Hour 1 – The Key Characteristics To Understand This Market Pullback

Click download link to listen on this device: Download Show

Another volatile week for US equity markets. With the NASDAQ on track for the worst month since November of 2008 we all need to address the likelihood of this correction continuing. In this weekend show we look at what has lead to this correction as well as how this pullback is different than others.

Please keep in touch by emailing me at Fleck@kereport.com. Also please click on the links below for all the company updates direct for management that we recorded this week.

- Segment 1: Jeff Christian, Managing Partner at CPM Group shares his thoughts on what it will take to shift investor sentiment towards gold.

- Segment 2: Mike Larson, Editor of the Safe-Money Report breaks down just how bad it is getting for US markets including the financial sector.

- Segment 3: Chris Kimble, Founder of Kimble Charting Solutions shares the importance of trend lines and moving averages when assessing the overall health of the markets. We use the HUI/SPY chart as an example.

- Segment 4: Extended Interview – Dan Oliver wraps up the first hour by looking at the credit markets and outlining how corporations are getting squeezed with higher rates.

Exclusive Company Updates This Week

Segment 1

Click download link to listen on this device: Download Show

Segment 2

Click download link to listen on this device: Download Show

Segment 3

Click download link to listen on this device: Download Show

Segment 4

Click download link to listen on this device: Download Show

Agreed. Mad props to the KER crew and all the contributing guests.

Ever Upward!

Agreed. Mad props to the KER crew and all the contributing guests.

Absolutely, the boys are always fascinating and much appreciated. Great interviews!

Ever Upward!

Well, maybe not so much for the conventional market.

😉

Good macro comments from Dan Oliver, and always good to hear Chris Kimble’s technical views. Jeff Christian is good to hear from for the pulse on the metals, and Mike had good macro comments as well, and it is encouraging to hear a generalist paying a bit more attention now to the PMs as a chaos hedge, along with currencies, and volatility instruments.

Cory – That was one of the better Dan Oliver interviews you guys have done to date.

CRASH! Late in October 2018, the stock market looks to me like it is ready to break. There have been other bad breaks but this time the World is sitting on a huge debt bomb. There are more people than ever seeing the “Big One”, but like in all cases of speculation when a bad break occurs speculators think it is a good time to buy. Back in they rush and they will have no trouble finding investment trusts willing to sell their unwanted securities. The room is full of people rushing to sit down before the last chair is pulled away. The only way out is for humans to feel the pain. CRASH! LOL! DT

Agreed. But I’ve been thinking this for years. When it gets ugly instead of a crash the markets go back up. But the debt is untenable and must eventually be dealt with.

Thanks for another great lineup of guests!

Here is a good article with good crosses with gold and long term charts.

Gold Reaches Another Milestone This Week

by Gary Wagner – October 26, 2018 #TechnicalAnalysis #Charts #VIDEO

https://thegoldforecast.com/video/gold-reaches-another-milestone-week

Ira Epstein’s Metals #Video (10/26/2018)

Technical Analysis, Gold, Silver, Copper, Platinum

GDX, Nasdaq, & Gold Stock Trade Tactics

Morris Hubbartt – posted Oct 26, 2018

Super Force #PreciousMetals #TechnicalAnalysis

(double click blue links to watch #VIDEO TA segments):

Stock Market Crash & Gold Price Update

iGold Advisor – Christopher Aaron – Oct 24, 2018 #TechnicalAnalysis #VIDEO

Yamana Gold sells Gualcamayo to Mineros in $85 million deal

MINING.com Editor | about 19 hours ago

Gualcamayo is an established producing mine with a long operating history. The mine is on track to achieve Yamana’s 2018 gold production guidance of 100,000 ounces.

The Gualcamayo acquisition adds 491,000 ounces of gold in reserves and 2.28 million ounces of gold in indicated mineral resources, representing a 56% and a 142% increase, respectively, to Mineros’ current reserve and resource base.

http://www.mining.com/mineros-acquire-gualcamayo-gold-mine-30-million-deal-yamana-gold/

$LMC Leagold said restarting Santa Luz mine in Brazil requires $82 million

Cecilia Jamasmie | a day ago

http://www.mining.com/leagold-mining-said-restarting-santa-luz-mine-brazil-requires-82-million/

So after paying a bunch to take over Brio Gold…. Leagold still has to raise $82 Million to get their mine into production (which is a process never without speed bumps during the first 3-6 months).

Looks like LMC could have skipped taking over Brio Gold and just raised $3 more and taken over a fully functioning 100,000 ounce per year operation at Gualcamayo from Yamana and been far better off for it on the dilution to the prior shareholders before their merger.

> It looks like a buyers market for picking up producing mines at present.

I realize those mines may not be a mirror match, but dang, they paid a ton to take over a company and then still have to raise a ton more money go through all the startup issues that any new mine has. Based on what other operating mines are selling for in other transactions, it makes more sense, in many cases, to wait on buying development projects in lieu of just grabbing a producing asset on the cheap.

At this point in the cycle, it seems more economic to take over a full mine like what Mineros is doing from Yamana. That is exactly what First Majestic did when they took over Primero’s operating San Dimas mine, or what McEwen did by taking over Black Fox mine from Primero, or what Bonterra just did taking over Metanor’s Bachelor Mine mine, or what Golden Reign is doing taking over Marlin Gold’s Lt Trinidad mine, or what Alio did by taking over Florida Canyon from Rye Patch.

This was clearly the draw in Monarques taking over Ricmont’s 2 mine before Alamos bought them out, and what Hecla was doing taking over Klondex’s operating mines.

Seems like the smaller 1 or 2 mine operations would be the best takeover candidates for the larger mining companies, with these low valuations. After taking over the smaller 1/2 project producer, then all the larger multi-mine company has to do is bolt on that mine or mines to their existing operation, and optimize them for better costs and margins, and they’ve added the most value the quickest.

I believe we’ll see about a dozen takeovers of small/mid-sized producers over the next 12 months in the Gold & Silver sector for just these reasons.

This tweet from Palisade Radio also reminded me that Equinox also just bought out the Mesquite mine directly from NGD New Gold for a steal.

>> It truly is a buyers market for picking up producing mines on the cheap.

_______________________________________________________________________________

Why does Ross Beaty need to build another #mining company?

He tells us his investment thesis as to why. #RossBeaty $EQX Equinox Gold Corp

https://twitter.com/PalisadeRadio/status/1056518703620198400

I initially did a swing trade in Equinox (EQX) coming out of the gate with all the fanfare, but then sold out. However, I recently started building my position back in $EQX again and feel at ease with Ross Beaty a the helm. He’s said a few times it is the last Gold company he’ll build, so why not jump on for the ride?

I had watched (LGC) (LGCUF) Luna Gold get off to a rough start and saw (SAND) Sandstorm look for options on how to save things. Then (TREK) Trek Mining tried to initially roll them up with the merger with $JDL (a prior rollup of Lowell Copper, Gold Mountain,and Anthem United).

Well, Trek never got trekking, but but then they ultimately merged with (NCA) NewCastle Gold and (ANF) Anfield Gold to form the modern day (EQX) Equinox Gold.

I was concerned they’d shelve some of their assets, but then they sold their Koricancha mill in Peru to (IO) Inca One (which I was a fan of for Equinox monetizing it, but also because it really helped Inca One turn the corner and I expect more people will pick them up on their radar as a good toll processor in Peru over the next year. IO is dirt cheap right now).

Next, EQX spun out the Copper assets into Solaris (which really deserved it’s own vehicle as many of those projects were scouted out by David Lowell himself).

Lastly EQX just bought the Mesquite Mine from (NGD) New Gold for a good deal, and while NGD needed the cash, Equinox got the longer term win here and saved themselves years of work finding/developing/permitting a 3rd mine and just bought one. Very well executed.

There are lots of moving parts in the rollup of assets & spinout/divestment of other assets regarding (EQX) (EQXFF) Equinox Gold, but they have a good pipeline to work from now with 3 mines and a solid team. Wish Ross all the success he deserves, but something tells me, with so many well known key investors, that this one is destined to shine. Ever Upward!

Serial Entrepreneur | Ross Beaty Outtake

Real Vision – Video Interview

Mining tycoon Ross Beaty back in the spotlight with Equinox Gold (EQX)

Pan American Silver founder and Canadian mining tycoon Ross Beaty hasn’t led a company for nine years, but that will change once Trek Mining, NewCastle Gold and Beaty’s own Anfield Gold merge.

“To build a nice mid-tier gold producer is something I wanted to do for the last couple of years,” he told BNN in an interview. Trek and NewCastle each own one major asset (in Brazil and California, respectively), and Beaty’s Anfield has the capital.

Beaty says that the new company will focus on two projects, both past-producing operations.

(SGI) (SUPGF) Superior Gold has really been sold off hard here, and yet their production was solid (25,000 ounces in the 3rd quarter isn’t a reason for panic selling), but it looks like a large investor did liquidate a position on Oct 19th creating large selling pressure. Their economics are are better than the share price would indicate with their $22 Million cash, no debt, AISC around $1000.

The sentiment seems overly bearish in Superior Gold all things considered, so I grabbed a small starter position back in this stock the end of last week and will be adding to it through year-end, as it will likely be re-rated up on par with other peers doing roughly 100,000 ounces a year in a safe jurisdiction.

___________________________________________________

(SGI) (SUPGF) Superior Gold – Corporate Presentation:

They did 25,842 ounces in Q3 (not soft by any stretch but some wanted to see a few thousand ounces more) and 25,797 in Q2 and if they keep that up they’ll be producing 100,000 per year. Granted in Q1 they were at 18,940 so they need 29,421 in Q4 to hit 100,000, but those are still great results, and if they keep doing 25,000 ounces per quarter then they’re on track for the 100,000 ounces per annum run rate by Q1 2019. Their AISC is around $1000 which is fine at today’s metal prices.

One unique opportunity lately (like we saw with JAG and IPT) was a large fund or investor sold on the 19th (maybe for a tax loss due to the pullback the stock experienced), so they likely had an annual loss they are taking in 2018. Their loss is our gain….

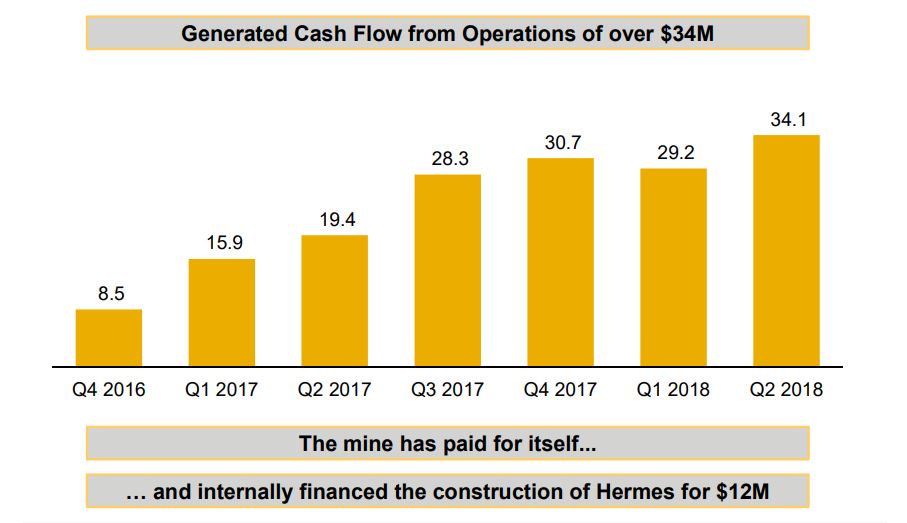

Most miners struggled this year, but Superior Gold is churning out results at a good cost basis and thus producing cash flows from operations to fund other initiatives.

http://cdn.ceo.ca/1dt8n4n-Superior%20Gold%20Free%20Cash%20Flow.JPG

{kind=link}

What’s important about generating cash flows like that is that this funds growth, and rencently funded their new open pit mine Hermes; (without diluting the snot out of existing shareholders, like most companies would do).

There is plenty of room for expansion there at Hermes and also at Plutonic where they’ve been doing a lot of successful exploration. Once again, they have the incoming revenues to fund their exploration organically like a real business, without the never-ending capital raise that explorers and developers most come back to the market for time and time again.

Over the last decade the Plutonic mine has been converting mineral resources and unclassified material into production (which wouldn’t show up in the life of mine based on their defined reserves), so one has to be careful not to throw out the baby with the bathwater in that regard, as the common knock against them is the limited mine life.

This “short mine life” argument is often tossed out by investors that expect all companies to blow through insane amounts of money to produce a 10-20 year mine life. Why the hell would they?

The market is NOT rewarding that use of capital at present, and that would be the wrong call, and it’s the wrong investor expectation at this point. When the cycle gets hotter and expectations change, then they’ll prove out a longer mine life when the underlying metals prices make the exploration costs worth it.

For now I’d rather see just enough exploration to grow the operation, good acquisitions & development, and money put into mine & production expansion (like what they’ve done with their 2nd mine Hermes). $SGI’s plan makes sense.

Here are some interesting comparables on $SGI versus some of their peer Gold producers, from their Corporate Presentation:

http://cdn.ceo.ca/1dt7h8q-Superior%20Gold%20revaluation%203.JPG

{kind=link}

Here’s another good comparable slide from their Corporate Presentation:

http://cdn.ceo.ca/1dt7han-Superior%20Gold%20revaluation%202.JPG

{kind=link}

One last slide with comparisons against some of Superior Gold’s peer producers:

http://cdn.ceo.ca/1dt7hbr-Superior%20Gold%20revaluation%201.JPG

{kind=link}

I bought some Novo on Friday after the price drop. I think they should buy a washplant and a couple of Bulldozers and start making money, it’s too bad it isn’t The Yukon where they have lots of water. Quinton is a brilliant geologist but he is no hard rock miner. When you listen to him explain the gold deposits on their properties it makes me think this guy could be talking theories for the next five years when what is needed is production. That maybe Bob M’s call but I agree. DT

I’ve almost pulled the trigger on Novo a few times in the last 2 weeks, but keep buying smaller distressed producers or adding to medium sized producers that are on sale. I also threw a little more at Uranium & Lithium stocks on Thursday and Friday as they continued correcting, for some energy metals.

Maybe on my next winning swing trade I’ll stash a little over in Novo and get a starter position going again.

Excelsior, whar are your favorite plays in the Lithium space?

There are quite many and it is not so easy to pick the right ones.

Nemaska for example is fully financed and well below the financing.

I have owned & traded around my positions in Galaxy Resources, Nemaska Lithium, and Lithium Americas since 2015. I have owned Pilbara Resources since early 2017.

In the past I also held positions in Orocobre & Neometals , but don’t currently hold those. I’ve considered picking up positions in Critical Elements Corp & Altura Mining, but never pulled the trigger.

There is also MGX Minerals that claims they can extract Lithium out of old oil/gas wells, but not sure if they’ll ever prove their case definitively. If they could it would be a game changer, but it’s remained a speculative stock the last few years.

One thing to note is that last year’s beauties are often the next years divorcees.

Many of the darlings of last year like Novo, Garibaldi, Aurion, Metallis, Bitterroot, De Grey, Arizona Silver, New Range Gold, Secova Metals, and Ascot Resources have had a steady decline down over the last year as seen on this chart.

Then again, this years beauties and popular drill plays and even some of last quarters momentum stocks are already sold off hard and have created a new flock of speculative bagholders. The inflows are very fickel in any of these “discovery” narratives over the last few years.

Sokoman Iron, Golden Ridge, Aben, Medgold, Juggernaut, Pacton, NV Gold, Metals Creek, Blind Creek, Gungnir Resources.

And that brings us to the flavor of the day……

Like all the previous companies mentioned, this next crop of drill plays has tickled the fancy of the speculative hordes.

These are in their speculative prime at present, where valuations get divorced from economic reality due to runaway narratives, and most of these (despite putting out good drill holes) will pull back down once their pump has passed. (just like most of the others above made near return trips).

> Granted, a few of these stocks will go on to be winners as they are most followed at present (not the bottom dwellers), but in fairness, so were the companies listed above in the previous 2 charts over the last year or two.

Evrim, RNC Minerals, Westhaven, GT Gold, Great Bear, White Gold, Serengeti, Sable Resources, Wallbridge, Triumph Gold.

So the better question after looking at 30 stocks that already popped is…..

Who will be next in the discovery game of speculative herd flow?

I had a look at your chart, that is really neat, or like my sons say COOL! DT

🙂

Goldcorp CEO: ‘Nothing Is Broken’ Despite Plunge In Shares

Allen Sykora – Friday October 26, 2018

https://www.kitco.com/news/2018-10-26/Goldcorp-CEO-Nothing-Is-Broken-Despite-Plunge-In-Shares.html

The Dow transports are heading lower:

http://schrts.co/kDx7sv

Zoomed-in:

http://schrts.co/EcqgjK

SPY is down 13% vs GLD in just one month:

http://schrts.co/3wSZZB

The USD has proven less of a safe haven than gold as SPY is down about 9.5% vs it in one month:

http://schrts.co/tKJDBn

SPY does not look good at all and is extremely unlikely to be worth the risk for “buy and hold” types anytime soon…

http://schrts.co/ysEoXo

On October 15 the $BPGDM flashed a bull alert on the point and figure charts. This has been a fairly good predictor in the past but not necessarily an exact timing indicator.

Zinc market tightness confounds bearish expectations

Reuters | 3 days ago

http://www.mining.com/web/zinc-market-tightness-confounds-bearish-expectations/

Unsure if anyone has posted this link previously?

Apologies if so….

But I thought this keynote speech by Grant Williams about gold was fantastic.

What do you all think about his reasoning ?

Gold…Cry Wolf.

https://www.realvision.com/grant-william-keynote-speech

Cheers,

Skeeta.

Thanks Skeeta, Grant is always worthwhile.

I’ll let you know if I think there’s anything wrong with his reasoning — and I doubt that there is.

As you can see at about the 22 minute mark, gold at $1200 today is the same as $35 in 1971 or $255 in 2001 relative to the monetary base. So, for a buy and hold, one could do a lot worse than to buy gold today instead of worrying about dramatic new lows.

This sort of perspective is always important to note as I think alot of us get frustrated by golds price movement in a short to mid-term time frame, myself included. A buy and hold strategy with gold stands the test of time. I guess patience is a virtue.

I don’t know about you but the gold price would never frustrate me at all if it weren’t for it’s impact on the miners.

Gold is the least stressful asset to trade.

Rick Rule: Tremendous Discoveries In “One of the Last Great Exploration Frontiers”

by @sprottmedia on October 28, 2018

Ex. – you must have had me in mind when you made this post. Thanks as always for the info!

I’m a fan of West Africa, and hold a few Gold stocks in that area that are cheap in comparison to many of their peers on other continents.

Rick made some good points about how investors are overly concerned about the jurisdiction risk in Africa, while shrugging off the very real jurisdiction risks in NorthAmerica and Australia that are sometimes just a big of an issue for permitting or running a project.

There is no doubt that politically many countries can turn on a dime, but that’s also true in South America, which isn’t punished nearly so hard. Then there are places like Indonesia where majors operate that are far more risky than Africa, and yet “conservative” investors have no problem buying their stock.

There are risks and rewards all over the planet, but I find the gold miners in West Africa and even parts of the Nubian shield to offer good probabilistic set ups for outsized rewards versus the risks.

Interview with Dan Oliver > I listened 2x. The interview was 17 minutes. The information provided could have been said in 2 minutes. Worse, everyone knows that the “gold stocks” are leveraged to the price of gold. Everyone knows there will yet be once again a time when both rocket higher. It always boils down to “TIME” & “PRICE”. but the GURUS will NEVER commit to a forecast of BOTH together. They are professional HUCKSTERS. And they are damn good at what they do.

Thanks as always fella’s for your efforts in putting the weekend show together.

Much appreciated.

Cheers.