Hour 1 – The Best Investments In 2019 and Stocks To Watch For 2020

I hope everyone had a very Merry Christmas, Happy Hanukkah, or whatever you wish to celebrate. For a week that was supposed to be slow for the markets we saw some impressive moves over the 4 trading days.

In this weekend’s show I focus on recapping the top investments and strategies our guests employed throughout the year. More importunately we also look ahead with predictions on US markets, yields, and the metals sectors.

Please keep in touch by emailing me at Fleck@kereport.com. I love hearing from all of you and wish you all a very happy New Year!

- Segment 1 – Jesse Felder kicks off this hour with what he says was the biggest story in 2019 – the Fed turnaround. As for 2020 we assess the energy market, the possibility of a recession, and his investing strategy starting the year.

- Segment 2 and 3 – Joe Mazumdar joins me for two segments outlining the best resources stocks he followed in 2019 and what he is looking for in terms of different metals and companies in 2020.

- Segment 4 – Josef Schachter wraps up the first hour with a focus on the energy markets. We look ahead to 2020 in terms of what will drive the overall sector and what stocks are set up to best benefit.

The Train to the ( Concentration Camp ) is the internet money electronic dompamine phone brain wash system prison you’r living !!!!! 2020 will consolidation of the Prison ! Green is DEAD !

Cory Big Al ! Tanks and only GOLD and SILVER !!!!

Thanks for the concern and heads up Franky.

A week before Christmas, the Office of the Comptroller of the Currency (OCC) quietly released its quarterly report on trading and derivative activities of Wall Street’s “casino banks” and it shows that GoldmanSachs lost $1.24 billion trading interest rate derivatives during the third quarter of this year.”

Meanwhile, U.S.Congress de-regulates further and the New York Fed relaunches its multi-trillion-dollar bailout funnel. That forced the Federal Reserve to throw a cumulative $29 trillion in all directions to bail out not just U.S. banks on Wall Street but the foreign banks that were on the other side of these reckless and irresponsible derivative trades.

Josef Schachter what happen to one of your top pics Bellatrix Explore. Went bankrupt?

JP Morgan Silver Riggers Survive December COMEX Contract!….BARELY!! (Bix Weir)

Do not buy silver stocks.

Ya never no, maybe he is right.

I wonder what ever happened to that billions of gold in the grand canyon.

J.P.Morgan has reportedly never had a losing day on the COMEX trading.

It certainly must be profitable, since they have paid over $ 30 BILLION in fines for their illegal activity.

Best weekly close in 2.5 years for Kootenay Silver:

https://stockcharts.com/h-sc/ui?s=KTN.V&p=W&yr=5&mn=11&dy=0&id=p58112498352&a=709686500

One of my favourites, KTN

Invested in the KTN warrants exp april 2021, exp 0,55 cad. now 0.09 cad.

Im really excited, like a child at christmas😄

Yup it’s looking good……maybe a little more volume as it goes higher would be nice

Gold peaked this year about 6% above the R2 pivot point. If the same were to happen next year, gold would hit the upper yearly Bollinger Band at 1850. In 2011, it peaked at 14% above R2.

Such a move would require a 22% gain from here, the same as was required this year but significantly less than the 30% gold delivered in 2016. There is very little volume-based resistance above 1530 and the P&F PO is 1950. In addition, the dollar looks set to have a bad 2020 so gold could gain a big tailwind that was absent this year.

https://stockcharts.com/h-sc/ui?s=%24GOLD&p=W&yr=7&mn=7&dy=0&id=p48988360970&a=699861636

Matthew,

Do you have any targets for SILJ in 2020? Could SILJ reach 30 in the next 12 months?

I have been lurking on KER since 2014 and your comments have saved me ton of money over the years.

From Patrick Karim at Twitter

https://twitter.com/badcharts1/status/1210937085366026241?s=21

Blue – Thanks for posting that longer term KTN chart from Patrick.

The HUI was capped by the 100 month EMA in 2016 and again in both August and September of this year but is now set to close this month above it. The last such monthly close happened 7 years ago.

Monthly:

https://stockcharts.com/h-sc/ui?s=%24HUI&p=M&b=3&g=0&id=p40550767508&a=402975041

It also closed above the 500 week EMA for the first time in almost 7 years while reaching its highest level in 3.5 years. A weekly golden cross (50 MA crossing 200 MA) is also imminent..

https://stockcharts.com/h-sc/ui?s=%24HUI&p=W&yr=7&mn=7&dy=0&id=p34027540851

IF we get a pullback here, I don’t think it will last long, maybe a day or two…

https://stockcharts.com/h-sc/ui?s=%24HUI&p=D&yr=1&mn=5&dy=0&id=p40982321627&a=541768212

With all the new weekly MACD buy signals in the mining stocks, the new year should start with money pouring into the sector.

https://stockcharts.com/h-sc/ui?s=%24XAU&p=W&yr=5&mn=7&dy=0&id=p35943393779&a=699164164

With two days to go, ISVLF volume this month is over 6 times the previous month…

https://stockcharts.com/h-sc/ui?s=ISVLF&p=W&yr=4&mn=0&dy=9&id=p75030271177&a=677775870

Matthew – I have a portfolio management stylistic question for you. As opposed to the personal etf approach Ex takes it sounds like you hold fewer concentrated positions and I presume you don’t have any hard and fast rules about trimming positions based solely on a position getting to large. Is that correct. If that is the case, do you have an ideal in terms of the number of positions you hold in any one sector?

Yes, I hold very few positions compared to Ex for several reasons. The more positions you hold, the harder it is to beat or even match the market. It is also very time consuming from an analysis perspective and potentially expensive due to commissions and possibly tax preparation.

My mining portfolio went 7x in 2016 and my three largest positions just happened to be the ones that went 10x. I probably had 10-12 positions at the time. I’d hate to have 3 ten-baggers out of 50 positions.

It is just counterproductive to over diversify since so many miners are not worthy for one reason or another. There are too many that fail to deliver the leverage that makes the risks worthwhile. Mandalay Resources was one good example in 2016. It delivered a measly 130% before topping and ultimately cratering 96%. It looks like a much better bet now, fwiw.

You’re right that I don’t have any hard and fast rules about trimming. Some positions remain too large for extended periods because of my confidence (which is not wise most of the time for most investors). Weekly overbought readings with negative divergences always cause me to sell pretty heavily but I routinely rebalance before such readings if perceived opportunity/risk-reward setups swing wildly between my shares.

15 is about the max number of positions I like for one sector but am often comfortable with fewer than ten.

I would rather trade SILJ than hold too many individual positions.

Thanks Matthew.

As Matthew stated earlier this week:

On December 23, 2019 at 3:11 pm,

Matthew says:

“I get it but think it’s a good idea to remind newbies that it is not possible for everyone to make money. Bull or bear, the great majority loses money (especially when inflation is accounted for).”

As a result, going all in on less than 10 Jr miners is incredibly risky, and not something most investors are equipped to do well. Diversifying across more names, more subsectors, and different commodity or energy sectors, and then letting the few really big winners carry the day works and can still more than outpeform general equities or the ETFs stuffed with mostly larger producers.

This approach can be scoffed at by some, although a successful account management style is just that, but I’d rather water down some potential gains by spreading the risk over a basket of stocks, than be like countless overly confident investors that blow up their accounts taking extremely the extremely high risks betting on only a small handful of stocks in one of the highest fail rate sectors this is.

Bottom line, any approach that has investors outperforming the main indexes is worth considering and all investors have different risk appetites, goal, or experience levels/knowledge. Most investors can not do what Matthew does by betting on just 8-10 stocks and come out with gains on most years. As he mentioned, the great majority loses money.

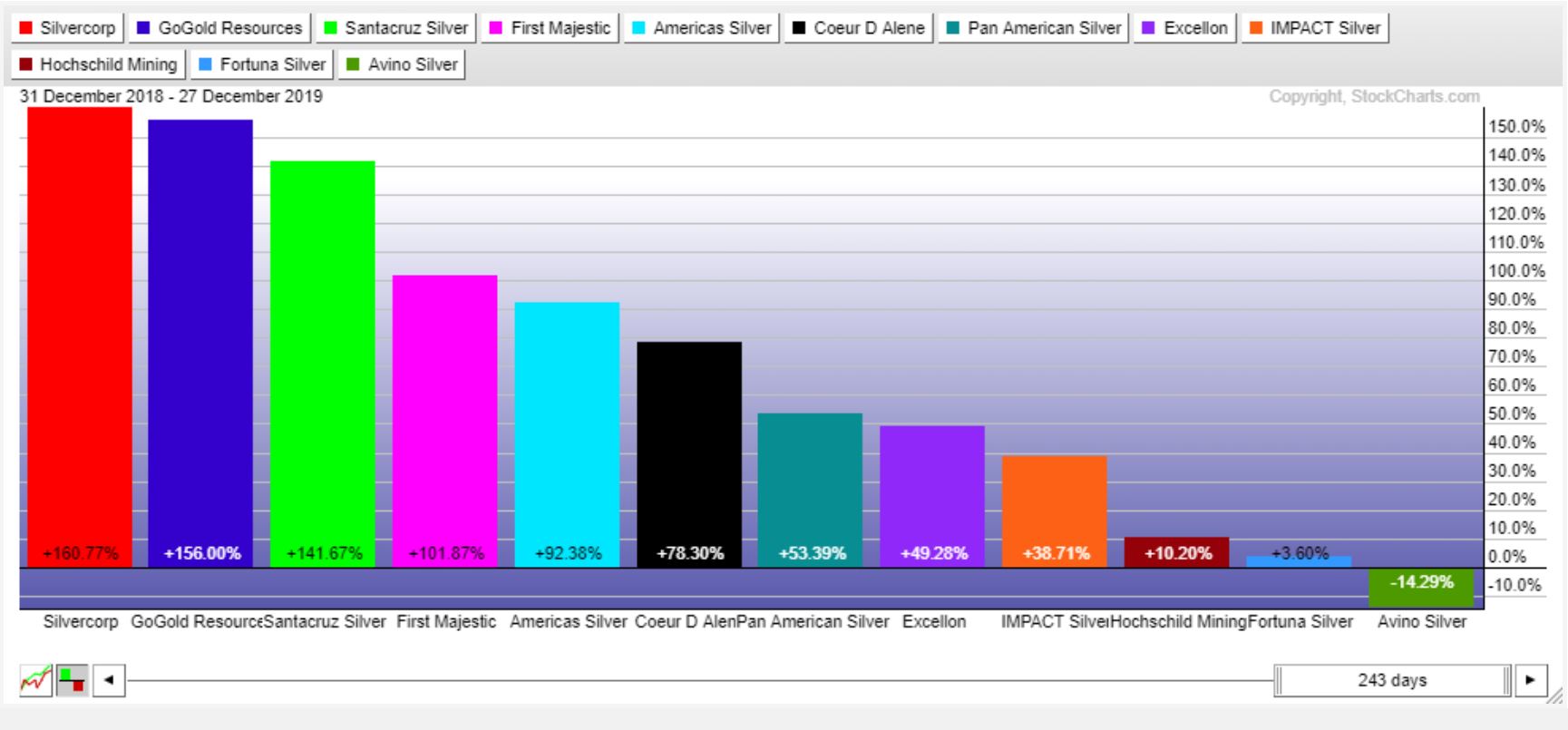

All it takes is one look at the 2019 Year-To-Date Chart in the Silver Producers to see why it makes sense to have a basket of stocks.

> For example: Many on here (me included) are animated by (IPT) Impact Silver in the small producer space, but it under-performed many of it’s peers Silver Producers, so to have gone all-in on it as your only Silver pick would not have had one as well positioned as someone with a basket of producers.

Sure (IPT)did well if looking at YTD returns of 38.71%, but I was sure glad I also had these other producers in my basket that had far better returns in 2019 and offered far better trades.

(SVM) up 160.77% YTD,

(SCZ) up 141.67% YDT

the over-hyped/over-loved (AG) up 101.87%, YTD

(USA) up 92.38% YTD

(EXN) up 49.27% YTD

http://cdn.ceo.ca/1f0i6cj-Silver%20Producers%202019%20YTD%20Chart.JPG

{kind=link}

At one point Santacruz was up 250% crushing the rest of the sector, and I doubt most investors were positioned before that if they only had a handful of stocks, but it allowed for a great trade in the summer surge to reallocate to companies that hadn’t moved as much like Impact Silver.

So there are pros and cons to a concentrated position versus a basket approach but both are viable strategies, and address different risk appetites or different investor preferences. Cheers!

It seems odd to me that you talk about actively managing your “ETF” yet you still find value in YTD performance. I can’t think of a less useful metric, especially in this highly cyclical and very volatile sector.

IPT has been lagging somewhat and I am not surprised since the senior gold producers have been leading the sector since 9/2018. That is changing now and I WILL be surprised if IPT continues to move without its usual gusto. Kootenay and Brixton both did quite well for me as did JAG considering my average price for each.

Then there’s the million+ shares of IPT I picked up in late 2017 that doubled in the first quarter of 2018 while its peers did very little. These discrepancies are the norm for this and every sector which is a good reason not to own just one stock (lol).

As for Santa Cruz, congrats to those who picked it up cheap; I didn’t. Frankly, I have never followed it and after “crushing” the competition to the DOWNside for the last few years, I wondered what might be wrong with it. My mistake but I can’t say I’m jealous of someone with one-fiftieth of their portfolio in it. That’s a joke. I’d be happy for anyone with 100% in it at 4.5 cents (Cdn).

IPT is up 35% vs FR in the last few weeks and is set to continue to outperform just like it did in 2016. When it counted on January 10, 2016…

https://stockcharts.com/h-sc/ui?s=IPT.V%3AFR.TO&p=D&st=2015-11-20&en=2017-01-19&id=p94732555127&a=450748116

Timing is everything in this sector. Stories and YTD data doesn’t mean much.

Hilarious Matthew. Most funds, analysts, and investors have looked at YTD returns, so try selling the whole investing industry that it’s a useless metric. Almost every trading platform or financial site online will list YTD metrics as quick way to look at how a company is trending.

Yes, I like to actively manage my account so that when stocks like Silvercorp, Santacruz Silver, and First Majestic outperform companies like Impact or Kootenay, that I can trim back some of the winners, and add more to the laggards that haven’t moved as much.

You’ve mentioned so many times that (IPT) is the bellweather for the Silver miners, and for a few years it was, but then how do you explain so many other Silver stocks moving first and 2-3 times as much? Either it is the bellweather setting the trends, or it is just another Silver stock with its own unique fundamentals and technical set up.

The facts are many other Silver stocks outperformed IPT in 2019 during the next leg of the Bull market, and while I own and like Impact, I was sure glad I had a basket of other Silver producers and developers that far out-performed it this year.

As for Santacruz, I had posted the news “stories” of them divesting their old projects to First Majestic, Marlin, and Americas Gold & Silver, of them paying down their debt substantially, of them improving their Zinc circuit, and optimizing their 2 producing mines and cost profile, so it was not a surprise at all to anyone following the news flow, and not just relying on charts. I had one of my largest positions in Santacruz coming into 2019 after adding more in tax loss 2018, and trimmed it back some in August and discussed these trades often over at ceo.ca.

I’m happy to have outsized gains in any stock, and don’t have the arbitrary prerequisite of needing to have 100% in it at the low. I’m happy for any investor when they make a nice gain, but I guess that is too funny for words.

Again, by owning more stocks, I can rebalance the portfolio on big rips in breakout stocks like that, and put the gains into the companies that didn’t move quite as much. It may not be a strategy everyone likes, but neither is your approach.

To each their own.

Ex didn’t mean to create any controversy or hard feelings between you and Matthew. Personally I manage two fairly small accounts combined probably have 30 stocks, but some are in energy and industrial metals. The bulk of my dough my wife and I have invested with a third party money manager and is very widely diversified. So I do this as a hobby, but certainly want to make money while taking measured risks. Out of curiosity do you have a concentration limit or a way you think about position size for each holding. I appreciate the dialog. I have learned from both you and Matthew.

Thanks Charles and no worries. I also have most of my funds tied up in a bunch of mutual funds with 3rd party money managers, but enjoy actively managing funds in my secondary trading account and it sounds like a similar spread between mostly PMs, but some Base Metals and some Energy stocks.

As for position size, I am more heavily weighted in the less sexy Mid-tiers (2-3% positions) to smaller producers, but will pepper in smaller (1-2%) in advanced developers or explorers. If a stock really starts to run I may initially sell 1/4-1/3 of the position if it technically looks oversold, but will keep a core position. If it keeps rising in multibagger scenario, I don’t want that core position to be much more than 10% of the value in the overall portfolio, so I’ll trim a high flyer back to keep is less that 10%, but eventually will unload much of that position in the final peak of the next intermediate cycle, and take it back down to a 2-3% position in the portfolio and reallocate the winnings into shoring up other positions that haven’t moved, or into starting new positions.

There are a number of attractive stories in each sector at any given time, but we can’t own all of them. I generally have as many Silver stocks as I want in my portfolio with 8 Producers, 6 Developers, and 4 Explorers. If a company gets taken over or if I liquidate the position, then I’ll refill one of those slots. For example, if a larger company bought out Discovery Metals, then I’d replace it with another Silver Developer, and so on.

On the Gold companies I have more Producers and Developers than I really want longer term, so as they rise in value or get acquired, then I intend to divest some of those positions and fortify the core group more, until in a few years I liquidate a number of the positions completely.

I’m underweight in the Base Metals and Energy stocks compared to where I’d like them longer term, so as some positions grow to be 4-7% valuations on big fundamental/technical moves, I’ll likely pair those back down to 2-3% positions and move the winnings over into new positions in those sectors over the next year or two.

That’s my basic approach, but there are certain fundamental cases where I’ll just let the company grow more than average, like what happened with K92 mining the last 2 years or Silvercorp in 2019, but eventually I trimmed both companies back (1 for jurisdiction concerns and the other because it was getting larger in my portfolio than I wanted). I still expect both companies to continue growing in value so I’ll watch them in relation to the rest of the portfolio and if they grow too large faster than the rest, then I’ll pair them back again. It is like financially pruning the tree from time to time.

I hope that this offers one perspective on position sizing and some ideas on rebalancing a portfolio. It would be the same concept if I only had 10 or 20 stocks, but hey that’s just one way of investing. There are investors with only a few stocks and some that have hundreds. I wouldn’t want to do the work to manage 100-200 positions at once, but some do it. Conversely, I watched too many people be burnt only carrying 3-7 positions and not having the right timing, understanding, or just bad luck where a company experiences unforeseen problems and a good things goes bad.

Every investor needs to decide for themselves how much risk they are willing to take and how concentrated of a bet they want to make. I could see taking on a larger stake if you had ownership in a company (like some CEOs do) where they can actually shape the outcome and do work to help their investment.

As retail investors the ability to shape the destiny of a company is not there, nor is the control of investing in one’s own business or real estate, so I stay diversified. My longer term plan is to make gains in paper assets and my trading account, and store them longer term in real estate. I’ll likely keep things more concentrated in real estate, because I’ll have more control of many of the variables, but over time I want that portfolio diversified between rentals, lease options, some flips, land, and tax liens.

In a previous life I helped families with investing goals, planning for retirement, and allocating investments based on their risk profiles. There were all types of investors, with all kinds of unique personal ticks and preferences, and I’ve seen it all. There were some with concentrated bets all in one kind of asset classes and some that so many irons in the fire and were so diversified it was a lot to take it all in. For most people and in most portfolios I reviewed, the ones that were concentrated either had stellar years or terrible disaster years, and the diversified ones were a slow and steady wins the race scenario like the tortoise and the hare story. I’m more conservative by nature so I like the latter strategy of less risk and steady gains over time, and that is likely why a manage a larger basket of stocks personally.

Ever Upward!

Ex, I rest my case about your technical acumen. YTD performance completely ignores cycles/nature. Traders and active managers capture individual trends which have nothing to do with YTD nonsense and vary from one stock to another in their timing.

Do you attempt to buy lows or do you consult your calendar?

The metric is completely useless for sizing up any miner.

The financial industry that you’re so impressed with also loves to fill ads with past performance figures. Do YOU like to buy last year’s overbought winners along with the rest of the bag-holding sheep? Most people own lots of SPY and zero GDX right now due to such brilliant logic.

Matthew – It is the end of 2019 and Year To Date performance metrics are incredibly relevant to see how stocks did this year for the overall trend. There are tons of investors that are not short duration traders, that are buy and hold value investors that may buy at the end or beginning of the year and hold for the whole year, so the YTD figures are very appropriate.

Not everything I post about is for traders, and from what I gather from most of the comments here and on other forums, most investors are not day traders or swinger traders, but rather value investors that look very much at how asset classes or certain stocks did YTD.

I’m incredibly aware of how to use charts in my individual trading to look for opportune times of entries and exits, and am fully aware that during the year there were highs in lows in every stock and that they should all be looked at individually if a trader is looking for buying into weakness or some that like to buy with the chart indicators show a powerful trend in motion.

That has nothing at all to do with looking back at year-end to see how a sector did for value investors that bought at this time of year and held for the duration.

Some of the stocks I positioned in or added to were at the end of 2018 right after the holidays, and I held some those positions all year so the metrics are quite relevant.

Your error in judgement is assuming everyone trades the same way you do, and your need to be an ass and keep attacking everything I post and make personal attacks is getting old, is not constructive, and you are not offering any value when you post garbage like that. Give it rest and get over it that IPT underperformed most of the sector on the YTD figures.

Just go post some charts with Andrews Pitchforks on it…. you’ll feel better 😉

Thanks Ex. I agree that portfolio management is a personal thing, but learning from others is always helpful and insightful. I have a system that seems to be working and it is similar to yours although I only have about 30 names spread between two accounts (one taxable and one IRA). 30 is more than I want, but I have added some new names recently. I will probably get rid of some under performers at the next intermediate top to get down to about 20-25. Good luck with your trading.

Thanks Charles. It sounds like you have a good process in place between the two accounts, and yes, I believe we can all learn from one another, as there are many paths up the mountain.

You have a good eye for some of the better performing stocks in the sector, so keep up the great work, and if you have any companies you want to review or find anything you think we should all take a look at, please share your insights. I always appreciate your comments, good questions, and desire to learn and share ideas. It is greatly appreciated.

Good luck to you in your investing in 2020 and may you have a prosperous year!

Your use of YTD is foolish and never made anyone a single cent. It would be just as useless if IPT were doing twice as well as your favorites.

I’m not going to bother with the rest of your claims at 5:37 but you really ought to see someone about your digital diarrhea. You must be in marketing.

Btw, 9:30am To Date, bellwether IPT is stomping your picks flat and my portfolio is up 6 times as much as SILJ. 😉

Again, more hubris and attitude, and missed the point completely. Get over yourself.

BTW – (IPT) IS one of my positions, and happens to be one of my 3 picks for 2020 in the stock picking contest over at ceo, because it technically looks much more constructive that it did in 2019. If you are so all-knowing, then why didn’t you invest in the companies that outperformed Impact in 2019 and then rotate those winnings into IPT on the latest dip?

Just curious since you are so wise, how you missed the easier gains in 2019 and bet on the horses the underperformed. All the pitchforks in the world won’t change that you missed the better performers in 2019. Cheers!

You’re a words guy yet you missed that I was referring to your picks in your YTD example above.

Yes, I have an attitude when it comes to complete BS and it’s some rich BS that you’re asking me about missed gains when you do A LOT of riding positions all the way down. I’d be having a great year even if I didn’t trade in and out (based on trends, not calendars 😉).

As for your comments about missing easy gains, and pitchforks, you just put your ignorance up in neon lights.

Btw, MTD (month to date), IPT is at the top of your little stack and KTN and BBB have beat 3 out of 4. And yes, “anything-to-date” is still worthless just like a bunch of stories.

Charts rule if you know what to do with them but you’re clearly not wired for them.

Your insults and put downs are what is neon lights and it’s not a good look Matthew.

I have all 3 of those positions IPT, KTN, and BBB and fine with their moves lately, but they weren’t even close to the best performing stocks in the Silver sector this year.

I’d disagree and say that month-to-date data IS VALUABLE and shows some of your picks are finally getting traction. I’ve owned them waiting to see a little more life out of all 3 so I’m all smiles despite your cockiness and nastiness.

Sincerely hoping your picks do better in 2020. (I’ve been trading IPT, KTN, and BBB since 2016 and using technical analysis to do so, despite your nonsensical wiring comments – which is just an asshole comment).

Your insults and put downs are what is neon lights and it’s not a good look Matthew.

I have all 3 of those positions IPT, KTN, and BBB and fine with their moves lately, but they weren’t even close to the best performing stocks in the Silver sector this year.

I’d disagree and say that month-to-date data IS VALUABLE and shows some of your picks are finally getting traction. I’ve owned them waiting to see a little more life out of all 3 so I’m all smiles despite your cockiness and nastiness.

Sincerely hoping your picks do better in 2020. (I’ve been trading IPT, KTN, and BBB since 2016 and using technical analysis to do so, despite your nonsensical wiring comments – which is just an a-hole comment).

Being an a–h— doesn’t make me wrong. I think I’ll go play with my pitchforks now.

Yeah it does make you wrong, and I don’t need to defend my knowledge or usage of TA to you, don’t need your approval, or your biases that blind you.

I value your charts, and would like to think we could have a conversation where you weren’t so insulting, and could admit there are other perspectives than your own, but it looks like you are incapable and are just digging in to your own personal “I’m right” party.

Good luck partying by yourself and your pitchforks, and Happy New Year amigo.

To each their own. I would much rather build my own ETF of Silver miners, and actively manage the weightings and positions in it, than hold SILJ where it is often skewed to much larger and clunkier companies, and doesn’t even feature some of the smaller Jrs. My basket of stocks continually outperforms GDXJ or SILJ, and doesn’t have as many Major or Mid-tiers holding it back.

Yes it takes research and work to manage a portfolio, but is very doable for 1-2 hrs per day. If people don’t want to to spend the time, then yes, they can go with the ETF and make lessor returns.

I’ve also watched many investors blow up their accounts going all in on just a handful of names, particularly in the explorers, and not properly account for risk or diversify into other subsectors or commodities. We see it all the time over at ceo.ca or stockhouse or hotcopper where investors bang on their chests about their few pet stocks and when they sell down by 50-99% they get their clocks cleaned, (even though they were so sure they had the best horses in their stable).

That is why many of the resource investors have left over the years never to come back, because they blew their wad on a handful of stocks and lost big. Very few investors do well on all or most of their positions, and betting the farm on 5-10 Jr miners is like juggling dynamite.

Some of the reasons for investors devestating their accounts were on them for not understanding the risks they were taking going all in on just a few momentum stocks, and some of that is compounded by the huge fail rate among Jr miners, even including developers and producers.

I don’t have delusions or expectations that all my positions will be 10-baggers, but those kind of gains sure help pull the overall gains of the portfolio higher and more than cancel out any losses on other positions. As long as I’m outperforming the general equities and outpeforming sector ETFs with better returns, then I’m a happy investor and my objectives have been met.

Wishing everyone success in 2020 regardless of their investing strategy or personal preferences.

Concentrated positions are definitely not for those who don’t know what they’re doing. And in a sector-wide downturn, diversification doesn’t help much. They all fall apart.

Holding 5 or 10 positions is juggling dynamite if you don’t know what you’re doing.

I don’t find it difficult to choose relatively safe plays even though I often buy riskier cheapies like Scorpio Gold. Position allocation size is one key way to manage risk and it works well.

I’d wager that the vast majority of “ETF buliders” will rarely outperform SILJ. It nearly quintupled in 2016 while a lot of juniors (like Mandalay) barely doubled or tripled.

I have to agree with Warren Buffett:

“Diversification is protection against ignorance. It makes little sense if you know what you are doing.”

“Wide diversification is only required when investors do not understand what they are doing.”

I would wager to guess that the vast majority of investors don’t know what they are doing, and like you mentioned earlier this week “the great majority loses money.”

The advantage of a diversified basket, is that one hasn’t bet the farm on just a handful of very high risk Jr mining stocks, and by taking smaller positions, can wait out down turns, or wait for a few of the high flyers to wash out malinvestments.

It doesn’t take many 10 baggers to wash out several 30-50% losses in positions that were of similar size. At that point the gains can be reaped, and reinvested in some of the positions that sold off if there is still fundamental belief in those companies, or put into new positions. Rebalancing the portfolio is tough if there are only a handful of stocks and most are done, but much easier in a basket of stocks where it is likely on any given day/week/month some stocks are up nicely.

Let’s be real, most resource investors do not know what they are doing and having 5-10 stocks is definitely juggling dynamite, and far riskier than many generalist investors with Mutual Funds full of 30-100 stocks each are willing to take.

Different strokes for different folks,

Berkshire Hathaway, Buffet’s company, has absorbed about 70-80 companies, so ironically based on his statement it is pretty well diversified.

The vast majority of retirement accounts on the planet are in a base of mutual funds or ETFS (each with 30-100 stocks in them), so most prudent money managers place families funds into large baskets of stocks for diversification.

Most investors & funds, who lose or underperform the general indexes, would be ill-advised to only invest in 5-10 stocks, unless, like Berkshire Hathaway, it has already diversified itself across dozens of sectors and with several companies within each sector.

And that is why my answer to Charles is specifically about MY preferences and not a recommendation to the average investor or anyone else.

If we’re being real as you suggest we should, I’d be much worse off had I taken your approach over the years instead of mine. That’s just a fact. Like I said above, there’s simply no reason to own a lot of these things. Many have terrible prospects technically even if their “stories” are sound.

Eric Sprott, a Billionaire through resource investing, has positioned in about 40 stocks, and something tells me he is going to do just fine as the bull market continues to unfold. 🙂

Don Durrett that runs Gold Stock Data has a Top 25 list, and I believe I remember him saying in a few interview that he holds around 40-50 resource stocks at any one time and he’s been around and successful for decades.

David Erfle mentioned holding around 20-24 stocks and he’s a solid investor and commentator in the space.

Brien Lundin, who runds the New Orlean investment conference holds about 60-80 stocks in his portfolio.

John Doody has had times where he held around 30 stocks in their GSA portfolio.

Again, the ETFs like GDX, GDXJ, SIL, or SILJ have between 40-50 stocks in them at any given time, only investors have internal fees charged for someone else to manage those, and they have no control of removing certain lager cap laggards, on controlling the weighting, or adding in many smaller Jrs that are microcap stocks too small to even include in their ETFS.

Many savvy investors manage their own ETFS. Again, they aren’t all going to be winners, but the big multibag gainers, more than wash out some losses, and it isn’t nearly so risky as putting all ones eggs in 5-10 stocks.

There are investors that private message me regularly at ceo.ca that talk about how they are down 60-90% from going all in on hot trending stocks that go parabolic and then head back down for a return trip (or worse). When they ask for advice, I recommend not taking such huge risks on just a few companies and spreading their bets over different sectors Gold, Silver, PGMs, Copper, Nickel, Zinc/Lead, etc… and different subsectors Producers, Developers, Explorers, Prospect Generators / Royalty companies. They often write me back later thanking me for perspectives on taking a more balanced approach to the resource sector. Sure this limits some of the big gains on a concentrated position (but those are far more rare than big losses on a concentrated position).

Re: “Eric Sprott, a Billionaire through resource investing, has positioned in about 40 stocks, and something tells me he is going to do just fine as the bull market continues to unfold”

—

Too funny for words, Ex. He’s a billionaire. Whatever a billionaire chooses to do, you should rest assured that his objectives are very different than yours. Sprott’s got sweet deals and warrants up the wazoo so he obviously is not into taking much risk. And why should he. He made it. For those who might want to quit their 9 to 5 at 28, 40 positions will get you there by 50!

Eric Sprott positioning in about 40 companies is to capture the upside in the coming bull market just like everyone else, and it doesn’t seem funny, but more like a winning strategy.

I went on to quickly list 4 more prominent full time investors like Don Durret, David Erfle, John Doody, and Brien Lundin that all have many more than 5-10 stocks and they’ve been doing this for a while, but I could go on – Doug Casey has about 80 resource stocks, John Kaiser has positions in dozens, as does Eric Coffin, and many more.

To act like most investors should only carve out concentrated positions in 5-10 stocks in such an incredibly risky sector would be more funny if it wasn’t so dangerous. It is interesting that when responding to Goldfingers post about us “all making some money together” you wanted to protect newbies, but advising most newbies, who likely don’t know what they are doing, to invest in concentrate positions is a very risky strategy, and the only ones around to promote that are the ones like yourself that are far better than average stock pickers and that won with this strategy. Unfortunately most folks chasing hot money into the miners lose big only betting on a few hot picks, and without diversifying, blow up their accounts in a few ill-timed bets or betting on the wrong companies, and they leave never to return. It was the same with Biotech, or Pot stocks, where people went all in on a hot tip in a concentrated bet and lost bigly.

The biggest advantage to concentrated bets is IF one is correct and holds on to a winner, the gains can be huge, but as we’ve discussed, most investors don’t pick winners and lose big. Again, I’d rather trade some of the upside potential, to spread the risk across a larger basket and then actively manage the winners/losers, weighting, and position sizes accordingly. It may limit growth, but it also limits downside losses, and over time a solid portfolio can outperform the general indexes and sector ETFs. If people can’t beat the indexes and ETFs, then I agree they shouldn’t be managing their own money, and should just buy the ETFs and save themselves the time doing research.

Different strokes for different folks.

Re: “To act like most investors should only carve out concentrated positions in 5-10 stocks in such an incredibly risky sector would be more funny if it wasn’t so dangerous. Etc, etc”

— — —

Ok, now I’m wondering if you’re related to Birdman. I can see why charts aren’t very useful to you if that’s how rational you are. I was asked a question about what I do. That’s all. My honest answer was just that and NOT a recommendation.

Furthermore, bringing up a bunch of newsletter writers and promoters is just silliness.

Doug Casey thought the the bond bull was ending over ten years ago, for crying out loud.

No wonder he doesn’t manage his own money. I was a subscriber long ago and his picks rarely passed a technical screening because he is not wired that way. Like you he is all about stories so he MUST diversify. But I digress. Successful newsletter writers probably should hold all the stocks that they cover for many reasons. They too are likely to have a different risk profile considering their average age, net worth, and income from subscriptions.

Good luck. I hope you don’t buy the top like you did in 2011 (your words).

This is going nowhere Matthew as you are just being insulting to me and other and not even considering the merits at the heart of portfolio balancing, but trying to cherry pick a few areas to be ugly.

Please show me where I said I bought the top in 2011, as those were not my words, and that is for more reminiscent of Birdman – putting words in others mouths, and is a low for you.

I’ve stated dozens of times on here that I used to buy and sell physical Silver bullion, and bought most of it from $10-$20 in 2008 & 2009, and sold most of it 2011 in the mid 30’s. (hardly buying at the top in 2011, but why concern yourself with the facts) 😉

As for the miners, I started buying Gold & Silver, Base Metals, and Uranium miners in 2010, and had a nice run higher in all of them (once again, not buying the top in 2011). I did hang onto some positions past the peak in 2011 and into 2012 before selling some of them with losses, but I’d had 2 years of gains in 2010, and 2011. It was 2012 that I decided to get more into technical analysis, because prior to that I was not using it to analyse companies, and wanted to learn how to swing-trade shorter duration rallies in the bear market.

In no way was any of that buying at the 2011 top, so you must have me confused with someone else like Spanky who did admit buying at the top in 2016. I was the one recommending buying in late December 2015 and early Jan-Feb 2016, and mentioning I was trimming things back in July and August 2016.

How you can insinuate I was buying at the tops is as puzzling as it is disappointing.

I actually learned a lot from folks here at the KER like you, Doc, Gabrial, Rick Ackerman, Gary Savage, Avi Gilburt, as well as many other folks like Gary Wagner, Morris Hubbart, Claude Maund, Peter Hug, Jim WycKoff, Sid Norris, Christopher Aaron, Ira Epstein, the many contributors at Gold Tent, Goldfinger, Ty, Northstar, and many other contributors on different forums. I believe I’ve shared enough over the years for you to realize I understand, use, and appreciate technical analysis, so I’m really not sure what that last post was about.

I’m done debating this topic dude, because it’s clear you don’t value the points I’m sharing, and just want to argue. Good night!

Ex, you said that I “act like most investors SHOULD only carve out concentrated positions in 5-10 stocks…”

THAT was a BIRDMAN move on YOUR part. I answered a question about what I do and did not “act” like anyone SHOULD do anything. Absolutely no one SHOULD do anything that I do. I constantly sing the praises of stocks that I don’t even own (like EGO and CDE in late spring or early summer when they were cheap). You, on the other hand, have something good to say about every single miner in existence regardless of the chart. Maybe that’s because you own them all.

As for your words, that was many years ago and maybe you were talking about buying silver wrong. Whatever it was, you made it sound like a big mistake. Whatever. I’ll continue to answer questions without regard for your approval.

Rob McEwen, btw, has about 20% of his net worth in one miner. Yes, different strokes for different folks and appeals to authority are always dumb.

As for your use of the charts or “technicals,” you’ve been here long enough for me to know that you don’t really know.

Thanks for the extra insults, putting words in my mouth, and discounting down my perspectives. You’re really offering up the value for the KER site here tonight.

It’s beneath you man.

Then I guess you can tell that I didn’t appreciate you claiming that I was saying what others “should” do. No advice was given. Got it?

No I don’t get it or any of the rants you are going on for most of this thread.

You made the point earlier in the week about making sure newbies know that most people lose money when my post was not geared for newbies, but you had to grandstand on that point.

Up above Charles had specifically mentioned my name regarding a managed portfolio approach, and proceeded to diss on that whole approach, and made several definitive statements as if they were facts, when they are just your opinions. Since I was specifically mentioned and disagreed with some of your assertions, I posted a reply reviewing the advantages of a balanced portfolio approach over the FAR riskier small handful of mining stocks approach, but acknowledged that if one was correct on their bets sure, but we had already covered that most investors don’t know what they are doing and fail in their bets all the time in the resource sector.

I pointed out using the Silver producers how a managed portfolio of companies like Silvercorp, Santacruz, First Majestic, Americas Gold & Silver, Excellon, and Impact outperformed just picking a stock like Impact for one’s Silver producer position, and you threw a tantrum over YTD numbers as being irrelevant. Try selling that to all the buy and hold value investors that buy during tax loss and hold for the year.

Instead of acknowledging there are pros and cons to both approaches, or the risks associated with only having a handful of stocks in one of the most volatile sectors with the highest fail rates in companies, you acted like if you know what you are doing you’ll be fine. (which is incredibly pompous and arrogant). More investors blow up their accounts going all in on 5-7 stocks, than a more diversified portfolio where it is unlikely ever stock will crater (like so many mining stocks do). I was simply sharing a different perspective and then you got all pissy.

Then you implied it would be better just to buy the ETF if your going to hold a basket of stocks, which is poppycock. That ignores the ability of investors to select better Jr companies with more torque that can not be included in ETFs due to their smaller market caps or less liquidiity, or that by utilizing TA or following fundament news that investors can manage their positions different than in an ETF and outperform them.

You’ve been repeatedly combative and insulting to me in your replies, and have been ugly and snide in your responses where it was not required to make your points, and it is sad, because normally you posts are more constructive and actually have value.

Peace out Matthew.

For clarity Charles was fine in asking his question and I didn’t want to imply in that comment above that he dissed on it, that was all you Matthew.

It’s fine to disagree, but the way you got so snarky and insulting as if you had the only approach that worked was way over the top and out of line.

My silver positions are doing very well-SVM, WPM, FR(AG) and EDR. I think it is due to the same reason as early 2000s. The good silver miners are so few and the PE became crazy. All the marginal producers are cutting or closing. It will result in lack of supply too. The silver production has been declining since 2016. All of the over supply due to last price spike is gone. Silver must rise or we have no silver to feed the industry. IMHO.

I hope someone confirm my observation. I may be wrong.

Dragonite – great points, and yes, there was just Jeff Clark article out talking about both the declining Silver grades across the industry, and shrinking size of most new deposits being found, and his conclusion was a rise to the Silver price over the next few years.

You are spot on with SVM Silvercorp as it was the best performing Silver Producer of 2019 up over 160% year to date (although at one point Santacruz was up 250% in the summer as the to performer). Yes First Majestic (AG) has also been solid up about 102% on the year (more than peers like Coeur up 78% YTD, Pan American up 53% YTD, or Hochschild up only 10% YTD).

Hopefully investors that know what they are doing had nice positions in Silvercorp, Santacruz, and First Majestic this year. 😉

Check out this 2019 Silver Producers Year-To-Date returns Chart:

http://cdn.ceo.ca/1f0i6cj-Silver%20Producers%202019%20YTD%20Chart.JPG

Excelsior, I guess your points will ensure that the silver price must rise significantly to allow more production. Silver miners are desperately waiting for the chance to go low grade. They are exhausting their high grade mines and it may leave them with nothing to mine. This at least applies to the pure or near pure silver producers. If silver just rise a bit, e.g. 50% , the production will drop because they will produce on lower grade mines. This will not work so the price has to go much much higher like after 2003. Since people have lost their shirt for the last two times and they will sit tight for much longer too.

Silver Mine Grades are Plummeting—What Does it Mean for Your Holdings?

Jeff Clark, Senior Analyst, Dec 16, 2019

“Silver mines aren’t pulling the same amount of metal out of the ground as they used to, which means less and less silver is coming to market.”

“new supply from silver mining is locked into a structural decline.”

“Structural,” meaning there are barriers and impediments embedded into the silver mining industry itself that cannot be easily or quickly changed.”

“They can’t just flip a switch and reverse years of problems.”

“The average grade from the 12 largest silver projects in the world has declined a whopping 36% in just one decade!”

“This is one big reason why new supply of silver has rolled over and begun a global decline. If you have less metal to dig up, less metal goes to the market.”

https://goldsilver.com/blog/silver-mine-grades-are-plummetingwhat-does-it-mean-for-your-holdings/

The week that just ended was a big deal technically for the sector and for sector bellwether Barrick Gold. Now we need confirming action: more gains and hopefully swelling volume.

https://stockcharts.com/h-sc/ui?s=GOLD&p=W&yr=4&mn=11&dy=0&id=p59649698370&a=666388372

GDX version of the above chart:

https://stockcharts.com/h-sc/ui?s=GDX&p=W&yr=4&mn=11&dy=0&id=p36900340854&a=709864450

Matthew, I like Newmount more. I had Goldcorp shares which I was in a losing position. Newmount acquired GoldCorp and I double down on newmount shares. Now I turned a 30% loss to 20% gain.

That’s great, Dragonite. I see that NEM just put in its best weekly close in 7 years.

https://stockcharts.com/h-sc/ui?s=NEM&p=W&yr=7&mn=7&dy=0&id=p62084675186

Even I am not very sure about how much, NEM also has good copper properties. Copper should do well in the next few years too I believe.

I have not been a buyer but the copper stocks already look promising…

https://stockcharts.com/h-sc/ui?s=COPX&p=W&yr=7&mn=7&dy=0&id=p74120403529

Copper is currently at what appears to be significant resistance:

https://stockcharts.com/h-sc/ui?s=%24COPPER&p=W&yr=4&mn=2&dy=0&id=p70623623357&a=613559752

Dragonite I own some Newmont at a loss and am considering selling for greener pastures that have more torque. Let me know if you ever plan to sell.

Sure, I will let everyone know. I usually hold a stock for many years. Newmount just turned the corner and rises again. I feel between the share appreciation and dividend, it should be good one to hold. It is also safe.

This year’s 180 degree turn ripped off Fed’s mask of pretending they have the control. Fed is now the emperor without cloths. We have only one direction left – inflation. We the precious metal investors are proven right after all. The next critical point is the destruction of the world reserve currency. Fed has no choice but to react at that point. It might be a few years away. We can stay in PM during this period.

Energy is my heavy position next to metals, I believe it will rise with inflation and supply shortage due to the completely lack of exploration and the death of expensive shale oil.

Nice to see you posting here again Dragonite. Are you still looking at Uranium stocks as part of your energy mix for 2020? If so, which ones are you liking and why?

Excelsior,

I hope that I can post more here. I haven’t sold one share of Uranium stocks. I am still holding and adding more. I actually bought DML before Christmas. I still believe that Uranium is coming back. My biggest holdings are CCO, DML, UEX,EFR and URE. All TSX stocks. China starts to add 8 nuclear reactors a year till 2030. These ones are massive. So I think Uranium can at least return to the price before Fukushima regardless Japanese reactors start or not. Japan is buying expensive natural gas to replace nuclear energy. I feel they have to compete with China, otherwise China will eat its lunch as it has been in the last 20 years. Japan is losing the economic battle badly. Industry centre has been shifting to China. China is doing so well and its manufacturing is matching rest of the world. Japan can not afford losing the war since the two countries have been threatening each other and now Japan is fading away.

BTW, my precious metals position has been doing very well for the last two years and energy is turning the corner too.

How about your uranium position and viewpoint?

Great picks there in the Uranium sector, and I hold profitable low cost-basis positions in many of the same stocks (UUUU/EFR), (URG/URE), and have considered (DNN/DML). I also hold (UEC) as a solid US-based insitu devloper, (NXE) as the premier and best advanced explore/developer in the Athabasca basin, and (AEC) a small US-based developer that has picked up most of Uranium One’s controversial US assets that were sold a few years back. AEC is my only underwater Uranium position at this point, but it is an optionality play on higher prices, so this is to be expected.

Overall I’ve done well trading the rest of the Uranium stocks in the Q1 2017 surge, the Q1 2018 surge, and did a few good swing trades around the Section 232 news, but wished I had taken more off the table before the outcome new broke that this wasnt the direction the Trump administration was going, and instead they implemented the Nuclear Working Group to debate the best path forward. It’ my position that US based companies will likely outperform most of the Canadian companies initially when that report comes out (likely in Feb/Mar). Then over time, as the contracting price goes higher the larger defined deposits like (NXE) (FCU) (DNN/DML) will move first.

I’ve also owned (UEX) and (AL) for Canadian explorers in the past and they stay pretty high torque, and I may position back in them down the road; but honestly the world doesn’t need as many Uranium explorers, but rather the industry needs higher prices, which will be a result of new longer-term off-take contracts.

All the industry market research is pointing to mid-2020 as the time when we’ll really see more longer term contracts signed by the utility companies, and thus a sudden move higher in the U price suddenly when that kicks off.

I believe the whole energy sector is primed to move higher (Oil, Nat Gas, Uranium, Lithium/Cobalt for batteries, and renewables like Solar/Wind/Hydro/Geothermal), however Uranium stocks are where I anticipate the largest returns in the medium to longer term (1-3 years).

It will take a bit longer for U sector wake up, but when it does, there is no bull market like a Uranium bull market, and the easiest gains are the initial moves up for those that positioned during the low sentiment.

Until then….. Cheers!

A Cheer for the Trump Uranium Plan

Beyond a stockpile, Trump must forge longer-term, taxpayer-friendly solutions

By Stephen Moore and Katie Tubb – – Sunday, December 15, 2019

“Our sources are telling us that President Trump is nearing a decision on how to revive the all-but-dormant American uranium industry. This proposed plan would create a reserve of domestically-mined uranium and stored in a “Federal Uranium Security Stockpile.” One option on the table is for the Department of Defense to purchase uranium through the 1950 Defense Production Act. ”

“The president concluded in July that: “The United States requires domestically produced uranium to satisfy DOD requirements for maintaining effective military capabilities,” including the Navy’s nuclear fleet.”

“Uranium is used for America’s nuclear arsenal as well as domestic nuclear power plants. The U.S. reactor fleet purchased about 40 million pounds of uranium last year. But American production of uranium has fallen steadily over the last 30 years and the nuclear power industry now gets 90 percent of its uranium through imports from nations like Canada, Australia, Russia and Kazakhstan. Only a few small American mines remain open.”

https://www.washingtontimes.com/news/2019/dec/15/a-cheer-for-the-trump-uranium-plan/

Country With World’s Largest Uranium Reserves Finally Considers Nuclear Energy

“Australia’s Parliament presented this week a report that outlines a series of measures to take into consideration if the country wants to move forward with the development of nuclear energy.”

“The report, which arose from a legislative committee’s inquiry into the matter, states that it is important for the island nation to consider the prospect of nuclear technology as part of its future energy mix and that to do so, relevant institutions would have to undertake a body of work to progress the understanding of nuclear technology in the Australian context.”

Group of Premiers Band Together To Develop Nuclear Reactor Technology

Ontario, Saskatchewan and New Brunswick will work together to research and build small modular reactors

Elise von Scheel · CBC News · Posted: Dec 01, 2019

“They will be working on the research, development and building of small modular reactors as a way to help their individual provinces reduce carbon emissions and move away from non-renewable energy sources like coal.”

This is like year 2002 when the silver miners significantly out-perform silver price. When the silver price declined, the companies like SVM, FR(AG) and WPM refused to move down, totally opposite to a few years ago. I believe that this scenario is very unique to the silver miners and it is the result of a massive reduction of quality silver miners. Funds which must invest in silver equity has no choice but to buy quality silver mines. It also comes with significant decline of silver supply in a long term. This phenomenon resulted in massive rise of silver price from 2003-2011. This time will not be any different. I expect a multi-year silver price explosion which will take silver price to three digit.

My best performing silver stock is SilverCorp. My lowest purchasing price is 65 Canadian cents. Now, it is 7.57 Canadian dollars. A gain of more than 10 times. Off course my average is around 1.5, but it is still 5 bagger for now.

Dragonite – Great post on the set up for the Silver Miners and limited pool of companies to pick. I agree that when the volume from more generalist investors does show up, that it needs to be funneled into small number of issues, which can create explosive gains.

In addition, I agree that SVM Silvercorp has had a stellar run since 2016, and it was your comments here on the KER that had me take another look at them near their lows. They have the best margins and lowest AISC in the Silver space hands down and became a sought after stock these last few years. 2019 was another great year for SVM.

Thanks again for your comments Dragonite and it is good to see you posting here at the KER again. May 2020 be a prosperous year for you in the markets and in life!

Thank you very much for your informative posts, especially in uranium stocks. I have sold around 40% of my SVM position and it still seems too large. It is a smaller miner nevertheless. My next target to sell is Cnd $9.9.

Happy investing in year 2020. As real asset investors , our good time is here.

Right back at you Dragonite, and I appreciate your input as always.

Yes, I recently trimmed back my Silvercorp (SVM) position after going on such a big run, and put more into some of the smaller Silver names that haven’t moved as much.

One of the companies I placed some of those gains was (DSV) Discovery Metals, after they took over the large but stranded asset from Levon resources. I like the Oxygen Capital Group run by Mark O’dea, and have invested with him over at Pure Gold (PGM) as well. (DSV) has really surged the last 2 weeks, so I’m looking forward to see where it goes in 2020. Yes, I agree that “our good time is here.”

2020 Is Just Around the Corner, and Shows Real Potential for Gold

December 27, 2019 – Gary Wagner #TechnicalAnalysis #Chart #VIDEO

https://thegoldforecast.com/video/2020-just-around-corner-and-shows-real-potential-gold

Silver Price 2020 Forecast – Surge then Retracement #VIDEO

iGold Advisor – Christopher Aaron •Dec 26, 2019 #TechnicalAnalysis #Chart

Gold: Massive Bull Flag Breakout

Morris Hubbartt – Super Force #PreciousMetals

Dec 27, 2019 #TechnicalAnalysis #Chart #VIDEO

TAKING THE HARD WAY OUT

By David Hay December 27, 2019

– Interest rates and inflation couldn’t be more different today than they were in the 1970s.

– One of the shocking surprises of the last decade is that despite ultra-low, zero, or, even, negative interest rates inflation has generally fallen rather than risen.

– Yet, when it comes to asset prices (US stocks, global bonds, and real estate), it has been a completely different story.

– One asset class that hasn’t risen as swiftly as others is gold and other precious metals.

– This underperformance has caused most American investors—be they retail or institutional—to give up on precious metals as an essential asset class.

– However, John Hathaway, who is considered to be the “Warren Buffett of the precious metals space,” is much more bullish given all of the macro-economic factors at play.

– In the short-term, John and top economist David Rosenberg anticipate we could have a recession in 2020.

– This becomes much more probable should financial markets correct hard next year after this year’s historic and euphoric rally.

– We are likely to see governments and central banks launch a coordinated blitz made up of additional trillions of pseudo-money and unbridled spending should a recession hit.

– With most US portfolios heavily skewed towards paper assets (i.e. stocks and bonds) and nearly devoid of hard assets (i.e. energy producers/transporters, gold miners, copper producers, and agriculture nutrient companies) the stage is set for a significant paradigm shift over the next decade.

A lot of insider buying at OM Osisko Metals. https://www.canadianinsider.com/node/7?menu_tickersearch=OM+%7C+Osisko+Metals

The USD is taking it on the chin in the overnight market action.

(BAR) Balmoral Resources: A Revival Story Of 2019

Dec. 27, 2019 – Peter Arendas

– Balmoral Resources is up 250% year-to-date and up 340% since the middle of July.

– Balmoral was able to benefit from Wallbridge Mining’s exploration success at Area 51 and from the Kirkland-Detour transaction.

https://seekingalpha.com/article/4314276-balmoral-resources-revival-story-of-2019

I wonder why he posted YTD percentages if nobody cares about them? (lol).

Obviously buy and hold investors do review them, especially at the end of the year looking back on the prior years performance.

YTD for your whole portfolio is far different than your use of it. It’s a scorecard for our combine activities throughout the year. It most certainly NOT a good way to compare the merits of mining stocks.

He was posting YTD in that particular stock (not his portfolio), and also posted the returns since July, so clearly he saw the value in the YTD figures (which you claim are worthless), and was using it the exact same I do or most investor do.

I agree that YTD numbers are scoreboard for 1 stock, a group of peer stocks within a sector, or even for comparing different sectors for a quick comparison as to how things stacked up in a particular year. Many utilize YTD figures to analyze the overall trend, and the closing year prices are all some care about, no different that using the daily closing price and not getting all jacked up about the intra-day swings. If you can’t grasp that there’s value in the annual performance of a stock a fund or group of stocks, then you’re lost.

I’m fully aware that during the year there are different highs/lows, and that is great information for active traders, and I enjoy those metrics as well, but those are apples and oranges to what I was posting about and you know it.

Most analysts, funds, and investors look a quarterly or annual performance metrics on a stock, ETF, Mutual fund, or in comparing sectors, and compare them to other like assets. That isn’t worthless data by any stretch; (except from your extreme vantage point and particular biases with how to chart for active trading).

If a company or sector ends the year up 160% or down 50% that is pretty significant for most people and definitely speaks to the overall trend. Many are stating that Gold is up about 18% YTD, and comparing it to other sectors, and that is no different that comparing companies YTD open to close metrics.

I’ve posted similar charts in the Gold, Silver, PGM, Copper, Uranium, and Lithium sectors for years here and on other sites, and most investors thanked me or appreciated the data. You’re the only one in a tizzy over it and calling it worthless, so don’t frigging use it then, but it has value, and I could care less about getting your validation.

If your memory is good, you know that I’ve always taken issue with YTD garbage. We’ve gone back and forth about it before (and having nothing to do with how my shares are doing).

It is a logical fallacy that it has merit because someone else uses it or finds the trivia interesting.

It’s ad-man hocus pocus for dummies that has never served me in ANY situation I’ve ever had in markets.

OK Matthew – Everyone else is crazy for using YTD data to compare sectors, funds, or stocks, and everyone should just follow your pitchforks and R2 philosophy and all be short duration traders in the Silver stocks that didn’t move as much most of the year.

If you knew what you were doing you would have used your amazing TA skills to pick better stocks for 2019. Wishing you a better 2020. Don’t go buying the tops now… Cheers!

But I’m the best out there, you said so yourself. Oh I get it, that was just more ad-man smarm. I prefer honesty but thanks all the same.

You are one of the best technicians out there, and suddenly one of the rudest and cockiest. That doesn’t mean you’re the best stock picker out there, but I like most of the stocks you pick.

Your discounting down of fundamental news is a weakness from my perspective. and I’m not an ad-man, but thanks again for more insults.

What is your problem Matthew. I’ve see you be a jerk to others regarding political views, but your recent hubris around trading and trolling is unbecoming.

If you don’t like my perspectives that’s fine, but don’t be a little chit about things.

Re: “jerk to others regarding political views”

I’ve not been nearly enough of a jerk regardless of the sheeple consensus. All collectivists are tyrants/criminals whether D or R and they’re easy to spot. F’em.

Thanks Cory & Big Al & all the KE Report contributors for all that you do, and another great weekend show. Cheers!