Weekend Show – Peter Boockvar & Matt Geiger – From Wall Street to Gold Stocks: Markets and Resources in Focus

This weekend’s show dives into what’s really driving markets amid tariff tensions and why global money is quietly rotating into commodities and resource stocks.

If you enjoy the show, be sure to subscribe to our podcast feed (KER Podcast), YouTube channel, and follow us on X for more market commentary and company interviews. Don’t forget to subscribe and leave us a review!

Also check out our Substack where we email you summaries of Daily Editorials and the Weekend Show! Click here to check it out.

Show Segments

- Segment 1 & 2 – Peter Boockvar, Chief Investment Officer at Bleakley Financial Group and editor of The Boock Report on Substack, joined the show to share his views on a market rally driven by AI enthusiasm despite uneven economic data, a global rise in long‑term rates, and shifting foreign capital flows. He also highlighted opportunities in international equities, a sustained bull case for commodities like gold, silver, and oil, and the need for patience with resource stocks as sentiment slowly rebuilds.

- Click here to follow Peter at The Boock Report.

- Segment 3 & 4 – Matt Geiger, Managing Partner at MJG Capital, joined the show to discuss his resource‑focused fund’s strong first half of 2025, driven largely by precious metals and standout positions like Bravo Mining and Neo Performance Materials, while highlighting his portfolio’s heavy weighting in copper and growing exposure to prospect generators. He also shared insights on shifting global capital flows, U.S. rare earth policy moves like the MP Materials deal, and Tether’s investment in Elemental Altus Royalties as early signs of new outside capital entering the mining sector.

- Click here to visit the MJG Capital website and read over Matt’s investor letter.

BLOW ME TO BERMUDA! DT 😉

That made me chuckle DT. 🙂

Yes, I do get about 150-200 emails per day, and it takes me considerable time to filter through all the noise to find the signal. If I take a few days off without looking, it is a deluge to sort through, which is what I did a lot of yesterday and today thus far. As for my pants, I’ve gained a little weight eating a strict diet of pizza and beer so if they are shorter it is because my waistline grew a bit. Haha!

Hi Ex, I don’t eat too much Pizza maybe just once a year, it tends to ball up and stick in your intestines and can cause blockages. However, with beer the “nectar of the gods” that is another matter. LOL! DT 🤣

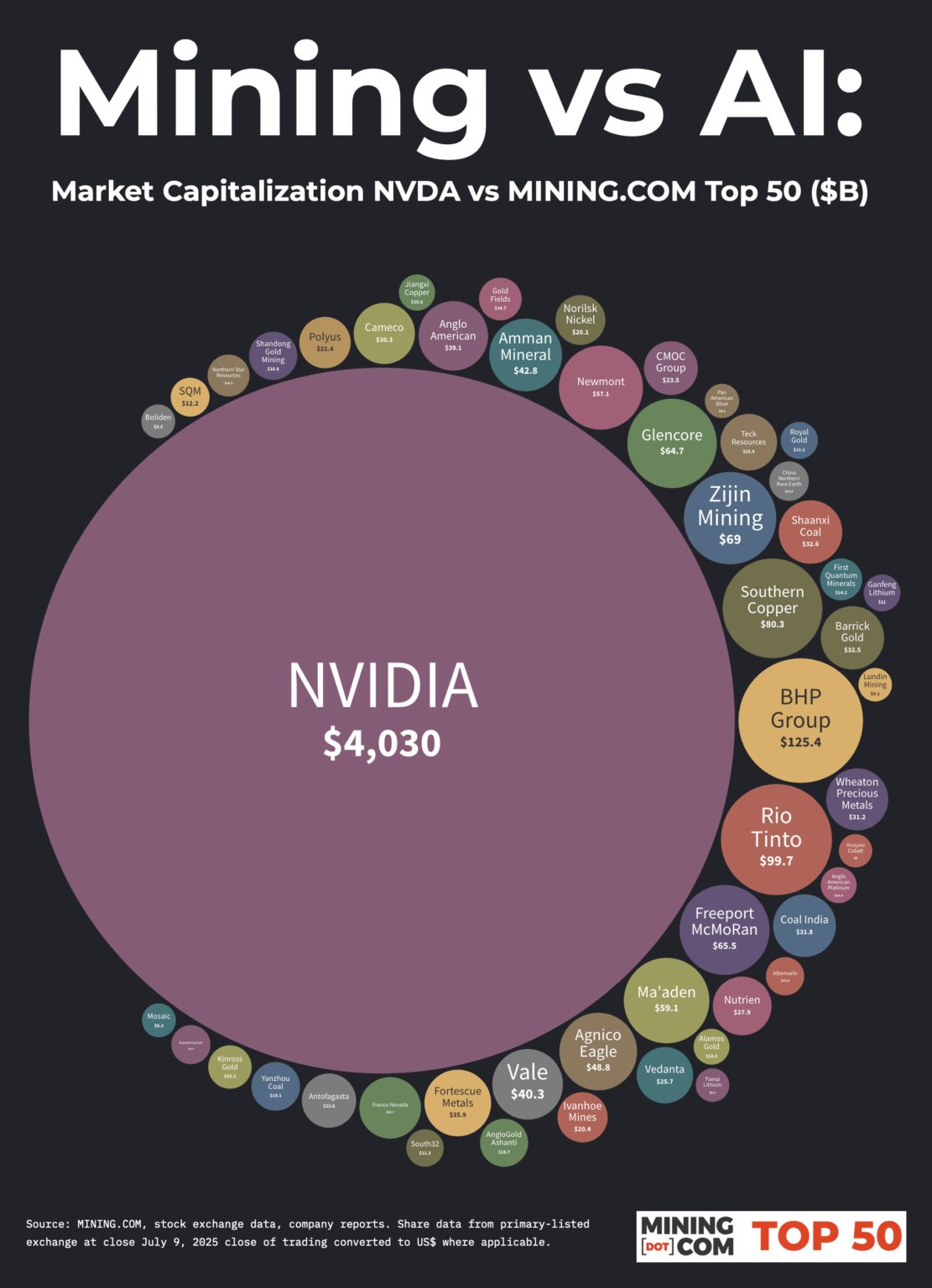

Nvidia hits $4 trillion – How do mining stocks stack up?

Frik Els – Mining.com – July 11, 2025

https://www.mining.com/chart-nvidia-hits-4-trillion-how-do-mining-stocks-stack-up/

The chart from that article above that contrasts the market cap of Nvidia versus all the senior miners is quite revealing:

https://www.mining.com/wp-content/uploads/2025/07/mining-v-ai-jul-2025-nvidia-top-50-1111×1536.jpg

{kind=link}

I talked about Nvidia a couple of days ago on this site, it had gained $735 billion in one month. At the time it was $4 Trillion $220 billion. This is a very dangerous situation to say the most. DT

That makes Nvidia twice as ‘valuable’ as all of Canada’s GDP… ridiculous for something ultimately designed to control the populace.

+2

How the United States Can Enhance Critical Minerals Supply

Richard Longstaff – Wall Street Journal

As the U.S. government considers how to strengthen America’s economic and national security, many industry stakeholders are calling for a more cohesive and coordinated approach to the development of critical minerals, including rare earth minerals, to accelerate results.

Why it matters: Progress in the past decade toward achieving resource security has been slow. More than 15 federal agencies are currently engaged in activities and programs aimed at increasing the United States’ mineral security, but these initiatives have at times overlapped or lacked effective coordination.

If U.S. industries from advanced manufacturing to energy, semiconductors, and defense applications continue to rely on foreign mineral supply chains, the United States will become increasingly vulnerable to potential disruptions of those same supply chains and industries.

By the numbers: Of the 50 elements deemed critical to the American economy and national security by the U.S. Geological Survey, the United States is 100% dependent on foreign suppliers for 12 of them and is more than 50% reliant on non-domestic sources for another 29.

What’s next: Through an executive order, President Trump created and empowered the National Energy Dominance Council (NEDC) comprising at least 19 senior U.S. government officials to advise the White House on strengthening the U.S. energy sector, improving permitting and regulation, enhancing private sector investments, and facilitating cooperation among government agencies and industry, including for critical minerals. The Trump administration has made critical minerals security a key component of its energy-focused strategy, evident by several recent executive orders.

The NEDC could coordinate, manage, and work closely with relevant U.S. government agencies and key private-sector stakeholders to implement the critical minerals action plan and help identify additional policy and investment measures that could increase the supply of key minerals and enhance supply chain security. Such a critical minerals action plan could focus on three priorities:

Fostering a domestic renaissance for the mining and processing of critical minerals

Strengthening international cooperation and expanding U.S. access to critical mineral production and processing capacity of America’s global partners

Mitigating risk and fostering a well-functioning and more transparent critical minerals market.

Go deeper: The priorities of this critical minerals action plan could inform multiple actions to help advance three key outcomes:

Reduced reliance on imports from selected countries, measured by official trade data

Enhanced competitiveness of the reconstructed U.S. mining industry, measured by regular, reputable surveys such as the survey conducted by the Fraser Institute7 capturing key industry data, including average permitting time, the number of workers in the critical minerals industry, and the number of projects in development

Reduced risk of market disruptions, measured by numerous formal reporting channels, including stockpile reporting, price volatility, and increased transparency.

The bottom line: By designing a time-sequenced, prioritized plan that can be implemented with an effective accountability framework, the United States could significantly enhance the attractiveness of its domestic mining industry for new investments. It could also promote supply chain access, creating flexibility to respond to market movements and developing resilience against future supply chain shocks.

By following a targeted strategy and working with industry toward the achievement of a set of common objectives, the U.S. government can make tangible and measurable progress toward its goal to promote U.S. critical mineral security and move from being a primary consumer and price-taker in a nontransparent market to being a supply maker in a transparent and resilient market.

Corporate Insiders Have Never Been More Bearish

Jesse Felder – The Felder Report – (07-19-2025)

I’ve not seen it mentioned anywhere in the media but do you ever wonder how many of the podcasts on you tube or other social media internet sites are backed by the CIA, MI6, and various NGOS?

That’s a good point Doc. As you know, at least here at the KER, our podcast is run by 2 guys with laptops in Vancouver and Seattle, and we do our best to share accurate info and keep it real.

P.S. – We should get you back on the show soon to talk technicals on the markets, metals, and stocks.

Hi, Ex, I wouldn’t be surprised if we hit a little quiet period for these PM stocks. I mentioned on Friday about adding a position into WWR which I already had a large position. You might want to look at the stock. It’s a graphite processing company that will benefit from bringing back supply lines to the U.S. The company has taken off due to an announcement.

Doc, are technicals largely informing your comments yesterday and today? The idea that some backing and filling is now in order because so many pm stocks have gapped up recently?

Thanks.

Just uncomfortable with some of the price actions such as kooyf. I don’t see any huge price movements down for most of the PM stocks but just some consolidation for awhile. Also, as you mention, some of the gap action. Regardless, I just keep adding a little on all pullbacks like I’ve been doing for 2 years. Most of my average cost basis is very low and adding a few thousand shares here or there on these pullbacks don’t move my cost basis much higher.

Thanks for the heads up on Westwater Resources. I remember many years ago when they were a uranium company, but didn’t realize that they had shifted over to graphite.

Yes, it wouldn’t surprise me to see some of the high flying PM stocks take a breather for a bit, to cool off their momentum and strength indicators.

I’ve been trimming back some positions up multi-fold over the last few weeks to raise some spare cash and personally have the biggest cash position inside my trading account that I have for years… but still have plenty of exposure on to keep riding any moves higher.

Martin Pring wrote an interesting article on stockcharts saying inflation-sensitive stocks look set to move higher. (Commodities) His inflation/deflation ratio has broken out

https://schrts.co/gTuCGNkv

Nice. The Silver-Gold Ratio and the silver miners are giving the same message…

https://schrts.co/pnGgrBtQ

Yep. Astute of you!

XAU priced in CRB arrived at interesting and significant resistance 6 weeks ago…

https://schrts.co/PRTQJBec

https://www.fibonomics.com/2025/07/natgas-pull-back-complete.html

NatGas : Bottom Complete : Deeper Pull Back Likely

I asked Deepseek to report on some precious metals companies. It took about 20 seconds for it to come up with a pretty long answer. Information was well organised with Derpseek’s own opinions included.

A Nuclear Engineer Explains Why He Favors Hydrograph Clean Power with Jay Taylor

DT, I asked Deepseek about HG and this was the answer given in under 5 seconds.

Based on public information and analysis of Hydrograph Clean Power’s (HG) technology, their graphene products (**specifically their signature “Hyperion” fractal graphene**) possess **several potentially superior characteristics compared to many competitors**, particularly in terms of **purity, structure, production method, and environmental profile.** However, declaring absolute, across-the-board “superiority” is complex and depends heavily on the specific application and the competitor being compared.

Here’s a breakdown of HG’s potential advantages and the challenges:

**Arguments for Superiority in Key Areas:**

1. **Exceptional Purity:**

* **Claim:** HG’s detonation synthesis process produces graphene with extremely low impurity levels (consistently < 10 ppm, often < 1 ppm for metals like iron). This is significantly lower than graphene produced via many common methods (like chemical reduction of graphene oxide – rGO, or CVD).

* **Why it matters:** Purity is critical for high-performance applications like electronics, batteries, and certain composites where impurities drastically degrade performance (e.g., cause short circuits, reduce conductivity, catalyze unwanted reactions).

* **Superiority:** For applications demanding ultra-high purity, HG's material has a *strong claim* to superiority over rGO and potentially other methods.

2. **Unique Fractal Structure:**

* **Claim:** Hyperion graphene has a distinctive branched, fractal-like 3D structure, unlike the flat 2D sheets typical of mechanically exfoliated or CVD graphene, or the crumpled sheets/flakes of rGO.

* **Why it matters:** This structure offers:

* **High Surface Area:** Beneficial for sensors, catalysis, and energy storage.

* **Easier Dispersion:** The structure may integrate more readily into polymers and composites without extensive functionalization or risking re-agglomeration.

* **Potential for Unique Properties:** The branching could create unique conductive pathways or reinforcement mechanisms.

* **Superiority:** Offers distinct structural advantages *different* from competitors, potentially superior for specific composite or conductive ink applications where dispersion is key.

3. **Scalable & Efficient Production:**

* **Claim:** Their proprietary detonation process is continuous, uses relatively low energy compared to CVD, requires no harsh chemicals (unlike rGO), and is inherently scalable. They claim a low cost structure at scale.

* **Why it matters:** Scalability and cost are the biggest hurdles for graphene commercialization. A truly scalable, clean, low-cost process is a major competitive advantage.

* **Superiority:** The *process* has significant potential advantages over CVD (energy/cost) and rGO (purity/chemical use). If proven at full commercial scale, this could be a *fundamental* superiority.

4. **Environmental Profile (Clean Production):**

* **Claim:** The process uses acetylene and oxygen as primary feedstocks, produces minimal waste (mostly CO2 and water vapor, which can be captured), and avoids toxic solvents or strong acids/oxidizers/reducing agents used in rGO production.

* **Why it matters:** Increasingly important for ESG compliance, appealing to sustainability-focused customers and industries, and reduces regulatory burden/cost of waste disposal.

* **Superiority:** Clearly superior environmental profile compared to rGO production. Likely more favorable than some other methods too.

**Challenges and Caveats (Why "Superior" Isn't Universal):**

1. **Commercial Scale & Validation:** While HG has a pilot plant and is commissioning its first commercial facility (Kansas), they are still relatively new to the market. Widespread commercial adoption and validation of Hyperion graphene in *end-user products* is still developing. Competitors with established production and customer bases (like Cabot, SGL, Thomas Swan, NanoXplore, Versarien, etc.) have more proven commercial track records, even if their material might have different specs.

2. **Application Specificity:** "Superiority" depends entirely on the application.

* For high-strength composites requiring large, pristine 2D flakes, CVD graphene might still be preferred.

* For applications where cost is paramount and moderate quality is acceptable, rGO might be "superior" from a cost perspective.

* HG's fractal structure might not be ideal for *every* application.

3. **Performance Data vs. Competitors:** While HG publishes performance data (e.g., conductivity in inks, battery results), direct, independent, head-to-head comparisons with specific competitor materials in identical applications are less common. Claims need ongoing validation in real-world settings.

4. **Market Position & Maturity:** HG is currently a smaller player competing against well-funded, established chemical and materials companies with vast R&D, sales, and application development resources. Achieving market penetration takes time.

5. **Graphene Application Development:** The market for graphene is still evolving. Even the "best" graphene needs well-developed application pathways to succeed commercially. HG is actively working on this (e.g., batteries, resins, inks).

**Conclusion:**

* **Yes, Hydrograph Clean Power's Hyperion fractal graphene demonstrates several *potentially* superior attributes:** exceptionally high purity, a unique and potentially advantageous 3D structure, a clean and scalable production process, and a strong environmental profile.

* **These attributes give it a significant *competitive edge*, particularly in applications demanding ultra-high purity, easy dispersion, or sustainable sourcing.**

* **However, declaring blanket "superiority" over *all* competitors for *all* applications is premature.** Commercial scale validation, market penetration, and application-specific performance comparisons against established players are still ongoing challenges. The graphene market is diverse, and different types serve different needs.

**In essence: HG has a highly differentiated and technologically advanced product with strong claims to superiority in specific key areas (purity, clean production, structure). Whether this translates to *market* superiority depends on successful commercial execution and demonstrating clear performance advantages in target applications against established competitors.** They are a promising innovator, but the competitive landscape remains challenging.

Hi Terry, thanks for that analysis, purity is the number 1 criteria for investing in graphene, I believe like Deepseek says that Hydrograph has a superior product and yes, they are a new company, but they have the right technical team to gear up for production.

They have all the proper patents which will protect their technology in The West, but I won’t vouch for what might happen in China. Their product is being compared to the development of the resistor in 1949.

They are in the early stages but that is when you want to get involved as an investor. They see themselves as an American company technology company with a listing on The Nasdaq which is where they are headed according to their CEO.

If you listen to that video that I posted above their product has endless uses from the making of cement to high tech in all fields and in military applications, it really stands out. I hope they can execute and that they don’t get taken out. DT

“resistor?” I think you mean transistor, developed at Bell labs in New Jersey. Resistors go back decades before 1949..

Yes Rufust, I meant transistor, thanks for pointing that out! DT

And Terry, I hope we can collaborate in the future with your “Deepseek” analysis analyzer. DT 😜😜😜

Thankyou Terry

I’m not familiar with Deepseek.. going to look into it

Opportunities In Rare Earth Elements Stocks – Part 2

Excelsior Prosperity w/ Shad Marquitz (07/19/2025)

Supply/Demand fundamentals, Energy Fuels (UUUU), MP Materials (MP), Neo Performance Materials (NEO.TO)

https://excelsiorprosperity.substack.com/p/opportunities-in-rare-earth-elements-bf1

Free Rambus article

https://rambuschartology.substack.com/p/can-big-chart-patterns-lead-to-even

Here’s what I found about DeepSeek:

DeepSeek is facing bans and restrictions due to data privacy concerns, national security risks, and potential ties to the Chinese government. Several countries and organizations have taken action, including Germany requesting its removal from app stores and the U.S. Navy banning its use by service members.

Here’s a breakdown of the reasons:

Data Privacy:

.

DeepSeek’s handling of user data, particularly its storage of data in China, has raised concerns about potential leaks and lack of transparency.

National Security:

.

Some governments fear DeepSeek could be used for surveillance or espionage, especially given its connections to China.

Lack of Transparency:

.

DeepSeek’s failure to fully explain how it uses user data and who has access to it has fueled these concerns.

Potential Misinformation:

.

There are worries that AI-generated content from DeepSeek could be used to spread misinformation.

Government Restrictions:

.

Several U.S. states have banned DeepSeek from government devices and networks, citing security risks.

App Store Removal:

.

Germany has requested Apple and Google to remove DeepSeek from their app stores due to data transfer concerns.

This is what Deepseek says about IPT, produced instantaneously.

Impact Silver (TSXV: IPT) **can provide exposure to silver prices, but it comes with significant company-specific risks that make it a more speculative and less direct choice compared to other options.** Here’s a breakdown:

**Arguments FOR Exposure to Silver Price:**

1. **Pure Silver Focus:** Impact Silver’s primary revenue source is silver production from its Zacualpan project in Mexico. Their success is directly tied to the silver price.

2. **Leverage Potential:** Mining stocks *can* offer leverage to the underlying metal price. If silver prices rise significantly *and* IPT maintains or increases production while controlling costs, the stock price could potentially rise faster than the silver price itself (and vice versa on the downside).

3. **Exploration Upside:** As a junior miner, successful exploration results on their large land package could significantly increase their resource base and future production potential, boosting the stock price independently of, or amplified by, silver prices.

**Arguments AGAINST it being a “Good” Choice (Significant Risks & Challenges):**

1. **Operational Performance & Costs:**

* **High Costs (AISC):** Impact has historically struggled with high All-In Sustaining Costs (AISC), often hovering around or above $20 USD/oz in recent years. When silver prices are below or near this level, profitability is squeezed or eliminated.

* **Production Volatility:** Production levels have fluctuated and haven’t shown consistent growth. Reliable and scalable production is key for a miner to capitalize on higher metal prices.

* **Profitability Issues:** Due to high costs and operational challenges, the company has frequently reported losses or minimal profits, even during periods of decent silver prices. **This is the core issue.**

2. **Leverage Works Both Ways:** While leverage can amplify gains, it also amplifies losses. If silver prices fall, IPT’s high costs make it particularly vulnerable, and the stock price could plummet much faster than the silver price.

3. **Small Scale & Liquidity:** As a small-cap junior miner, the stock is less liquid and more volatile than larger producers or ETFs. It can be susceptible to sharp price swings based on news, market sentiment, or relatively small trades.

4. **Execution Risk:** Successfully expanding production, discovering new high-grade zones, or significantly reducing costs requires consistent and effective management execution, which has been challenging.

5. **Dependence on Single Asset:** All operations are centered on Zacualpan. Any significant operational setback (geotechnical issues, permitting delays, labor issues) disproportionately impacts the entire company.

6. **Market Performance:** Historically, IPT’s stock price has often underperformed the price of silver itself over extended periods, reflecting the operational challenges and lack of consistent profitability.

**Compared to Other Silver Exposure Options:**

* **Physical Silver / ETFs (e.g., SIVR, PSLV, SLV):** Provide the *most direct* exposure to the silver spot price without company-specific operational risks. This is the cleanest play.

* **Larger Silver Miners (e.g., PAAS, AG, FSM, HL):** Generally offer more diversified operations, larger scale, lower costs (relatively), better liquidity, and sometimes dividends. They still provide leverage but with less extreme volatility and execution risk than juniors like IPT.

* **Silver Streaming/Royalty Companies (e.g., WPM, FNV, SIL):** Provide financing to miners in exchange for future metal at fixed, low costs. They offer leverage to silver prices with significantly less exposure to mining operational risks and cost inflation.

**Conclusion:**

* **Exposure? Yes,** IPT provides exposure to silver prices through its operations.

* **”Good” Choice? Generally, No.** Due to its persistent high costs, inconsistent profitability, operational volatility, and history of underperformance relative to silver, IPT is considered a **high-risk, speculative investment** for silver exposure.

* **Investor Profile:** It might *only* be suitable for investors who:

* Have a very high risk tolerance.

* Have a strong conviction that silver prices will rise *significantly and sustainably* (well above IPT’s cost base).

* Believe IPT can successfully execute on reducing costs, increasing production, and/or making a major exploration discovery.

* Understand they are taking on substantial company-specific risk beyond just silver price movement.

**Recommendation:**

If your primary goal is **reliable exposure to the silver price**, **physical silver, silver ETFs, or established larger miners/streamers are significantly better and less risky choices** than Impact Silver (IPT.V). IPT is a speculative play on a potential turnaround or exploration success, not a reliable vehicle for pure silver price exposure. Thorough due diligence on their current financials, operational plans, cost structure, and management guidance is essential before considering an investment.

That’s a fairly succinct IPT summary. Otherwise, how much does it matter if Big Brother speaks with a Chinese accent?

Take a look at any main stream investing source and they’ll say the same thing. All juniors are very risky by definition. Why do you think they offer so much upside when things turn bullish and so much downside when things turn bearish? Why do you think the term “optionality” is frequently used to describe them? Nevertheless, it should be pretty obvious to you that IPT is among the least risky explorers because of its production and even its long-standing good relationship with the Mexican government and the remote community in which it is the largest employer.

Deepseek can do all that searching quickly, without any time consuming DD from me.

If people are worried about Chinese government involvement they could use a westetn AI service.

That’s not what I’d call due diligence.

How much can you believe in the governments reporting on CPI or PPI, the investors here know that it is very difficult to get the truth. You will never get the truth from the mainstream media but on the internet, you have a chance to filter through a number of possible interpretations and if you are shrewd enough you can get enough information to make a reasonable understanding of what is going on.

Thanks for expanding our knowledge, Terry, this applies to life as well as investing. DT

Meteoric(MEI.ASX) was/is a Rick Rule favorite which has tripled this year. So I asked Deepseek about its Brazilian deposit and this is the immediate response.

Based on current information and industry analysis, **yes, there is a reasonable chance** that Meteoric Resources’ (MEI.ASX) Brazilian rare earth elements (REE) clay deposit (primarily the Caldeira project) could be put into production, **but significant hurdles and risks remain.** Here’s a breakdown of the key factors:

### **Reasons for Optimism (Supporting Production Chance):**

1. **High-Grade Ionic Clay Deposit:**

* Caldeira boasts **exceptionally high grades** for Total Rare Earth Oxides (TREO) and particularly for the valuable magnet rare earths (NdPr, Tb, Dy) compared to many global peers. Surface samples and drilling consistently show grades significantly above industry averages for ionic clays.

* **Ionic Clay Advantage:** This deposit type is generally **cheaper and simpler to mine and process** than hard rock REE deposits. Extraction uses straightforward leaching (similar to copper heap leaching), avoiding expensive and complex cracking/separations needed for hard rock. This lowers capital (CAPEX) and operating (OPEX) costs, improving project economics.

2. **Positive Preliminary Economics (PEA):**

* The recently completed Preliminary Economic Assessment (PEA) demonstrated **strong potential economics:**

* **Very Low Estimated OPEX:** Projected operating costs per kg of TREO were among the lowest reported globally for REE projects.

* **Attractive CAPEX:** Estimated initial capital expenditure was relatively modest for a project of its scale.

* **High NPV & IRR:** The PEA indicated robust Net Present Value (NPV) and Internal Rate of Return (IRR), suggesting potential profitability even under conservative price assumptions.

* *This PEA provides a solid technical foundation for advancing the project.*

3. **Scalability & Resource Size:**

* The resource is already large (Millions of tonnes), and importantly, it’s **open in multiple directions and at depth.** There’s high potential for significant resource growth through further drilling, which could further enhance project economics and lifespan.

4. **Strategic Location & Support:**

* Located in Minas Gerais, Brazil, a mining-friendly state with established infrastructure (roads, power, water access, proximity to ports). Brazil has a supportive government actively looking to develop critical mineral supply chains, including REEs.

5. **Market Demand & Supply Security:**

* Demand for NdPr, Dy, and Tb (key products from Caldeira) is driven by **permanent magnets essential for EVs, wind turbines, and electronics.** This demand is expected to grow exponentially.

* Western governments and industries are **desperately seeking non-Chinese REE supply** to de-risk supply chains. Caldeira, as a potentially low-cost, scalable project outside China, fits this strategic need perfectly.

### **Significant Risks & Hurdles (Challenges to Production):**

1. **Early Stage (Pre-Feasibility):**

* The PEA is just the **first major economic study.** It’s based on preliminary data and assumptions. The critical next steps are the **Pre-Feasibility Study (PFS)** and **Definitive Feasibility Study (DFS)**. These require significantly more detailed engineering, metallurgical test work (especially on separation), environmental studies, and mine planning. **Technical or economic flaws can be uncovered during these stages, potentially derailing the project or requiring major redesign.**

2. **Metallurgical & Process Risks:**

* While ionic clays are simpler, **achieving high recovery rates and producing separated, high-purity REE oxides profitably at scale is complex.** Extensive pilot plant testing is needed to prove the flowsheet works consistently. Scaling up from lab/bench scale to commercial production always carries risks.

3. **Permitting & Environmental/Social License:**

* Obtaining all necessary environmental and operational permits in Brazil, while generally feasible, is a **complex, time-consuming, and potentially costly process.** Local community engagement and securing a “Social License to Operate” are critical and can be challenging.

4. **Funding Requirement:**

* Moving from PEA through PFS/DFS to construction requires **hundreds of millions of dollars.** While the PEA suggests low CAPEX relative to output, raising this capital for a junior miner is a major hurdle. It likely involves significant dilution through equity raises, debt financing (which may be difficult pre-DFS), or attracting a strategic partner/offtake investor. Market conditions significantly impact this.

5. **REE Price Volatility & Market Dynamics:**

* REE prices, especially NdPr, are **highly volatile.** A sustained downturn in prices could make the project uneconomical despite the low OPEX. Competition from other new non-Chinese projects (e.g., in Australia, Africa, North America) could also impact future market share and pricing.

6. **Project Execution Risk:**

* Successfully constructing and commissioning a mine and processing plant, even a relatively simple one, involves significant execution risk – delays, cost overruns, technical commissioning issues.

### **Conclusion:**

* The **technical fundamentals of the Caldeira project are very strong:** high grades, favorable mineralogy (ionic clays), potentially low costs, scalability, and strategic location. The positive PEA adds credibility.

* The **strategic demand context is highly favorable** for non-Chinese, low-cost REE production.

* **However, the project is still at a relatively early stage.** The path from a promising PEA to commercial production is long, capital-intensive, and fraught with technical, financial, permitting, and market risks. Many promising projects fail at the feasibility or financing stages.

**Therefore, while there is absolutely a reasonable chance Caldeira reaches production (likely the mid-to-late 2020s at the earliest, assuming no major delays), it is far from guaranteed.** The tripling of the stock price reflects high market optimism and anticipation of this potential, but it also increases the risk for investors if significant hurdles emerge.

**Key things to watch for in the near-to-medium term:**

1. **Progress & Results of PFS/DFS:** This is the *most critical* de-risking step.

2. **Metallurgical Test Work:** Especially pilot plant results proving separations at scale.

3. **Permitting Progress:** Timelines and any community issues.

4. **Funding Strategy:** Announcements of strategic partnerships, major offtake agreements, or successful capital raises.

5. **Resource Expansion:** Further drilling results showing resource growth.

The chance is reasonable and supported by the project’s inherent strengths, but investors must understand and price in the significant execution risks that remain.

PFS and trading halt on Meteoric this Monday morning

Been a while. Great show guys. How is Big Al doing? Please pass along our Well Wishes to him. He is missed. Thank you!

When Ex goes on a short vacation without his cell phone buddy for three days (down to the beach) and checks his e-mail there are hundreds of messages. If he takes off five days they could register in the thousands.

His stature in the mining industry has grown so much that his legs have started to lengthen and when he puts on his regular pants it looks like he is wearing Bermuda shorts. He has become a product of natural selection.

I always liked what the boys call BS, (or shooting the s**t) if you watch George Carlin, you will know what I mean, but in this case, it could be true! LOL! DT 🤣🤣🤣