Goliath Resources – 3 Vancouver Conferences, 70 Gold Drill Assay Results, Complete Ownership Of Golddigger, Buydown Of NSR, and Increased Stakes From Rob McEwen And Crescat Capital

Roger Rosmus, Founder, CEO, & Director of Goliath Resources (TSX.V: GOT) (OTCQB: GOTRF), joins us live from the AME Roundup to highlight the positive investor sentiment after attending 3 back-to-back Vancouver resource conferences. Additionally, we dig into recent news released on the final 70 gold-only drill hole assays returned from last year’s program, the pending assays for 110 multi-element results on all the 2025 drill holes, along with a number of corporate initiatives around not doing a share consolidation, on buying back the NSR from 3% down to 2%, and on fast-tracking its ownership in the Golddigger Property located in the Golden Triangle, B.C. that hosts the high-grade Surebet gold discovery from 49% to 100%.

- Drill hole GD-25-319 intersected 19.13 g/t Au over 6.10 meters, including 22.86 g/t Au over 5.10 meters, including 29.09 g/t Au over 4.00 meters in quartz-sulphide veins, part of the Golden Gate Zone

- Assays are still pending for 110 drill holes from 2025 for multi-element gold equivalent (AuEq) results. These results will be released in the near future once all assays have been received, compiled and interpreted.

- 100% of the drill holes completed to date, have all intersected gold mineralization clearly demonstrating the remarkable continuity, grades, and widths in 5 Main Gold-Rich Zones comprising 46 mineralized lodes that remain open for expansion.

- Of the holes drilled during the 2025 campaign, 83 out of 110 holes (or 76%) contained visible gold to the naked eye (VG-NE).

- The fully funded 2026 drill program will be mainly focused on expanding the 5 Main Mineralized Zones. Data compilation and interpretation is underway which will be used to vector in on the indicated Motherlode causative intrusive source to this extensive high grade gold system with widespread VG-NE.

As part of the transaction to J2 Syndicate Holdings Ltd. to acquire 100% ownership in the Golddigger Property, that Goliath is now set to publish a Maiden Resource Estimate (MRE) on the Golddigger Property before June, 1 2030 and on every 3 year anniversary of June 1,2030 thereafter vs. the prior requirement, in the original agreement, to publish the MRE by June 1, 2027.

- Roger outlines the Company’s rationale that it makes far more sense to keep expanding the mineralization with aggressive exploration programs, versus trying to pin down the MRE at this stage.

- He provides both positive examples of companies that have taken this route, versus the negative examples of companies that rushed to put out a MRE, only to fence themselves in with regards to valuations and market perceptions.

Wrapping up, we reviewed that in December cornerstone investors Rob McEwen and Crescat Capital increased their stakes in the company, as well as discussing the optionality that Goliath has with regards to their equity holdings of McEwen Inc shares which have essentially gone up about 3X since acquiring them. In addition to future conversion of warrants from Rob McEwen, the (MUX) shares provide the option for more capital inflows into the company treasury to fund more exploration.

If you have any questions for Roger about Goliath Resources, then please email us at Fleck@kereport.com or Shad@kereport.com.

- In full disclosure, Shad is a shareholder of Goliath Resources at the time of this recording and may choose to buy or sell shares at any time.

For more market commentary & interview summaries, subscribe to our Substacks:

The KE Report: https://kereport.substack.com/

Shad’s resource market commentary: https://excelsiorprosperity.substack.com/

Investment disclaimer:

This content is for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any security. Investing in equities and commodities involves risk, including the possible loss of principal. Do your own research and consult a licensed financial advisor before making any investment decisions. Guests and hosts may own shares in companies mentioned.

Click here to follow the latest news from Goliath Resources

.

.

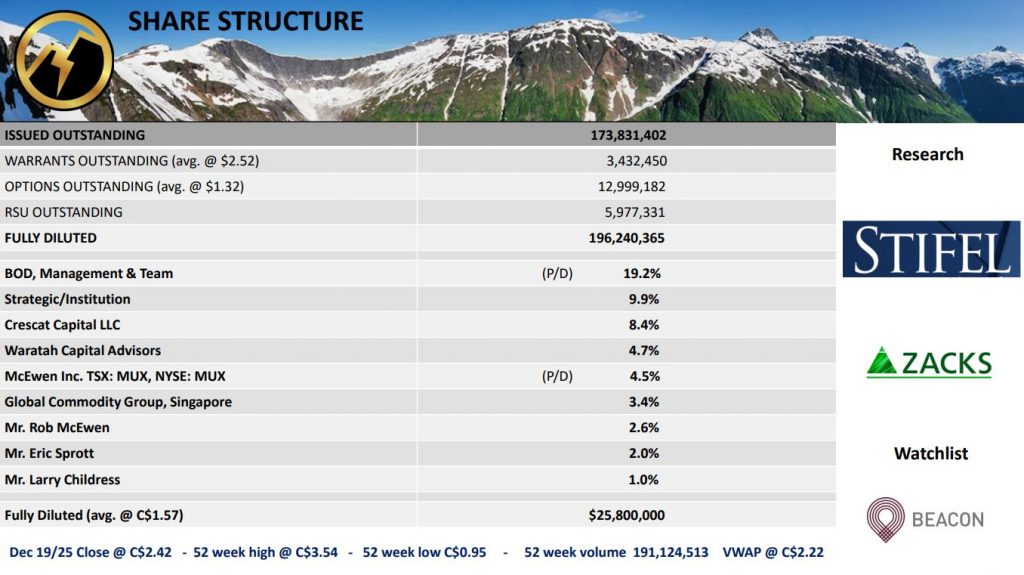

Yeah, it’s pretty telling that Rob McEwen and Crescat are increasing their stake, and that Larry Childress came in last year, along with the global commodity group fund from Singapore. Eric Sprott got involved earlier on, and there are a number of US and European financial institutions getting into position, taking the shares from retail investors that are getting sir crazy.

Smart money has been getting into position for some time for the larger journey.

Based on this discussion, I decided to go up and post the capital structure and key stakeholders in Goliath up above from their corporate slide deck, so that anyone can see the impressive roster for a junior exploration stock.

Even for me personally, I hold 19 gold stocks, but the vast majority are junior and mid-tier producers or gold developers with defined resources and economic studies in place.

I only hold 2 gold explorers at present (Goliath and Dryden Gold). I did have a 3rd one (Collective Mining) but it got a bit to pricey for me and so I sold it last year.

It has to be pretty special geology and drill results for me to get into a gold explorer pre-resource, and Goliath is undeniably unique and special.

Goliath Resources – Roger Rosmus at Metals Investor Forum 2026 in Vancouver

3 days ago…

Thank you Ex. You are a step ahead as usual. I’ve been meaning to ask you if there were any jr. explorers you owned. In this market jr. producers are where the action is so your owning Goliath now is quite an endorsement.

Thanks Blazesb. Yeah, I’ve continued to stay mostly weighted to the higher torque gold and silver producers, and better developers as that is where the action has been. Stocks like Avino, Santacruz, Discovery, etc.. are up 12X-15X in my portfolio so clearly weighting them the heaviest has been the right approach. Clearly one does not need to only gamble on drill plays to get the proverbial “10-baggers.”

Also a lot of producers have very exciting drill programs on tap that are funded internally — look at the exploration programs laid out for this year with Americas G&S, or Sierra Madre, or Silver X, or even Guanajuato and Impact.

Another example: I just had Mako Mining on the show yesterday and they are drilling this year at 4 different projects, and doing a ton of drilling around their main operating mines in Nicaragua.

Speaking of Nicaragua, remember how much drilling Calibre used to do there before being acquired by Equinox? (there were times they had 15-20 drill rigs going…. now THAT’s exploration).

Even Thor Explorations that I had on the show last week is taking their huge revenues from production and funneling it into exploration and development. They have 5 drill rigs turning near their mine in Nigeria, 3 rigs at their Douta project in Senegal, and 2 rigs going doing grass roots drilling in Côte d’Ivoire. Often times producers are the best explorers, because they are growing organically without the need to continually tap the markets for dilutive financings.

Then there a plenty of quality developers that are doing great exploration work. I literally just got off the phone with the guys over at AbraSilver and they just wrapped up their Phase 5 drilling (now having completed 150,000 meters of drilling on the project) and are immediately kicking off their Phase 6 drill program without even taking a break (except over the holidays).

I had Amex Exploration on the show earlier this month, as a developer working towards a bulk sample and advanced economic studies, and they’ll be doing 100,000 meters of drilling. Again, THAT’s exploration, and it isn’t on a risky drill play poking holes in the ground hoping they find something.

With Goliath and Dryden I’ve been in both the last 2 years because I see an intensity to their drilling, and their results are justifying their thesis.

It’s the same thing I saw with Great Bear a few years back where they were continuing to deliver before being scooped up, or more recently with Silvercrest and Probe before they just got taken out. Then there were explorers that graduated to developers like Vizsla, Abrasilver, Silver Tiger, Scottie, Thesis, Troilus, etc… They put out a few seasons of compelling drilling, building upon the prior years, until they made the move to go into advanced economics and start heading down the pathway to development and eventual production. There are a few more good ones that I missed out on like Snowline or Sitka or Banyan, but they’re all doing a great job too.

There aren’t that many great exploration stories like that which keep delivering year after year, but when people find them they need to get all over them and ride them into the 2nd wave of the Lassonde Curve “pre-production sweet spot” or “golden runway” as Lobo dubbed it.

I’ve been diversifying into several explorers that have been naked shorted to oblivion. Such as SSRSF, wish I’d bought more…

Ex. You’ve asked the question many times recently about the miners not popping as much expected vs the price increases in the metals themselves. How much of a factor is it that the price increases have not come from supply issues only but also the collapse of the US dollar and many of the miners expenses are in foreign currencies???

It’s a good question Wolfster, but to my thinking, it is irrelevant as to the why? and more germane that prices in gold and silver are way up, and yet the valuations in many producers with record margins are not really valued where they should be, and the developers with insanely good project economics at today’s prices are a fraction of where they should be.

To be clear, I’m not saying these stocks haven’t had really nice multi-fold moves or that investors haven’t had a great couple of years of gains… (that is not the point). It is moreso that the valuations have been dragging butt.

Just pull up a chart of the SIL:Silver ratio or SILJ:GDX ratio, or look at GDXJ that can’t even break it’s prior all-time high yet when prices are off the freakin’ charts. SIL just broke out to new ATHs 2 weeks back and it took $86 Silver. That’s nuts. The overall move, considering the move in the metals, has just been way more muted than many would have expected from a valuation standpoint.

The best silver developers are still getting $5-$6 an ounce in the ground in an environment where we are at $114 silver prices as I write this. That’s a HUGE gulf there to fill. I don’t expect them to get full spot value in the ground, but would be it be so crazy to see the very best development projects pulling in $15+ an ounce in the ground valuations at triple digit silver prices?

Look at the takeover of Probe gold at $56 an ounce in the ground. Is that really a “fair value” for one of the best development projects on the sales rack with 10million ounces of gold in a Tier 1 jurisdiction in Canada? That’s pretty lame IMO.

Even the takeovers we’ve seen at $80-$110 an ounce in the ground are lame, when gold has been up at $3000-$5000 during that time period, and producer margins have been $1,500-$2,500. Would it be so crazy to finally see some takeovers at $200-$400 an ounce in the ground valuations? I don’t believe that would be the seniors overpaying in this kind of environment, but we aren’t seeing that.

I think many drive-by investors are so enamored with their stocks moves up of 4x or 6x or 8x that they aren’t thinking critically about the comical valuations and troughs where those moves came from and how undervalued those stocks really still are all things considered.

Now, there were a few days last weeks where many stocks were up double-digits one day, and then double digits again the next day, and THAT is the type of price action we should have been seeing many days in 2024, 2025, and 2026. Instead we saw many days even in the last 2 months where silver was up 5% or 7% or 10% and the miners were up 2% or some days they were even down 2%-5%. THAT is the disconnect that many investors have been underwhelmed with. The bobble-head pundits that are just happy their stocks are going up and in the green don’t get it…

I just did a quick scan of my portfolio and watchlist and amazed that at $112-$116 silver, that isn’t even close to being factored in yet, that there are silver producers and developers in the red down 2%-6% on a day like this, and some of them were down yesterday too. These stocks haven’t even factored in $50 silver, and yet they are dragging their tail ends when silver is at all-time highs and on days where silver is up 6%… it’s really underwhelming, all things considered.

Well it can’t possibly be investor apathy or stupidity. 😜……..certainly makes it feel like it’s still the 3rd inning rather than the 7th. Past runs have seen the 7th be fully valued then the last push higher into irrational exuberance levels.

Yeah, it seems more like disbelief in the metals prices staying up at these levels or investors afraid of buying the top and becoming a bagholder.

Whatever the reason, the underperformance of most silver stocks to the rise in silver is a bit vexing.

Looks like I got into hot chili just in time for the next push higher. Seems under the radar in the west but the aussies are all over it.

Yeah, Hot Chili is waking up and they had a great presentation at the MIF in Vancouver.

Here’s my recent hot take on it from earlier in the month:

https://excelsiorprosperity.substack.com/p/opportunities-in-copper-explorers-6b5

Bonzo’s shares of GOTRF are up 5 fold and he is not selling if McEwen and Crescat are adding to their holdings.