Santacruz Silver – Review of 2025 Financials and Operations and Ongoing 2026 Growth Initiatives

Arturo Préstamo Elizondo, Executive Chairman and CEO of Santacruz Silver Mining Ltd. (TSX.V:SCZ) (NASDAQ:SCZM) (FSE:1SZ), joins me to highlight their full-year 2025 financial and operational results across their portfolio of producing mines in Bolivia and Mexico. We also review a few of the key growth initiatives that the company has slated for 2026 across multiple projects.

FULL YEAR 2025 HIGHLIGHTS:

- Revenues of $326.4 million, a 15% increase year-over-year.

- Gross Profit of $109.4 million, a 91% increase year-over-year.

- Net Income of $42.2 million, a 74% decrease year-over-year1.

- Adjusted EBITDA of $104.6 million, a 99% increase year-over-year.

- Cash and Highly-Liquid Marketable Securities of $66.7 million, a 87% increase year-over-year2.

- Working Capital of $63.7 million, a 38% increase year-over-year.

- Average Realized Price per Ounce of Silver Equivalent Sold of $39.00, a 36% increase year-over-year.

- AISC per Silver Equivalent Ounce Sold of $30.81, a 18% increase year-over-year.

- Realized Margin per Silver Equivalent Ounce Sold of $8.19, a 209% increase year-over-year.

Last year was a milestone year for Santacruz, highlighted by the full debt repayment to Glencore, payment of taxes to Bolivia, and still ending the year with ~$70 million added to the treasury and materially strengthened balance sheet. Strong silver prices throughout the year and improving mine efficiencies contributed to a revenue increase of 15%, and the margin between the average realized price of silver and AISC improved by 209%.

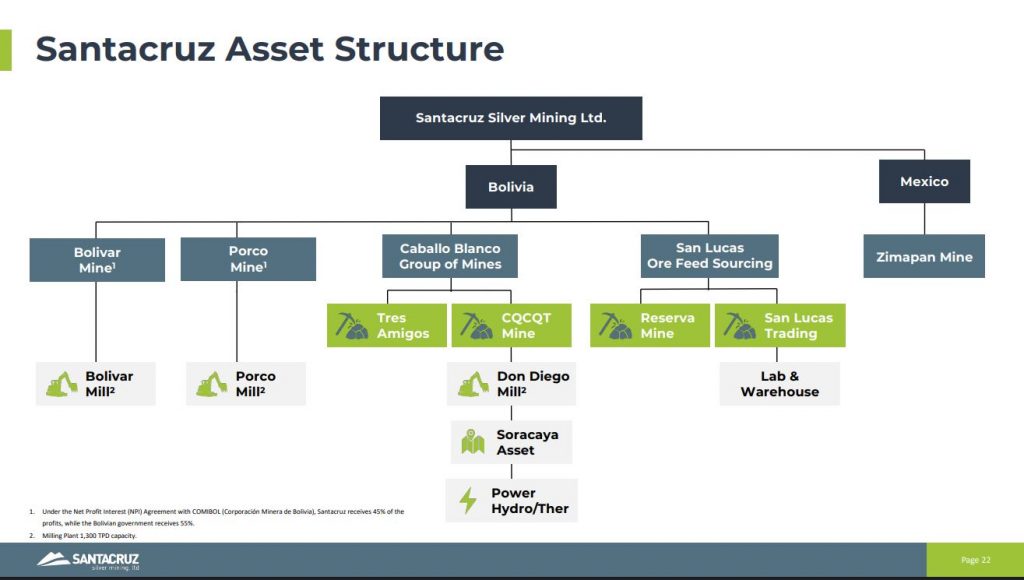

While total production was down 11% due to Bolivar’s May 2025 flooding event, the strength and diversification of their multi-asset operating portfolio helped offset the impact, with operations remaining cash-generative and profitable. The Company continues to expect Bolivar’s full recovery by Q4 2026, with the dewatering program progressing ahead of plan and driving consistent quarter-over-quarter improvements throughout the year. The Company is beginning to see the benefits of the recovery efforts at Bolivar, now accessing again the high silver-grade Pomabamba and Nané veins.

Next we moved over to the Caballo Blanco Group of mines, which is the lowest cost and thus highest efficiency of their operations. Colquechaquita and Tres Amigos are the 2 producing mines, but Arturo mentioned that the Company has now brought Esperanza Mine back into production during Q1, and that it should be a profitable smaller zinc-forward mine in this Caballo Blanco complex moving forward.

Next we shifted over to the high-margin San Lucas Group Lucas feed sourcing business (which now includes ore blended from the Reserva Mine, previously part of the Caballo Blanco complex). Arturo points out that since this is a “margin business” it will always be profitable, but that it will see higher costs in parallel with higher silver prices, and thus the higher amount needed to be paid to the small regional miners that bring in their ore to sell to San Lucas. The higher costs are not an efficiency issue, but rather reflective of moves up in the metals prices themselves.

Their Zimapán Mine in Mexico will be another area of growth for Santacruz Silver in 2026, after a substantial capital investment last year into plant equipment and improving mine efficiencies and metals recoveries. Additionally, the operations team had finally gained access to the high-grade 960 Level of the Zimpan Mine at the end of Q4, and so this will be a more significant contributing area of production starting in Q1 2026 and for several years to come.

The operations team is advancing their silver-dominant Soracaya mine towards development and near-term production. There is already a decline ramp into this project with initial stope access in 2 areas, and the plan once the permit is received is to get this mine into initial production by Q4 of 2026.

Wrapping up we discussed the potential for future accretive acquisitions in the Americas. The board and management team are open to a currently producing mine or development-stage underground mining assets, but only if the acquisition would be accretive for shareholders and if their team can unlock value in these acquired assets.

If you have any follow up questions for Arturo regarding Santacruz Silver, then please email those to me Shad@kereport.com.

- In full disclosure, Shad is a shareholder of Santacruz Silver at the time of this recording, and may choose to buy or sell shares at any time.

Click here to follow the latest news from Santacruz Silver

For more market commentary & interview summaries, subscribe to our Substacks:

The KE Report: https://kereport.substack.com/

Shad’s resource market commentary: https://excelsiorprosperity.substack.com/

Investment disclaimer: This content is for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any security. Investing in equities and commodities involves risk, including the possible loss of principal. Do your own research and consult a licensed financial advisor before making any investment decisions. Guests and hosts may own shares in companies mentioned, and companies profiled may be sponsors of the KE Report.

Leave a Reply