Sonoro Gold – Updated Resource and PEA, Expanded Land Concession, Commencement of 50,000m Drill Program, and Value Proposition For The Cerro Caliche Gold Project

John Darch, Chairman and Director, and Ken MacLeod, President and CEO of Sonoro Gold Corp. (TSXV: SGO | OTCQB: SMOFF | FRA: 23SP), both join me to review multiple milestones achieved and catalysts on tap transforming the value proposition for their flagship Cerro Caliche Gold Project, located in Sonoro State of Mexico.

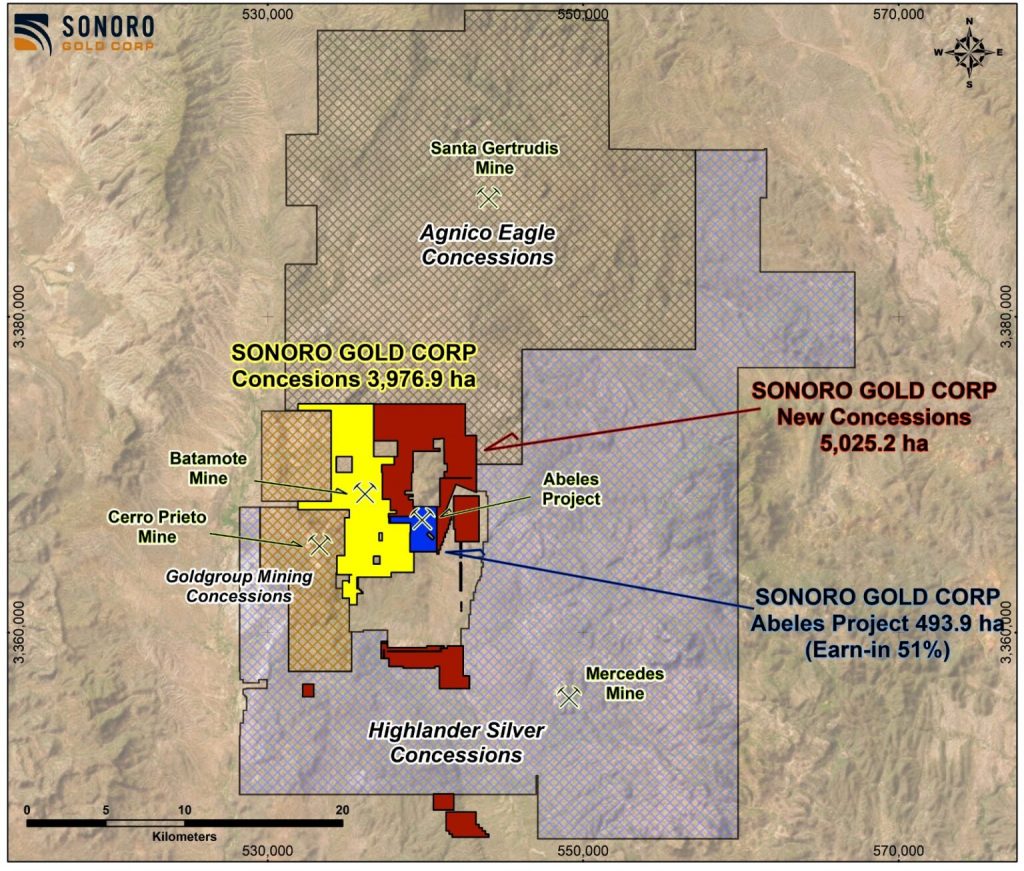

John and Ken both outline the transformation that Sonoro Gold has gone through over the last year, with the updated Mineral Resource Estimate, and resources and Preliminary Economic Assessment (PEA), the very large increase in their overall land package from 1,800 hectares to almost 9,000 hectares in 2 recent acquisition transactions. Thes increased land concessions build Cerro Caliche into a larger-scale gold mining project with multiple major mineralized zones stretching from the Agnico Eagle Santa Gertrudis deposit to the north down all the way to the Highlander Silver Mercedes Mine to the southeast.

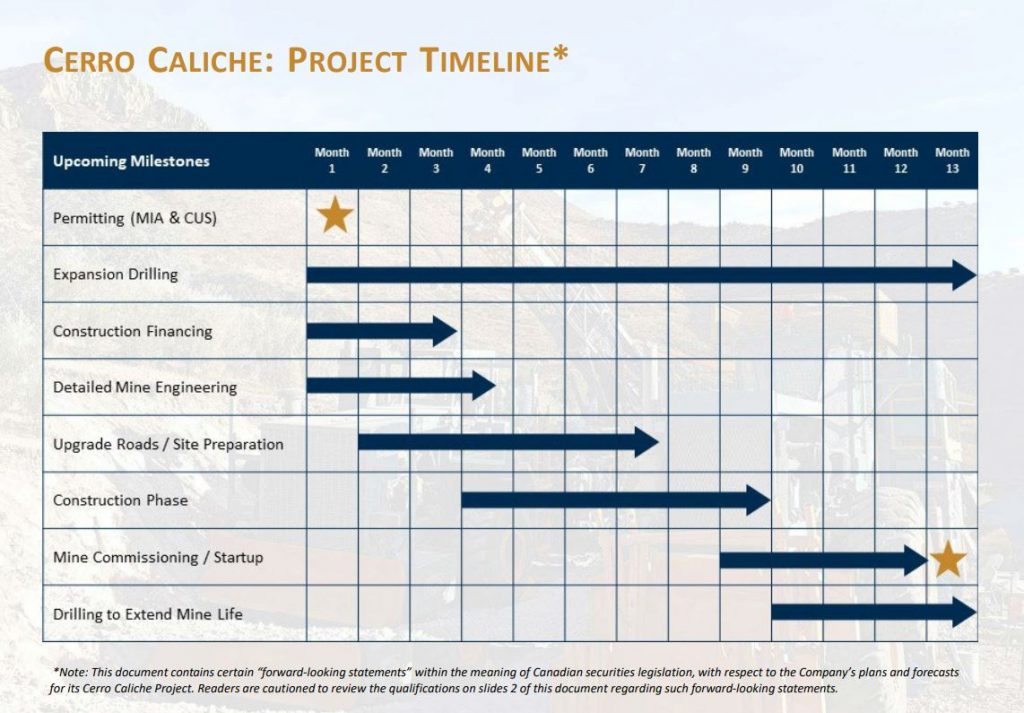

Next we got more details and initiatives around the commencement of the 50,000 meter drill program, which just got underway earlier this week. The focus will be on growing the resources, extending the mine-life, and exploring many of the areas across their new land concessions.

The company is now taking a hybrid approach, growing through exploration across their expanded project footprint, while remaining very constructive on the future development and production set to begin upon receipt of their final MIA environmental permit in Mexico.

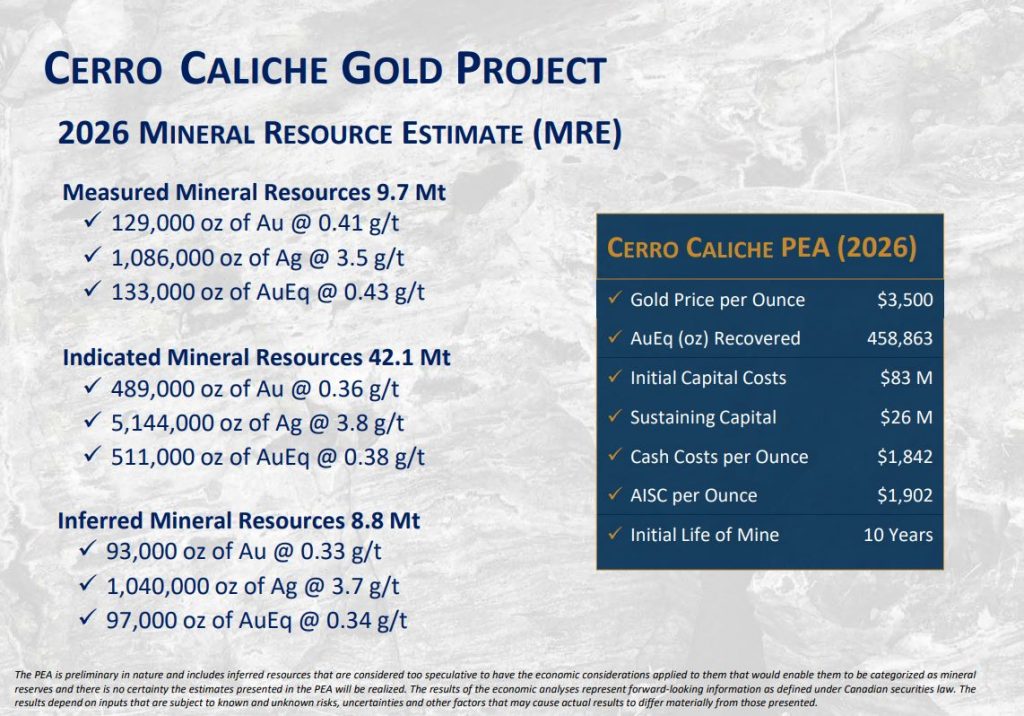

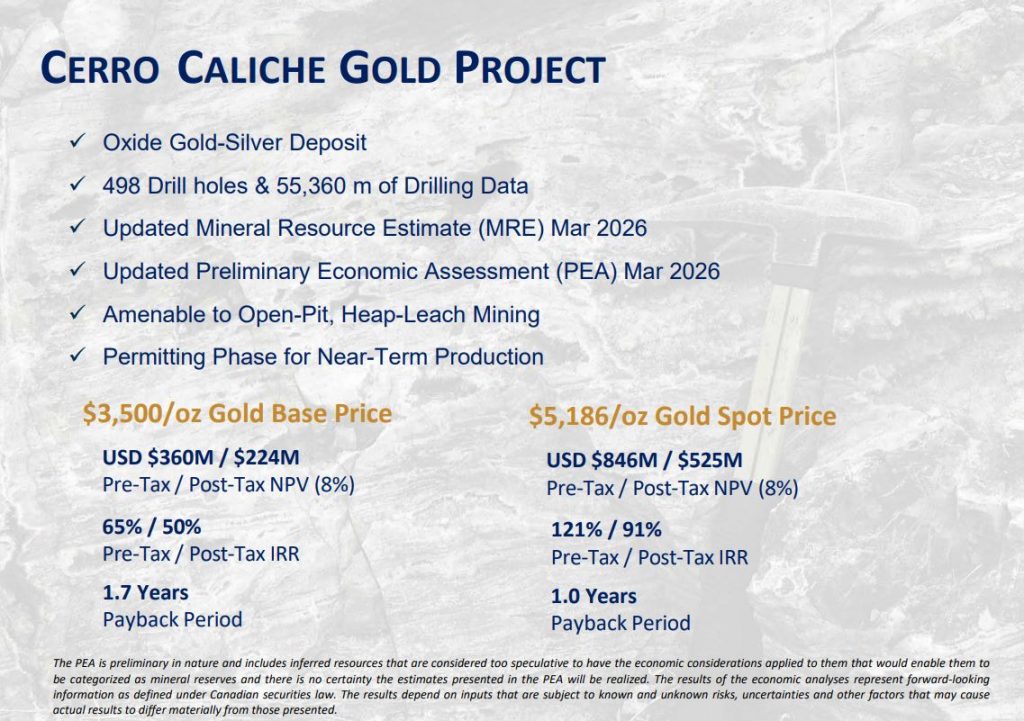

Updated PEA Highlights:

- Base Case Prices of $3,500/oz gold and $48/oz silver

- Pre-Tax net present value discounted at 8% (“NPV8”)of $360 million

- Pre-Tax Internal Rate of Return (“IRR”) of 65%

- After-Tax NPV8”of $224 million

- After-Tax IRR of 50%

- Spot Prices of $5,186/oz gold and $88/oz silver

- Pre-Tax NPV8of $846 million

- Pre-Tax IRR of 121%

- After-Tax NPV8”of $525 million

- After-Tax IRR of 91%

- Gold recovery of 72% and silver recovery of 27%

- 10-year LOM with 459 k ounces (“oz”) of gold equivalent (“AuEq”)

- LOM annual average production of 46 k oz AuEq at 0.38 g/t AuEq

- Initial CAPEX costs of $83 million, including $11 million in contingency

- Sustaining capital costs of $26 million

- AISC of $1,902/oz AuEq

- Payback period of 1.7 years

If you have questions for either John or Ken regarding Sonoro Gold, then please email those into to me at Shad@kereport.com.

Click here to follow the latest news on Sonoro Gold

For more market commentary & interview summaries, subscribe to our Substacks:

The KE Report: https://kereport.substack.com/

Shad’s resource market commentary: https://excelsiorprosperity.substack.com/

Investment disclaimer: This content is for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any security. Investing in equities and commodities involves risk, including the possible loss of principal. Do your own research and consult a licensed financial advisor before making any investment decisions. Guests and hosts may own shares in companies mentioned, and companies profiled may be sponsors of the KE Report.

Leave a Reply