crashing lower, and it is rarely orderly, like you’d see in a much higher volume blue chip stock.

There are tons of market participants and funds there to keep the pricing mechanism rational in the larger general equities, along with tons of mutual funds, ETFs, and pensions invested in the bigger names that don’t trade in and out of the stocks in mass on a daily basis and hold them in relatively strong hands day in and day out. Obviously we aren’t talking about Microsoft or Cisco here, where there is so much volume each day that it truly doesn’t matter what the peanut gallery thinks.

With Jr miner the stocks are often valued completely irrationally and the market is very inefficient, so I don’t buy the concept that the market makers always have things at the right price. That’s baloney.

If that were true you wouldn’t see companies trading for less their cash or less than their assets. If markets were always priced correctly then you wouldn’t see Golden Valley priced at such a discount to Abitibi Royalites. If deep pocket market makers had all these stocks in check then you wouldn’t see insane nosebleed valuations on explorers that haven’t even sunk their first drill hole. Jr miners are undervalued or overvalued all the time, and yes, it is possible to find stocks that priced in a way that makes no sense that can be capitalized on.

In 2015 I was also buy Scorpio Mining (before it merged with US Silver & Gold to form Americas Silver) because the valuation made no sense relative to peer valuations or the assets they had in the ground. Their costs were really high (just like Excellon’s were the last 2 years) and they developed a strategy in 2016 to start bringing those costs down and improve metals recovery, so that was a setup for a rerating.

Yes, obviously a rising metals prices will give the miners a serious boost, especially the ones right on the fence of being quite profitable (but that are not there quite yet as they make improvements). That is what attracted me to Claude, Lake Shore Gold, Crocodile Gold/Newmarket, etc…. and it is what attracts me to Excellon at present.

I never said anything about being the only one uncover this value, as there are others that can see the disconnect in many of these miners, but it is rubbish to think that Mr. Market always has companies priced to perfection. It doesn’t. We can use the technical indicators to trade a stock, but there are also clearly fundamental drivers that can move these stocks a great deal.

This is precisely why Novo resources can have a 35% down move in 1 day off a bad/confusing press release. There was nobody technically calling for a 1 day -35% move, even if they thought there was a pullback overdue, and that’s why fundamental news still plays a role in valuing these stocks (not just 100% TA).

The markets are out of wack and mispriced all the time, especially in sectors like mining were 99% of the investors and funds are totally uninterested and few are following the thousands of mining stocks to make the pricing mechanism work correctly.

Onne widely followed Newsletter Writer, can move a Jr Mining stock in a day just as much as a large fund buying/selling when their throngs of followers/subscribers mindlessly hede their recommendations. We see it all the time with Brent Cook or Eric Coffin or John Doodys newsletters, and in both directions (stocks surge on their pumps, and stocks fall on their critiques). The Angry Geo piece hit on Monday and clearly it had an affect where the stock sold off hard with a long red candle.

I may not be as good at charting as you, but I’m not new to the concept by any stretch and can read the chart just fine and can see it held onto it’s gains, much better than most of the Gold or Silver stocks over the last year, and thus why it hasn’t moved up as much as IPT since December, because it hadn’t been crushed down so low either. IPT had more room to move up after being reduced by so much since the 2016 high, and we’ve discussed this before that it is one of the most highly torqued stocks in the sector. I don’t know why you have to bring it in to every single discussion on Silver stocks, as not everyone wants to put all their eggs into just 1 basket, and some investors have lower risk tolerances and don’t want every holding to be that volatile.

IPT isn’t a one-size fits all stock that is good for everyone at all times, and has it’s own issues like no defined NI 43-101 resources, higher operating costs calculated in a weird way because they aren’t allowed to use AISC without calculating reserves like other companies, and now they are starting to focus on Gold exploration as well, which dilutes down their Silver purity narrative. Again, I own it, like it, and have traded it a number of times on technical setups, but nobody saw that fund liquidating shares last year on a chart until afterwards. If they had an environmental issue, or a series of poor drill results, or decreased revenues, etc.. it would hit their share price regardless of the technical set up.

I agree that true deep value doesn’t usually last long if it is a sudden event or 1-off news story, but there are plenty of miners that got hit hard with a 20-50% sell off and don’t recover long after the news has been resolved because investors throw away stocks due to irrational fears or concerns long after turnarounds are well underway and their is a delay effect.

Look at how Jaguary suddenly dropped huge when that fund liquidated shares, (for no fundamental reason… and they put out a press release saying there was no fundamental reason) but it hasn’t recovered back to anywhere close where it was before that fund decided to sell. So did Mr Market have it priced right before that fund sold or after. It was damn cheap compared to it’s peers before that happened and crazy cheap afterwards. Sorry there isn’t some deep pocket market maker keeping that all on track.

Mandalay resources had mine flood when a lake wall collapsed and it killed 2 workers and it tanked hard. It has compensated for production by increasing at it’s other 2 mines, and is outperforming many other producers on throughput, recovery, and with lower costs. Why isn’t it valued where similar miners with the same levels of production are valued? (Because the markets are inefficient) They do very little promotion, and no newsletters cover the stock, and as a result it languishes while other turds float.

I see a similar situation with Excellon, just not as extreme. It has held up well and kept a big piece of the gains from the 2016 surge, but sold off a bit since the beginning of the year PM rally, where as other stocks that were more beaten down have moved up more.

Again, Excellon isn’t my favorite stock pick or anything, but it definitely is misunderstood by most mining investors at present, and there is value there. I hold dozens of mining stocks for completely different reasons – some are for gradual growth with royalties or streams, some are drill play lottery tickets, some are developers moving into production that will have the “golden runway” effect, some are takeover candidates, and some are highly torqued producers that will get rerated with improving margins.

Different strokes for different folks….

Uranium Weekly – Kazakh curtailment and Yellow Cake IPO

June 5, 2018

“Ux Consulting’s (UxC) spot uranium price indicator increased by $0.60/lb this week to $23.35/lb (+2.64%). Two developments had a positive impact on the uranium

market over the past week, namely announced supply cuts from Kazakhstan and a planned uranium holding company IPO. The Trump administration also announced that it is seeking ways to support nuclear power in the United States.”

“Late last week, the Kazakh Energy Minister announced that the country’s uranium production target for 2018 has been lowered to 21,600 tU, down ~6% from the

original target of 23,000 tonnes”

“Yellow Cake IPO planned for July in London. Yellow Cake is seeking to raise between $150M to $200M, which it will use to buy 8.1mm pounds of U3O8, according to news reports. The company has already struck a deal with Kazatomprom, the world’s largest uranium producer, to buy up to $170M of the metal at a 7.7% discount to the current spot price. In addition, it has an option to purchase a further $100M of uranium each year from the company for the next nine years”

SLV managed to get above the flat topped red Ichimoku cloud on the daily chart, right at the transition zone. While downside is possible, the lower border of the red cloud should be the absolute lowest price should go (if it even manages to break below the top border). So no imminent smash lower (at least for now), IMO.

Wow, I spoke way too soon about silver. It’s reversed lower hard now. Looks like it will probably close below the cloud transition. Total fakeout. Par for the course. No break above the $16.70 level until mid July at the earliest.

Based on the SLV weekly Ichimoku cloud, there isn’t any possibility of sustained upside until October.

Silver was up to $16.92 earlier today and is currently at $16.75.

Kitco has 16.68 now. Silver is head lower.

Look at the SLV weekly Ichimoku cloud. The earliest silver can break out for good is October.

Silver at $16.85 . It broke above $16.70 both yesterday and today, so I don’t follow your point…

here is a Silver chart to keep up with the daily gyrations.

Sometime between now to the next 8 trading days gold is going to bust out of its wedge. The BBands are getting tight on the daily finally. The way the 50 is crossing under the 100 and widening while turning south and price being flat sure looks bad..

Either way it goes, we’ll know within two weeks. About the time the 50 crosses under the 200.

FANG BREAKOUT…………Or Not………

https://www.zerohedge.com/news/2018-06-05/faang-stocks-majority-breaking-out-bullish-patterns